Key Takeaways

- Strategic transactions and expanded credit facilities enhance Plymouth Industrial REIT's capacity for growth, with positive impacts on revenue and earnings.

- Favorable market conditions and targeted acquisitions support revenue growth and improved net margins, driven by leasing efforts and capital deployment.

- Tenant challenges, market conditions, and acquisition uncertainties could threaten revenue stability, growth projections, and investor confidence despite optimism about future improvements.

Catalysts

About Plymouth Industrial REIT- Plymouth Industrial REIT, Inc. (NYSE: PLYM) is a full service, vertically integrated real estate investment company focused on the acquisition, ownership and management of single and multi-tenant industrial properties.

- The strategic transaction with Sixth Street provides Plymouth Industrial REIT with up to $500 million for acquisitions, enhancing their capacity for future growth and positively impacting revenue and earnings.

- The refinancing and upsizing of unsecured credit facilities to $1.5 billion bolsters the company's borrowing capacity, enabling further growth opportunities that could drive revenue and improve net margins.

- The market conditions for buildings under 250,000 square feet remain favorable, which supports Plymouth's mark-to-market leasing efforts, potentially increasing revenue and improving net margins.

- The company is actively pursuing a pipeline of over 11 million square feet in potential acquisitions worth $1 billion, which should contribute to revenue growth and enhance earnings once executed.

- Plymouth’s focus on leasing and capital deployment, particularly in high-demand markets, is likely to enhance occupancy rates and lease rates, positively impacting both revenue and net margins.

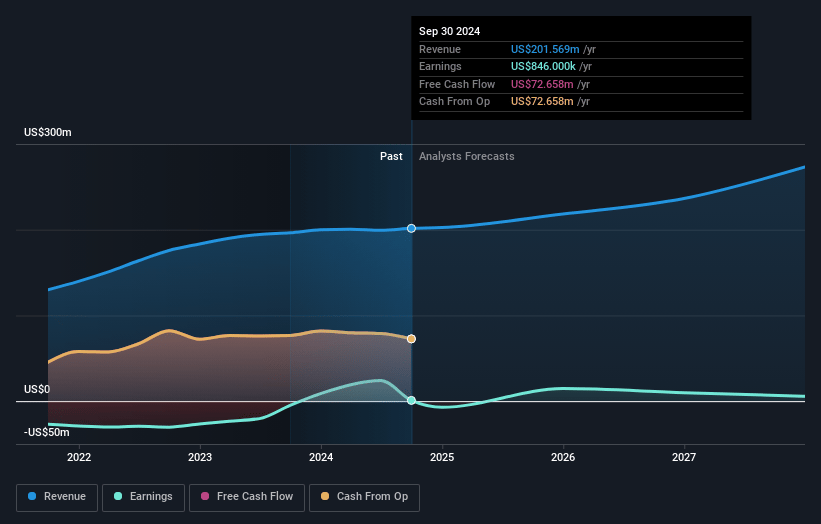

Plymouth Industrial REIT Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Plymouth Industrial REIT's revenue will grow by 10.1% annually over the next 3 years.

- Analysts are not forecasting that Plymouth Industrial REIT will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Plymouth Industrial REIT's profit margin will increase from 71.4% to the average US Industrial REITs industry of 30.8% in 3 years.

- If Plymouth Industrial REIT's profit margin were to converge on the industry average, you could expect earnings to reach $79.3 million (and earnings per share of $1.72) by about March 2028, down from $137.9 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 14.9x on those 2028 earnings, up from 5.8x today. This future PE is lower than the current PE for the US Industrial REITs industry at 31.5x.

- Analysts expect the number of shares outstanding to grow by 0.37% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.31%, as per the Simply Wall St company report.

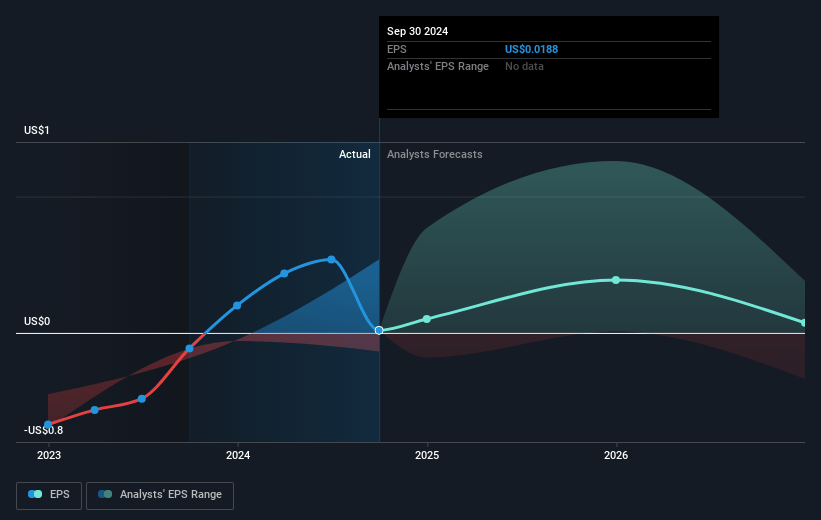

Plymouth Industrial REIT Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company faces tenant challenges, such as unexpected lease expirations and speculative leasing requirements, which could impact occupancy rates and, consequently, revenue stability.

- Market conditions, while generally favorable for smaller buildings, suggest tightening supplies that may strain the company’s ability to maintain high occupancy and lease rates, thus impacting overall earnings.

- Acquisition strategies are heavily dependent on securing advantageous terms and successful capital deployment, and failure to execute on planned acquisitions or delayed timelines could affect growth projections and financial performance.

- Significant capital has been deployed into acquisitions, but uncertainties regarding the timing and effectiveness of these acquisitions could impact future net margins if expected returns are not realized.

- The company expresses optimism about future leasing and occupancy improvements, but slow progress or unexpected vacancies, particularly in key markets like Cleveland and St. Louis, might pose risks to projected rental income and investor confidence.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $20.2 for Plymouth Industrial REIT based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $24.0, and the most bearish reporting a price target of just $17.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $258.0 million, earnings will come to $79.3 million, and it would be trading on a PE ratio of 14.9x, assuming you use a discount rate of 8.3%.

- Given the current share price of $17.44, the analyst price target of $20.2 is 13.7% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.