Key Takeaways

- Effective capture of leasing spreads and renewal activities is driving revenue and net margin growth due to tenant demand and strategic tenant replacements.

- Strategic reinvestments and strong tenant credit profiles provide a foundation for significant growth momentum, increasing traffic and enhancing future earnings.

- Economic challenges and tenant bankruptcies pose risks to revenue and profit margins, while redevelopment projects face cost and execution uncertainties impacting leasing revenue growth.

Catalysts

About Brixmor Property Group- Brixmor (NYSE: BRX) is a real estate investment trust (REIT) that owns and operates a high-quality, national portfolio of open-air shopping centers.

- Brixmor Property Group is effectively capturing leasing spreads and renewal activities, driven by tenant demand for their well-located centers and low rent basis. This is expected to positively impact revenue growth.

- The company is succeeding in backfilling space from recent bankruptcies with better tenants at higher rents, particularly in core categories like grocery and quick-serve restaurants, which should enhance net margins.

- The robust in-legal leasing pipeline and stacking of commenced rents signal significant growth momentum into 2025 and 2026, providing forward visibility on revenue and earnings growth.

- Brixmor is capitalizing on reinvestment projects, delivering them on time and on budget with high returns, expected to transform centers and drive traffic growth, thereby increasing net margins.

- Strong credit profiles of key tenants, combined with reduced leverage and available liquidity, position Brixmor to seize future growth opportunities through strategic investments, potentially increasing earnings.

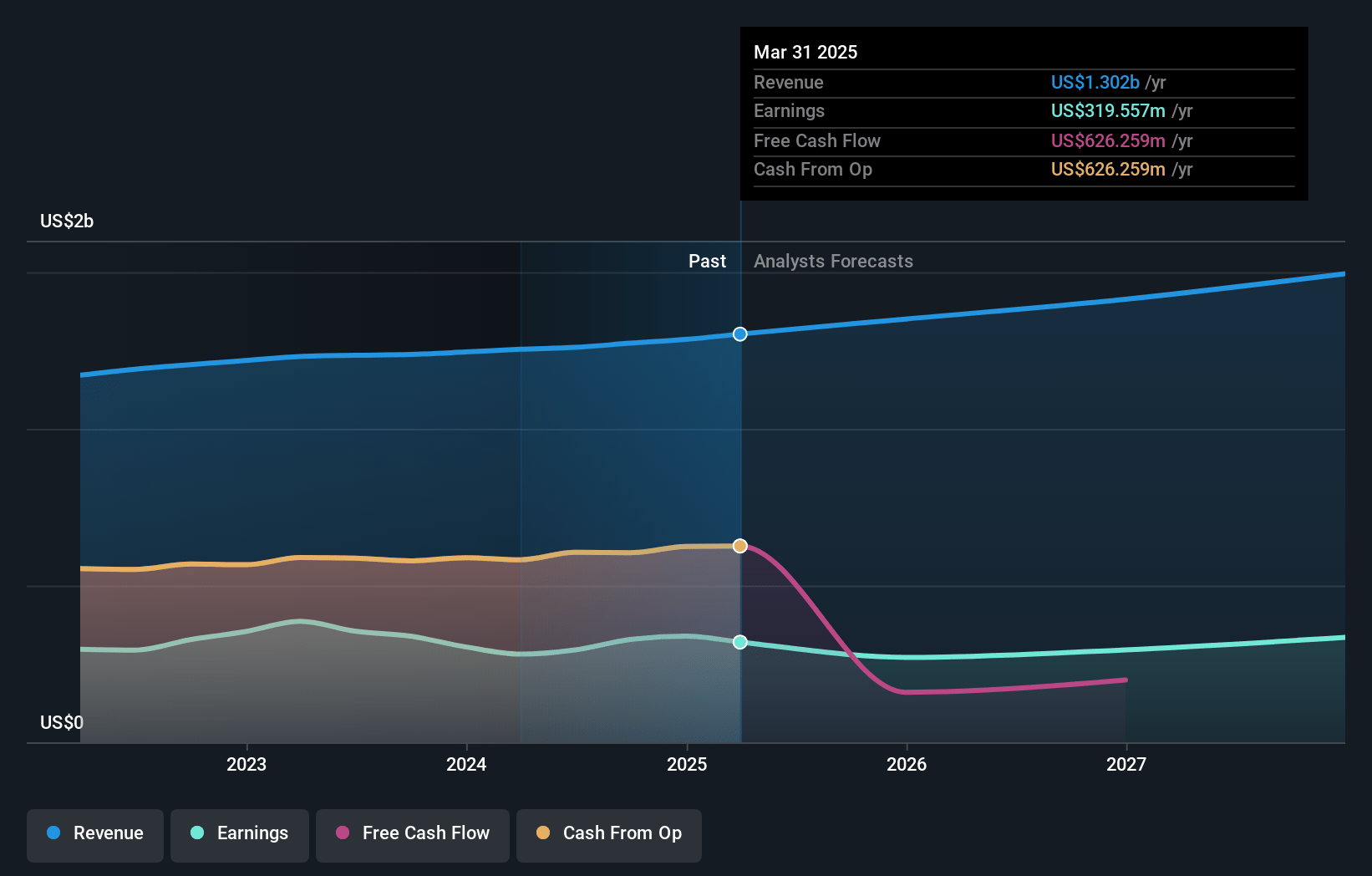

Brixmor Property Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Brixmor Property Group's revenue will grow by 4.8% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 24.5% today to 20.2% in 3 years time.

