Last Update30 Apr 25Fair value Decreased 1.94%

Key Takeaways

- Strategic investments and development projects are poised to enhance revenue and earnings through rent growth and increased occupancy.

- Asset recycling and rising demand for high-quality leases are expected to improve portfolio quality, net margins, and cash flows.

- Economic challenges, high construction costs, and leasing uncertainties may threaten revenue growth and cash flow, impacting dividends and development-driven earnings.

Catalysts

About Highwoods Properties- Highwoods Properties, Inc., headquartered in Raleigh, is a publicly-traded (NYSE:HIW), fully-integrated office real estate investment trust (“REIT”) that owns, develops, acquires, leases and manages properties primarily in the best business districts (BBDs) of Atlanta, Charlotte, Dallas, Nashville, Orlando, Raleigh, Richmond and Tampa.

- The strategic investment activity, such as the acquisition of Advanced Auto Parts Tower in Raleigh's vibrant North Hills BBD, is expected to lead to long-term rent growth as existing rents are currently below market, thus impacting future revenue positively.

- The development pipeline, including the nearly completed and majority-leased 2827 Peachtree in Atlanta, which contributes to a projected $30 million incremental NOI, suggests potential future earnings growth as the properties stabilize.

- Successful lease signings, including the significant 145,000 square-foot lease at Symphony Place in Nashville, demonstrate strong demand and are projected to drive $25 million of NOI growth, which should enhance future earnings.

- The asset recycling strategy, involving selling non-core, capital-intensive properties and acquiring high-quality, commute-worthy assets, is expected to enhance overall portfolio quality and improve future net margins and cash flows.

- The rising leasing activity and increased net effective rents, with April’s accelerated new leasing volume, indicate potential future revenue growth and serve as a positive momentum for improving financials.

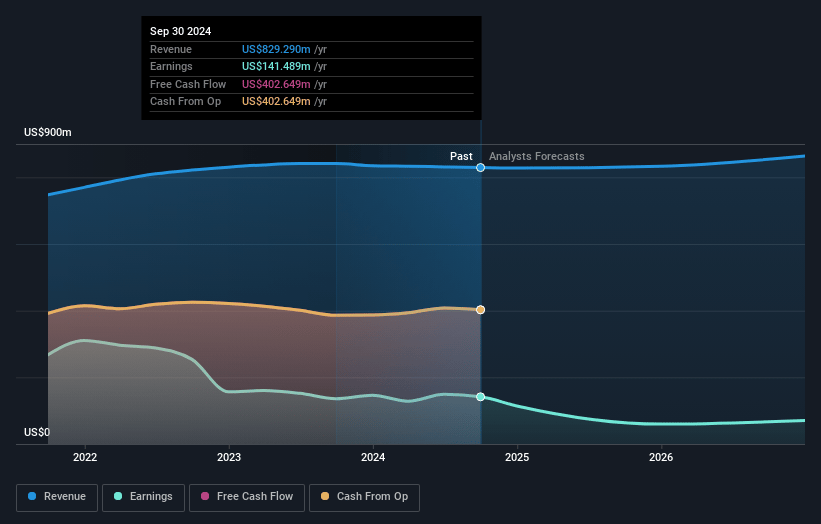

Highwoods Properties Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Highwoods Properties's revenue will grow by 2.2% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 12.0% today to 10.0% in 3 years time.

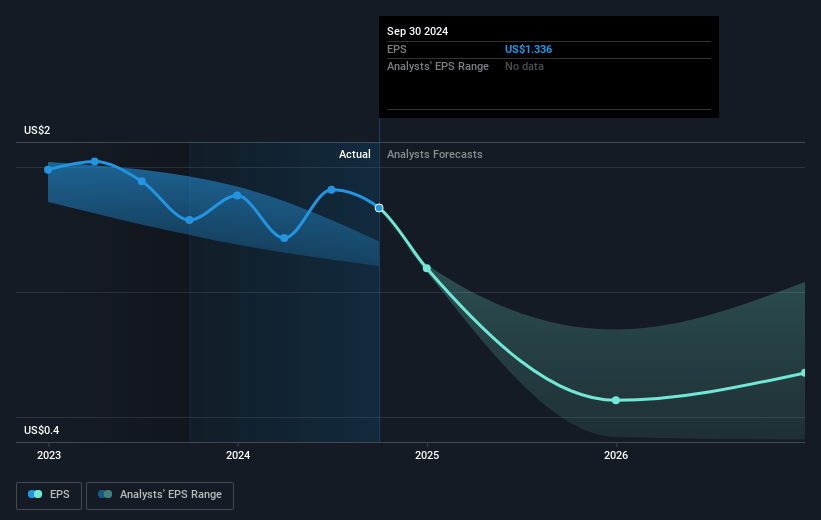

- Analysts expect earnings to reach $88.3 million (and earnings per share of $0.81) by about April 2028, down from $99.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 49.5x on those 2028 earnings, up from 30.0x today. This future PE is lower than the current PE for the US Office REITs industry at 64.8x.

- Analysts expect the number of shares outstanding to grow by 1.54% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.39%, as per the Simply Wall St company report.

Highwoods Properties Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Rising macroeconomic concerns and choppy capital markets could impact investor confidence, potentially affecting future revenue growth.

- Elevated construction costs and high vacancy levels are deterrents for new development projects, which could limit future earnings from development-driven NOI growth.

- Economic uncertainty, government cutbacks, global tariffs, and the possibility of a recession are headwinds that could affect leasing activity and revenue.

- The anticipated increase in leasing capital expenditure over the next few quarters could impact cash flow and net margins, possibly affecting the ability to maintain current dividend levels.

- Potential for increased concessions and long-term uncertainty about tenant expansions could affect future revenue and net earnings if market conditions do not improve.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $30.667 for Highwoods Properties based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $35.0, and the most bearish reporting a price target of just $22.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $885.2 million, earnings will come to $88.3 million, and it would be trading on a PE ratio of 49.5x, assuming you use a discount rate of 7.4%.

- Given the current share price of $27.73, the analyst price target of $30.67 is 9.6% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.