Key Takeaways

- RIDEA structure's growth potential may raise net income but higher operational costs risk compressing short-term margins.

- Asset sales and operator transitions could disrupt revenues as stable income sources are removed without immediate substitutes.

- The RIDEA platform, balanced portfolio diversification, strong liquidity, and experienced management position LTC Properties for transformative growth and stable financial performance.

Catalysts

About LTC Properties- LTC is a real estate investment trust (REIT) investing in seniors housing and health care properties primarily through sale-leasebacks, mortgage financing, joint-ventures and structured finance solutions including preferred equity and mezzanine lending.

- The implementation of the RIDEA structure is seen as a transformative growth strategy, as it allows for potential enhancement of net operating income and provides a new growth avenue, which impacts potential revenue and earnings positively.

- Reduction in lease income due to sales of properties and loan payoffs could lead to lower short-term revenue, as existing stable income sources are removed without immediate replacement.

- The required infrastructure and personnel cost increases to support the RIDEA platform will initially consume resources, potentially impacting net margins as expenses rise in the short term.

- Diversifying the portfolio with RIDEA could lead to higher G&A expenses and require significant upfront investment, which could compress net margins before anticipated revenue growth from this structure materializes.

- Operator transitions and asset sales are seen as strategic moves, but carry the risk of temporary revenue disruption, as existing rental income from these properties might not be immediately replaced.

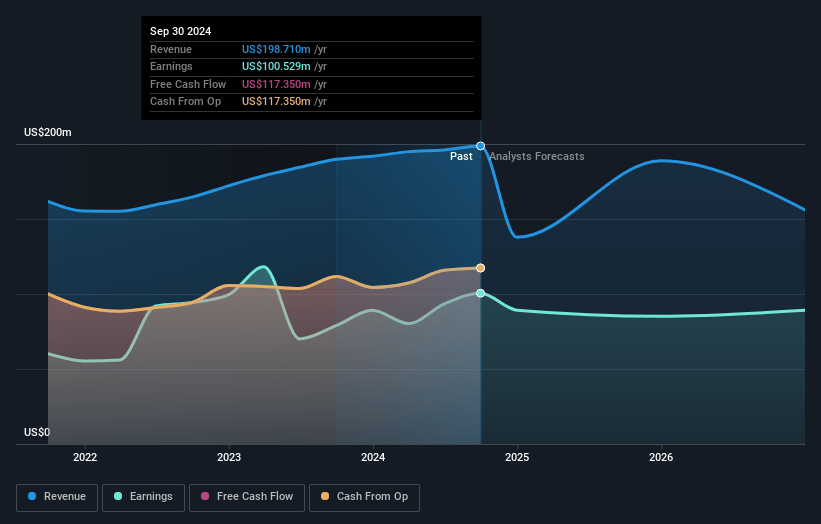

LTC Properties Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming LTC Properties's revenue will grow by 1.7% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 44.8% today to 39.2% in 3 years time.

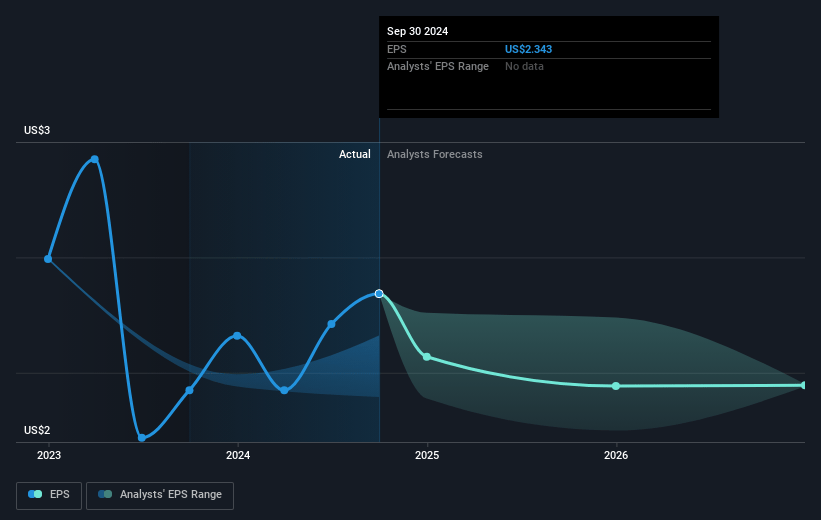

- Analysts expect earnings to reach $83.2 million (and earnings per share of $1.82) by about May 2028, down from $90.4 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 28.6x on those 2028 earnings, up from 18.0x today. This future PE is lower than the current PE for the US Health Care REITs industry at 33.1x.

- Analysts expect the number of shares outstanding to grow by 4.54% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.02%, as per the Simply Wall St company report.

LTC Properties Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The successful implementation of the RIDEA platform could position LTC for transformative growth, potentially increasing revenues and expanding profit margins through improved organic growth rates compared to traditional triple-net leases.

- LTC's strategic focus on diversifying its portfolio with a balance of operator, geography, property type, and investment vehicles may reduce operational risks and stabilize future earnings.

- The company's strong liquidity position, with approximately $680 million, and the reduction in leverage could provide financial flexibility to capitalize on growth opportunities, enhancing revenue and earnings potential.

- The depth and experience of LTC’s management team and board, along with recent strategic promotions, may provide resilience in navigating market cycles, potentially resulting in stable net margins and steady earnings.

- Improved operational performance indicators, such as increased occupancy in certain portfolios and successful asset conversions, could support sustained revenue growth and bolster overall financial health.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $37.286 for LTC Properties based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $42.0, and the most bearish reporting a price target of just $34.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $212.3 million, earnings will come to $83.2 million, and it would be trading on a PE ratio of 28.6x, assuming you use a discount rate of 7.0%.

- Given the current share price of $35.54, the analyst price target of $37.29 is 4.7% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.