Last Update30 Apr 25Fair value Increased 0.63%

AnalystConsensusTarget has decreased revenue growth from 5.5% to 4.0%.

Read more...Key Takeaways

- Getty Realty is focusing on high-density metro areas and diversified sectors to stabilize and enhance future income and net margins.

- Improved operational efficiency and strategic project completions are expected to boost revenue growth and earnings resilience.

- Economic uncertainty and tenant risks may impact Getty Realty's revenues, as transaction volatility, credit risks, construction delays, and cost pressures threaten stability and earnings.

Catalysts

About Getty Realty- A publicly traded, net lease REIT specializing in the acquisition, financing and development of convenience, automotive and other single tenant retail real estate.

- Getty Realty has increased its investment pipeline to over $110 million, with 85% focused on development funding transactions, which should positively impact future revenue growth as these projects are expected to complete over the next 9 to 12 months.

- The company is diversifying its investments across four target sectors (auto service, convenience stores, drive-thru QSRs, and car washes), which may lead to stabilizing and potentially enhancing future net margins by distributing income streams across different, potentially recession-resistant sectors.

- Getty Realty's acquisition strategy prioritizes high-density metro areas with long-term triple net leases, which could improve earnings resilience by ensuring steady rental income and occupancy rates.

- The resolution of the Zips Car Wash bankruptcy situation, including the potential to recover 70% of the ABR with less than one quarter downtime, represents a catalyst for maintaining or slightly increasing net income and EBITDA margins.

- Improved G&A cost efficiency, expected to further increase as the company scales, may lead to enhanced net margins by reducing overall operating expense ratios against revenue.

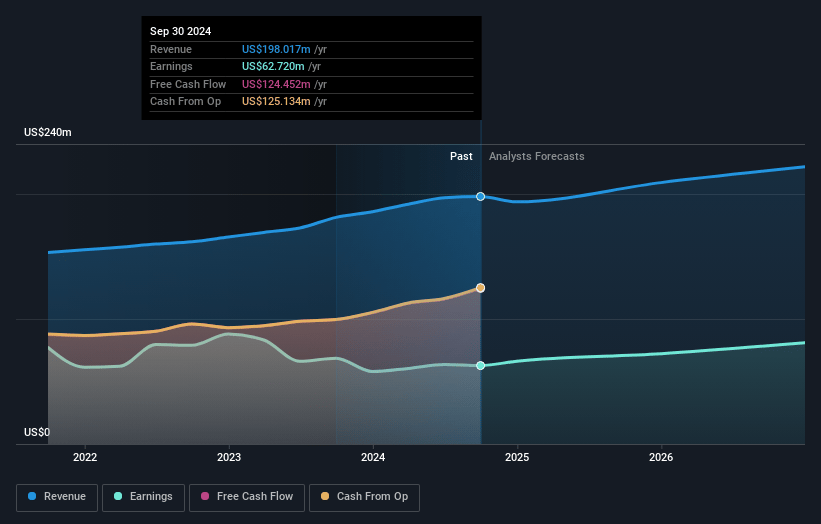

Getty Realty Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Getty Realty's revenue will grow by 4.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 32.1% today to 38.1% in 3 years time.

- Analysts expect earnings to reach $88.7 million (and earnings per share of $1.33) by about April 2028, up from $66.4 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 27.6x on those 2028 earnings, up from 23.3x today. This future PE is lower than the current PE for the US Retail REITs industry at 31.6x.

- Analysts expect the number of shares outstanding to grow by 2.73% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.46%, as per the Simply Wall St company report.

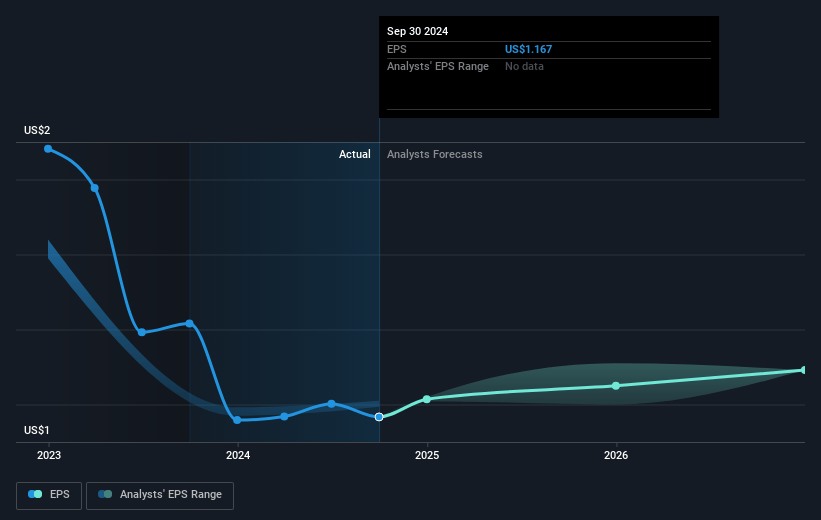

Getty Realty Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The economic and political uncertainty has led to significant volatility in the transaction and capital markets, which may create headwinds for closing deals in Getty Realty's target retail sectors. This could impact potential future revenue streams from new acquisitions.

- The Zips Car Wash bankruptcy highlighted tenant credit risk, and although actions are being taken to reposition affected assets, there is a chance that event-driven disruptions could lead to gaps in rental income, affecting revenue.

- With 85% of the investment pipeline consisting of development funding transactions, potential delays in construction due to macroeconomic challenges such as inflation or cost increases could impact the timeline for generating new revenue streams, impacting revenue and earnings.

- Getty’s reliance on long-term leases means changes in tenant creditworthiness or economic backwardness could affect cash flows from current lease agreements, posing risks to both revenue stability and net margins.

- Continued discussions around increased tariffs and supply chain disruptions may raise tenant operating costs, potentially impacting their profitability and ability to meet rent obligations, risking Getty Realty's revenue and net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $32.857 for Getty Realty based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $232.9 million, earnings will come to $88.7 million, and it would be trading on a PE ratio of 27.6x, assuming you use a discount rate of 7.5%.

- Given the current share price of $27.91, the analyst price target of $32.86 is 15.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.