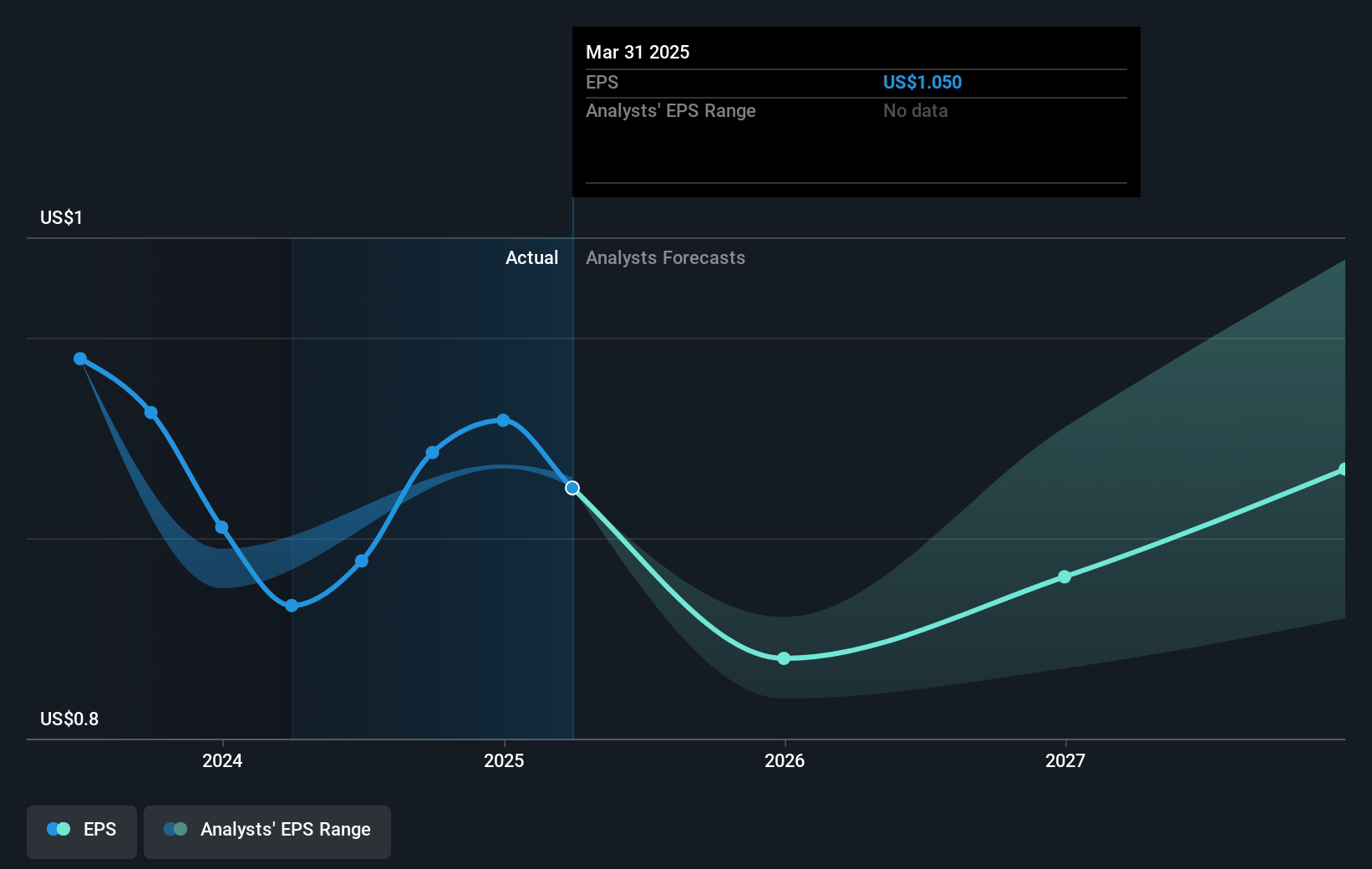

- Analysts expect earnings to reach $303.0 million (and earnings per share of $0.98) by about May 2028, down from $319.6 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 39.9x on those 2028 earnings, up from 24.1x today. This future PE is greater than the current PE for the US Retail REITs industry at 28.4x.

- Analysts expect the number of shares outstanding to grow by 1.58% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.59%, as per the Simply Wall St company report.

Brixmor Property Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The potential for an economic slowdown and looming tariff uncertainty are highlighted as significant risks, which could negatively impact tenant demand and subsequently affect Brixmor's revenue and earnings.

- The company is experiencing tenant disruption from bankruptcies, such as Big Lots and Party City, which is already resulting in a decline in occupancy. Ongoing or additional tenant bankruptcies could further disrupt revenue streams and impact net margins.

- The continued need for capital reinvestment in redevelopment projects, while beneficial, carries execution risk and may result in higher-than-expected expenses, potentially impacting net margins.

- There is an ongoing risk of increased materials or construction costs due to tariffs, which could impact the cost efficiency of tenant improvements and redevelopment costs, negatively affecting profit margins.

- Brixmor's reliance on securing better tenants at higher rents to offset space vacated by bankrupt tenants involves risk, particularly if economic conditions deter tenant expansions, potentially impacting leasing revenue growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $30.324 for Brixmor Property Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $39.0, and the most bearish reporting a price target of just $26.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.5 billion, earnings will come to $303.0 million, and it would be trading on a PE ratio of 39.9x, assuming you use a discount rate of 7.6%.

- Given the current share price of $25.15, the analyst price target of $30.32 is 17.1% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.