Last Update01 May 25

Key Takeaways

- Strategic growth in InsurTech and improved catastrophe management drive revenue and profitability, with efficient risk management strengthening margins.

- Project Manifest aims to boost revenue by leveraging excess capital, while technology upgrades improve operational efficiency and earnings.

- Delays in California rate approvals and underestimated risks in wildfire models threaten margins and financial performance, while strategic shifts may not deliver expected growth or efficiency gains.

Catalysts

About Global Indemnity Group- Through its subsidiaries, provides specialty property and casualty insurance, and reinsurance products worldwide.

- Strong growth in key segments such as InsurTech (expected to continue growing at 17%) and wholesale commercial (expected to grow at 12%), coupled with an 83% increase in the assumed reinsurance operation, is expected to drive revenue growth. This indicates positive momentum for future revenue increases.

- Continued focus on underwriting excellence with a full-year 94.4% underwriting result in 2024, plus improvements in reserve margins and loss ratios, suggests that Global Indemnity Group is well-positioned to improve net margins through efficient risk management and pricing above inflation.

- Efforts to reduce catastrophe losses through better management of exposures and improved modeling could reduce future losses and improve net margins. A reported 26% reduction in catastrophe losses in 2024 from 2023 points to future gains in profitability.

- Project Manifest, which includes hiring key talent and expanding product offerings, aims to make better use of excess capital, leading to higher revenue and potentially better earnings from new underwriting opportunities.

- The completed transformation to new technology systems, with the transition to the cloud expected to conclude by 2025, is expected to improve operating efficiencies, reduce the expense ratio, and contribute to higher net margins and earnings through improved service and processing capabilities.

