Key Takeaways

- Agree Realty's expanded investment guidance and strong liquidity position enable it to capitalize on market opportunities and potentially improve net margins.

- Proactive lease management and recession-resistant acquisition strategies are designed to bolster revenue stability and margins, ensuring growth and resilience.

- The volatile macroeconomic and interest rate environment poses risks to investment strategies, revenue growth, and net margins, especially with tenant and sector-specific exposure.

Catalysts

About Agree Realty- A publicly traded real estate investment trust that is RETHINKING RETAIL through the acquisition and development of properties net leased to industry-leading, omni-channel retail tenants.

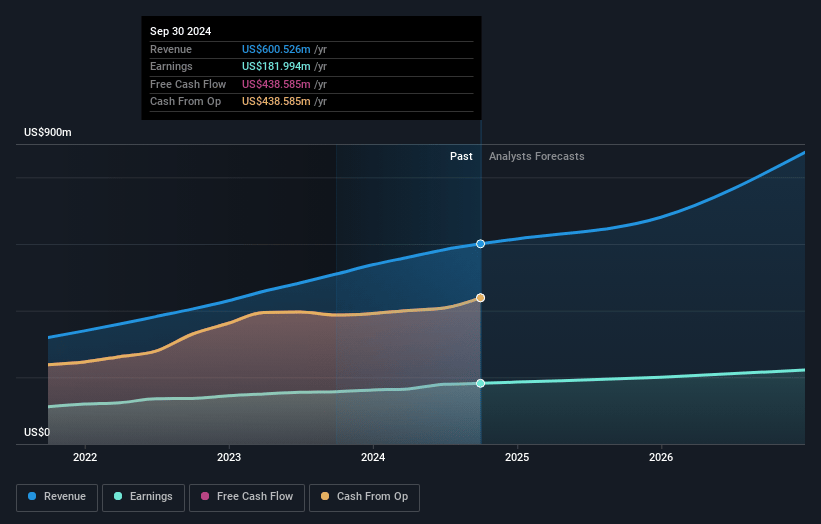

- Agree Realty has increased its investment guidance for 2025 from a range of $1.1 billion to $1.3 billion up to $1.3 billion to $1.5 billion. At the midpoint, this represents a 47% increase over the previous year, which is expected to significantly boost the company's revenue.

- The company maintains a strong balance sheet with $1.9 billion in liquidity and $1.2 billion of hedged capital, allowing it to take advantage of market dislocations. This strategic position is likely to impact net margins positively as the company can invest efficiently amidst volatility.

- Agree Realty's proactive lease management, such as re-leasing former Big Lots locations to higher-rent-paying tenants like Aldi, is expected to drive net effective rental lifts of up to 150%. This is poised to enhance earnings by maximizing lease revenues and improving margins.

- The company has a diverse acquisition strategy focusing on recession-resistant, necessity-based retailers, which may insulate them against economic downturns and ensure stable, recurring revenue streams. This strategic approach is likely to support earnings growth and stability.

- Agree Realty's investments in systems improvements and the addition of over a dozen new team members are expected to streamline operations and increase efficiencies, potentially enhancing net margins through optimized processes and reducing operating costs.

Agree Realty Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Agree Realty's revenue will grow by 13.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 28.8% today to 29.7% in 3 years time.

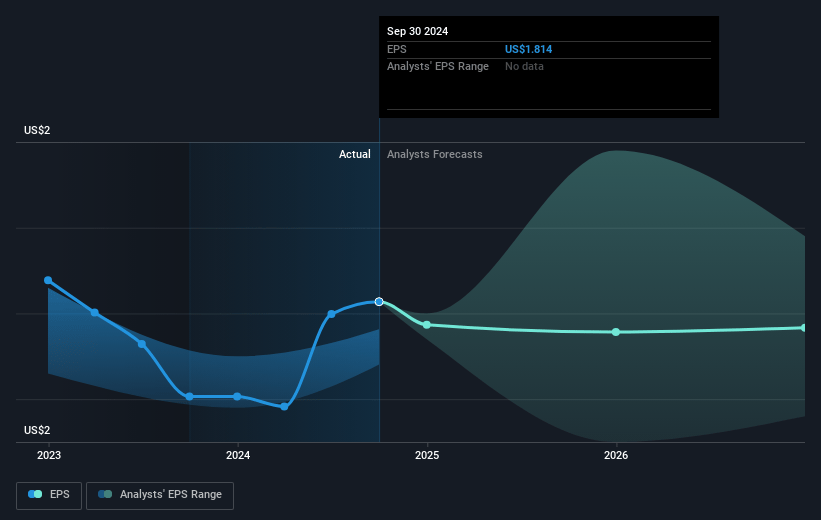

- Analysts expect earnings to reach $279.4 million (and earnings per share of $2.05) by about May 2028, up from $183.4 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $321.6 million in earnings, and the most bearish expecting $194.6 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 48.2x on those 2028 earnings, up from 45.9x today. This future PE is greater than the current PE for the US Retail REITs industry at 28.4x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.04%, as per the Simply Wall St company report.

Agree Realty Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The macroeconomic environment remains volatile and unpredictable, which may lead to risks in executing the investment strategies and affect future revenue growth.

- While tariffs continue to evolve, affecting various industries, the company may face unforeseen challenges that could impact net margins, particularly if larger retailers dominate the market at the cost of smaller ones.

- Concerns over tenant exposure in sectors like dollar stores and pharmacies, which have seen a decline, suggest potential revenue risks if these areas face further market challenges.

- Interest rate volatility and the inherent risks of leveraging forward equity positions could impact earnings if macroeconomic conditions shift unfavorably.

- The focus on expanding investments and relying on commercial paper programs could expose the company to short-term capital risks if market conditions deteriorate, potentially affecting net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $81.975 for Agree Realty based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $940.7 million, earnings will come to $279.4 million, and it would be trading on a PE ratio of 48.2x, assuming you use a discount rate of 7.0%.

- Given the current share price of $76.66, the analyst price target of $81.98 is 6.5% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.