Key Takeaways

- Hesitancy in data center leasing and reliance on price increases in RIM could constrain revenue growth, impacting margins and earnings.

- Economic uncertainties and competitive pressures in Digital Solutions may affect profitability, requiring innovation and managing costs amidst exchange rate volatility.

- Iron Mountain's strong financial growth, driven by digital solutions and data centers, benefits from diversified revenue, stable earnings, and high customer satisfaction.

Catalysts

About Iron Mountain- Iron Mountain Incorporated (NYSE: IRM) is trusted by more than 240,000 customers in 61 countries, including approximately 95% of the Fortune 1000, to help unlock value and intelligence from their assets through services that transcend the physical and digital worlds.

- The slowdown in leasing activity in the data center business due to pricing discipline could temper revenue growth, as the passing on a large leasing opportunity indicates hesitancy to compromise on returns, suggesting pricing pressures and potential stagnation in that segment. This may impact revenue and net margins if more such opportunities are foregone.

- The customer volume growth in the RIM (Records and Information Management) business is expected to remain flat to slightly up, meaning that revenue growth in this area will likely lean more heavily on price increases rather than organic expansion of volume, possibly constraining overall revenue growth potential.

- Growing competition and market dynamics impacting the profitability of the Digital Solutions and ALM segments could compress net margins. The continued pressure to innovate and expand capabilities in a highly competitive market could lead to increased costs without a commensurate increase in prices or volume.

- With global economic uncertainties and foreign exchange rate volatility already impacting results slightly, additional currency fluctuations or macroeconomic headwinds could negatively impact reported financials, affecting both revenue and earnings.

- The heavy concentration of significant ongoing and new business in economically sensitive sectors, such as government and large enterprises, might expose Iron Mountain to potential downturns or budget cuts, potentially impacting the consistency and growth of future earnings.

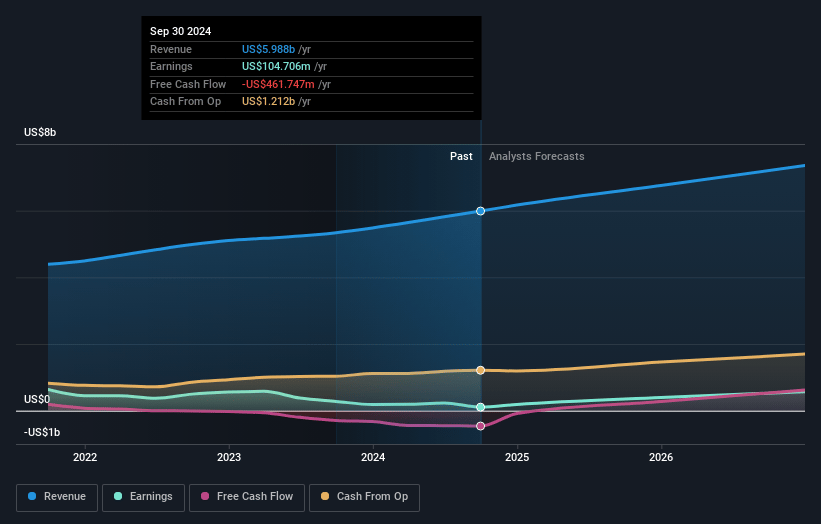

Iron Mountain Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Iron Mountain compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