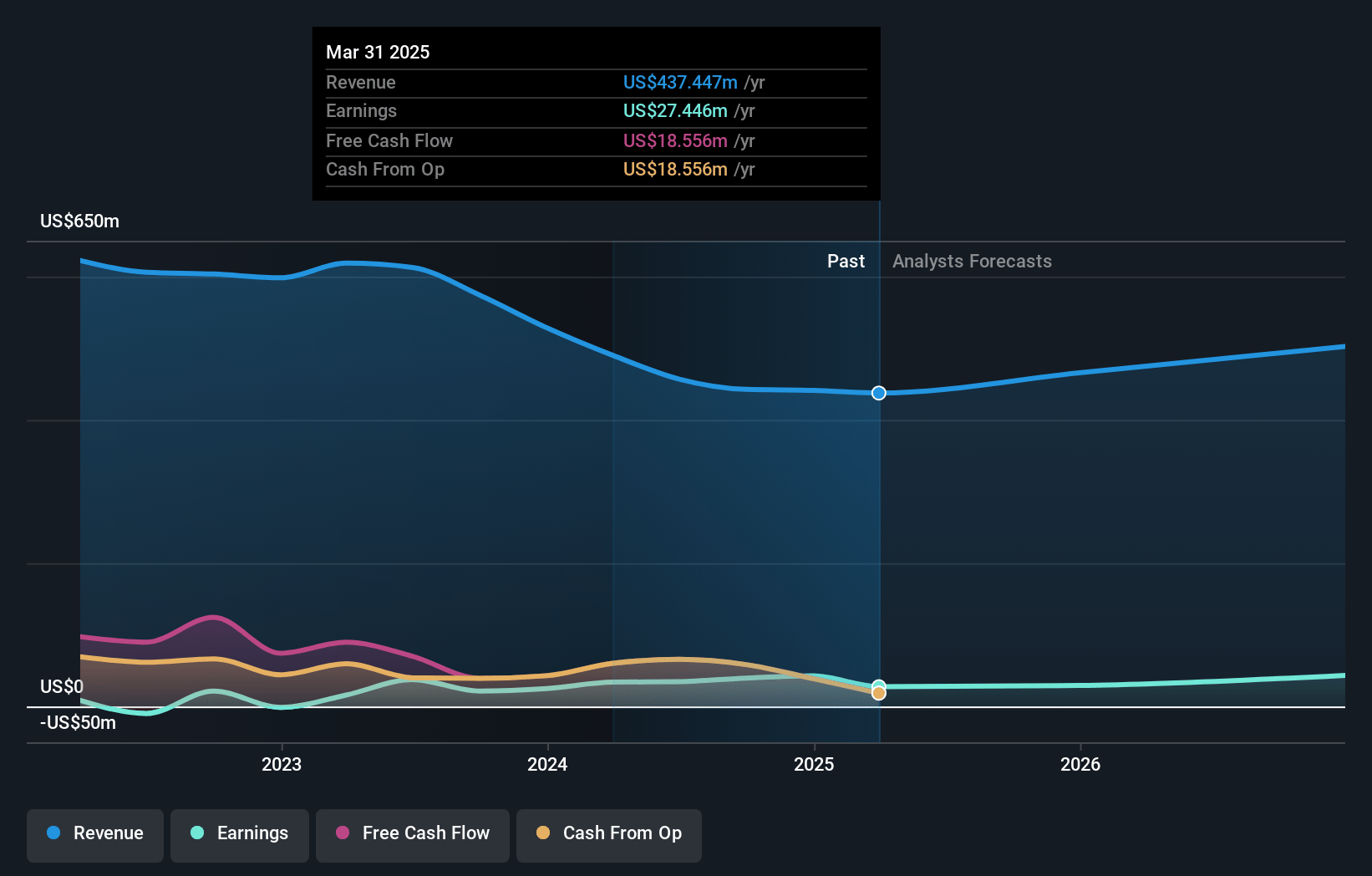

Global Indemnity Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Global Indemnity Group's revenue will grow by 10.4% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 9.7% today to 8.5% in 3 years time.

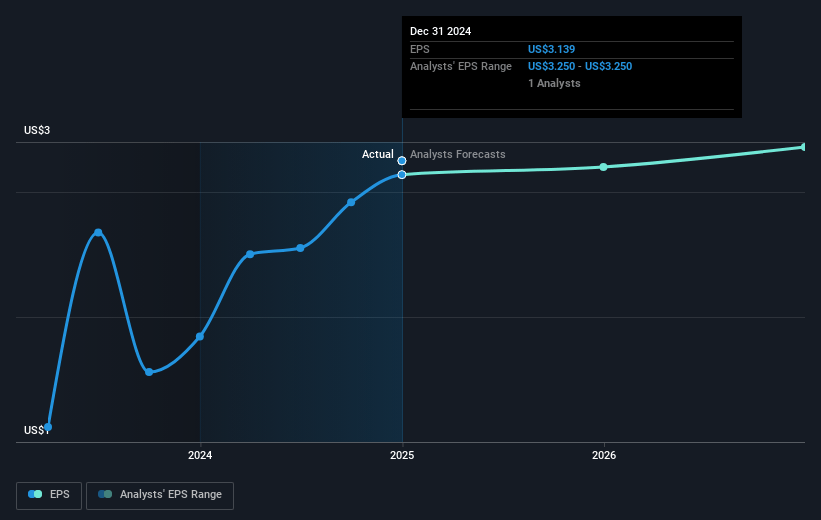

- Analysts expect earnings to reach $50.6 million (and earnings per share of $3.47) by about May 2028, up from $42.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 20.8x on those 2028 earnings, up from 9.6x today. This future PE is greater than the current PE for the US Insurance industry at 14.1x.

- Analysts expect the number of shares outstanding to grow by 4.81% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.21%, as per the Simply Wall St company report.

Global Indemnity Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The reliance on regulatory approval in California for rate increases, which has been stalled, could impact profit margins if the company fails to obtain necessary rate hikes to cover increasing wildfire exposures. This affects both underwriting margins and net income.

- The reliance on catastrophe models, which underestimated the magnitude of the Los Angeles wildfires, indicates potential risk in underwriting accuracy that could lead to unexpected losses. This impacts underwriting performance and reserve adequacy.

- The decision to prioritize growth through product expansion over share buybacks might not yield immediate returns, risking potential shareholder dissatisfaction if anticipated growth does not materialize. This impacts equity returns and potentially book value per share.

- High expense ratios, although partially addressed by Project Manifest, remain a concern and might affect the company's ability to compete efficiently, especially if expenses do not decrease as projected. This affects operating margins and overall profitability.

- The ongoing technology investments and structural changes, such as Project Manifest, have yet to demonstrate clear financial returns, posing a risk if the anticipated efficiencies and growth do not occur. This impacts operational efficiency and could pressure net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $55.0 for Global Indemnity Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $592.9 million, earnings will come to $50.6 million, and it would be trading on a PE ratio of 20.8x, assuming you use a discount rate of 6.2%.

- Given the current share price of $28.96, the analyst price target of $55.0 is 47.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.