Key Takeaways

- Sabra anticipates increased investment deals suggesting potential revenue growth, supported by their acquisition pipeline and cost of capital.

- Improved senior housing occupancy and effective labor strategies are expected to enhance revenue, cash flow, and net margins.

- Potential Medicaid cuts and regulatory changes threaten Sabra's earnings, while competition, labor costs, and rising interest rates challenge margins and strategic acquisitions.

Catalysts

About Sabra Health Care REIT- As of September 30, 2024, Sabra’s investment portfolio included 373 real estate properties held for investment (consisting of (i) 233 skilled nursing/transitional care facilities, (ii) 39 senior housing communities (“senior housing - leased”), (iii) 68 senior housing communities operated by third-party property managers pursuant to property management agreements (“senior housing - managed”), (iv) 18 behavioral health facilities and (v) 15 specialty hospitals and other facilities), 14 investments in loans receivable (consisting of three mortgage loans and 11 other loans), five preferred equity investments and two investments in unconsolidated joint ventures.

- Sabra is expecting a higher volume of investment deals in 2025, which suggests potential revenue growth as their acquisition pipeline appears robust and their cost of capital supports pursuing these opportunities.

- Senior housing occupancy and margins are improving, with SHOP cash NOI up 17.9% for the quarter, which is likely to positively impact revenue and cash flow.

- The political environment, specifically Medicaid cuts, is being managed with active lobbying, reducing risk and potentially stabilizing future expenses and revenue streams from government reimbursements.

- Sabra’s operators are implementing strategies to stabilize labor challenges, which should help keep labor costs under control, improving net margins.

- The expected sequential cash NOI growth in the senior housing portfolio projects continued steady earnings growth, as revenue growth outpaces expense growth.

Sabra Health Care REIT Future Earnings and Revenue Growth

Assumptions

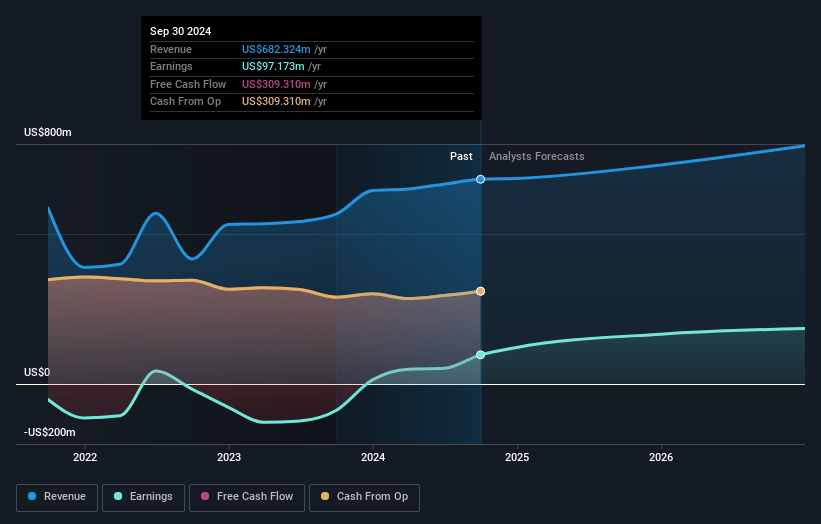

How have these above catalysts been quantified?- Analysts are assuming Sabra Health Care REIT's revenue will grow by 4.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 18.0% today to 24.7% in 3 years time.

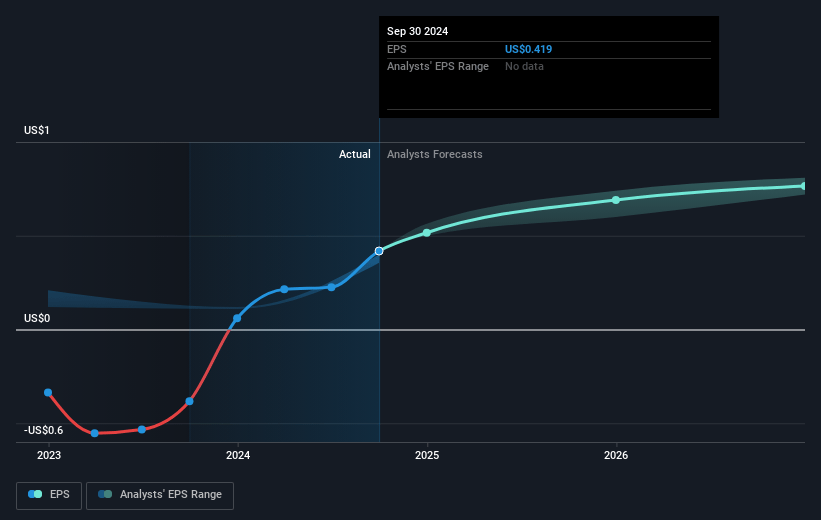

- Analysts expect earnings to reach $195.8 million (and earnings per share of $0.8) by about March 2028, up from $126.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 32.8x on those 2028 earnings, down from 33.4x today. This future PE is lower than the current PE for the US Health Care REITs industry at 35.9x.

- Analysts expect the number of shares outstanding to grow by 2.77% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.13%, as per the Simply Wall St company report.

Sabra Health Care REIT Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The threat of Medicaid cuts poses a significant risk, as any reduction in funding could adversely impact coverage in Sabra's skilled nursing facilities, potentially affecting revenue and margins.

- A robust skilled nursing transaction market with a lot of financial capital chasing deals creates competitive pressure, potentially affecting Sabra's acquisition strategy and increasing the cost of acquiring assets, impacting their net margins.

- Operational challenges, such as workforce availability and labor costs, remain a concern in the senior housing sector, affecting Sabra's ability to manage expenses and maintain earnings growth.

- Rising interest rates could dampen refinancing and acquisition opportunities by increasing capital costs, potentially affecting net income and cash flow projections.

- An uncertain political and regulatory environment, such as potential changes in healthcare policies, may impact Sabra's future earnings, especially if there is an adverse effect on Medicaid and Medicare reimbursements.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $19.667 for Sabra Health Care REIT based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $792.0 million, earnings will come to $195.8 million, and it would be trading on a PE ratio of 32.8x, assuming you use a discount rate of 8.1%.

- Given the current share price of $17.78, the analyst price target of $19.67 is 9.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.