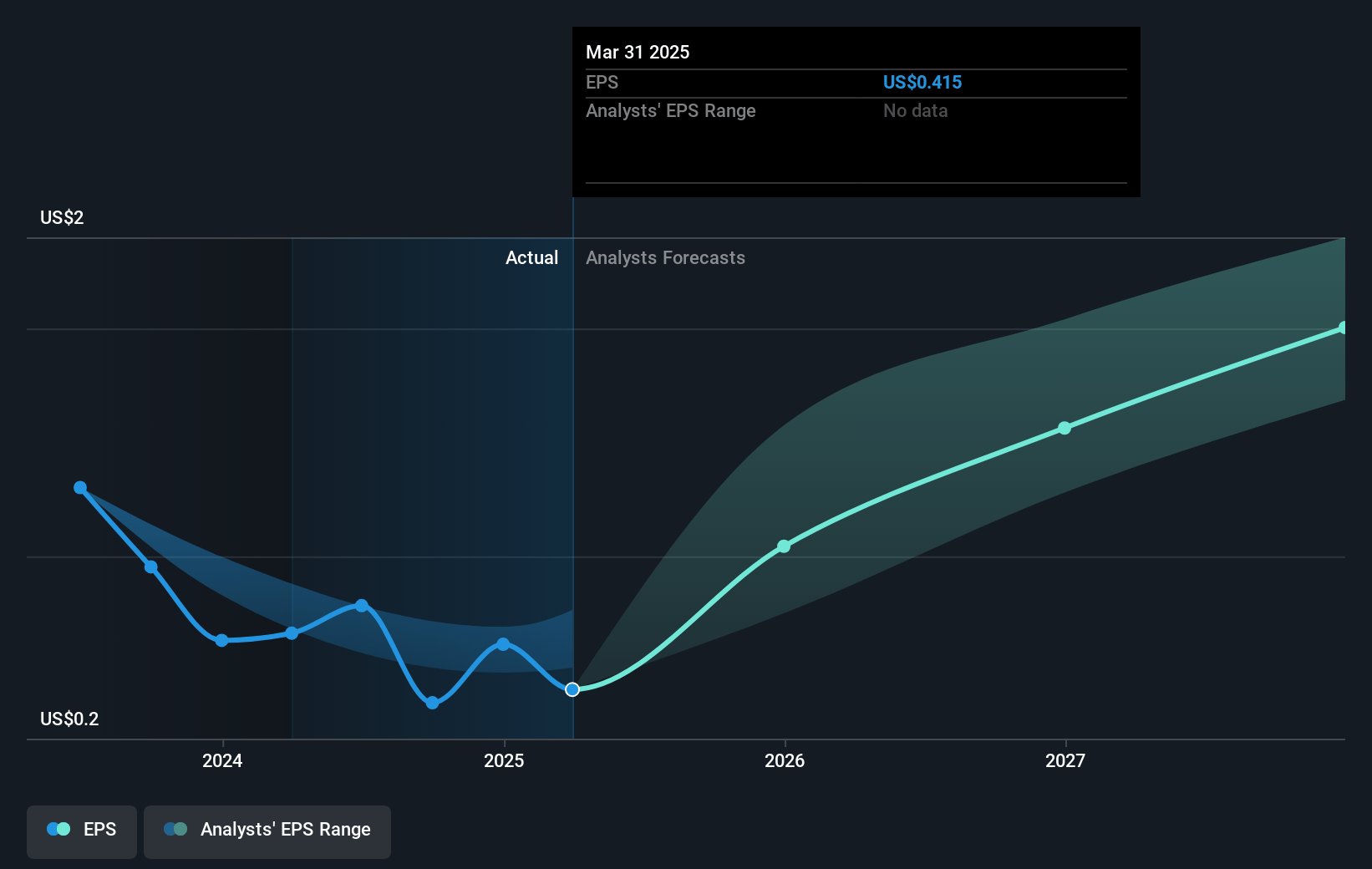

- The bearish analysts are assuming Iron Mountain's revenue will grow by 5.8% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 2.9% today to 9.5% in 3 years time.

- The bearish analysts expect earnings to reach $691.0 million (and earnings per share of $1.63) by about April 2028, up from $180.2 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 45.4x on those 2028 earnings, down from 137.3x today. This future PE is greater than the current PE for the US Specialized REITs industry at 27.7x.

- Analysts expect the number of shares outstanding to grow by 0.21% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.33%, as per the Simply Wall St company report.

Iron Mountain Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Iron Mountain reported record performance for 2024 with revenue increasing 12% to $6.1 billion, adjusted EBITDA growing 14% to $2.2 billion, and AFFO increasing 11% to $1.3 billion, indicating strong revenue and earnings growth.

- The company has consistently exceeded its growth targets, achieving a growth in revenue and adjusted EBITDA at an 11% CAGR since 2021, which outpaces the targets of 10%, suggesting continued strong financial performance.

- Iron Mountain's diverse portfolio, including a rapidly growing digital solutions segment and a robust data center business, contributes to a stronger revenue stream composition, with digital solutions setting record revenue in 2024 and data center revenue increasing 25% to $620 million, enhancing overall net margins.

- Recurring revenue streams, strong customer satisfaction, and vigorous cross-selling, especially with 95% of the Fortune 1000 among its customer base, provide a stable revenue basis and opportunity for higher earnings through diversified sales efforts.

- The guidance for 2025 projects revenue growth of 9% at the midpoint and adjusted EBITDA growth of 12%, supported by a substantial backlog and 94% leased under-construction data center assets, indicating high earnings visibility and contributing positively to financial stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Iron Mountain is $86.02, which represents one standard deviation below the consensus price target of $113.78. This valuation is based on what can be assumed as the expectations of Iron Mountain's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $140.0, and the most bearish reporting a price target of just $45.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $7.3 billion, earnings will come to $691.0 million, and it would be trading on a PE ratio of 45.4x, assuming you use a discount rate of 7.3%.

- Given the current share price of $84.21, the bearish analyst price target of $86.02 is 2.1% higher. The relatively low difference between the current share price and the analyst bearish price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystLowTarget holds no position in NYSE:IRM. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.