Narratives are currently in beta

Key Takeaways

- Growth in online sales channels and strategic geographic expansions are key to increasing Coty's future revenue and market share.

- Cost-saving measures, supply chain optimization, and a deleveraging strategy are expected to improve margins and shareholder returns.

- Coty faces risks from retail inventory dynamics, Asian market volatility, tariff impacts, and beauty market growth shifts, affecting revenue and investor confidence.

Catalysts

About Coty- Manufactures, markets, distributes, and sells beauty products worldwide.

- Coty is experiencing significant growth in its online sales channels, driven by increased consumer trust in platforms like Amazon and strong advocacy marketing efforts, which are expected to boost future revenue streams.

- The company anticipates improvements in gross and EBITDA margins due to rigorous cost-saving initiatives, productivity measures, and the implementation of a centralized planning hub to optimize supply chain efficiency.

- Coty's strategic focus on expanding into the skin care category and new geographic regions, along with the launch of new licenses and products, is expected to drive revenue growth and market share gains.

- The company is poised to leverage strong innovation pipelines in both mass and prestige fragrances, which will sustain earnings growth by tapping into white spaces in these segments.

- Coty's deleveraging strategy remains a priority, with plans to reduce leverage ratios, enhancing free cash flow and potentially increasing shareholder returns and earnings per share.

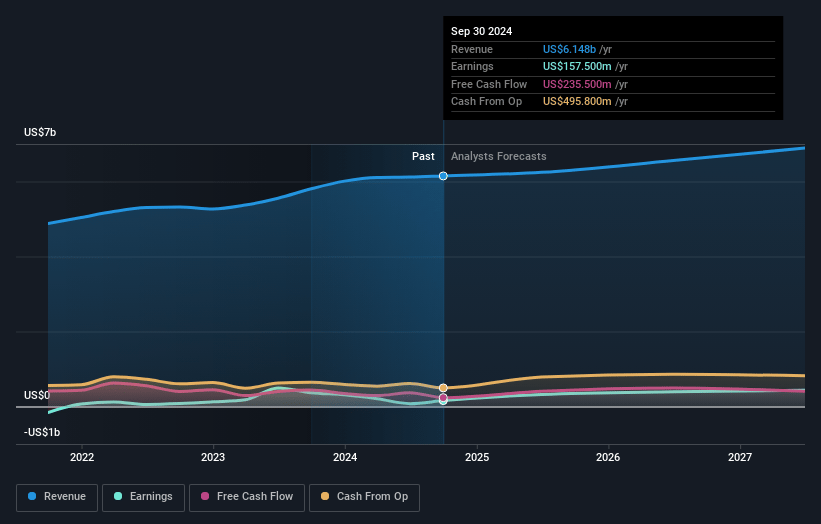

Coty Future Earnings and Revenue Growth

Assumptions

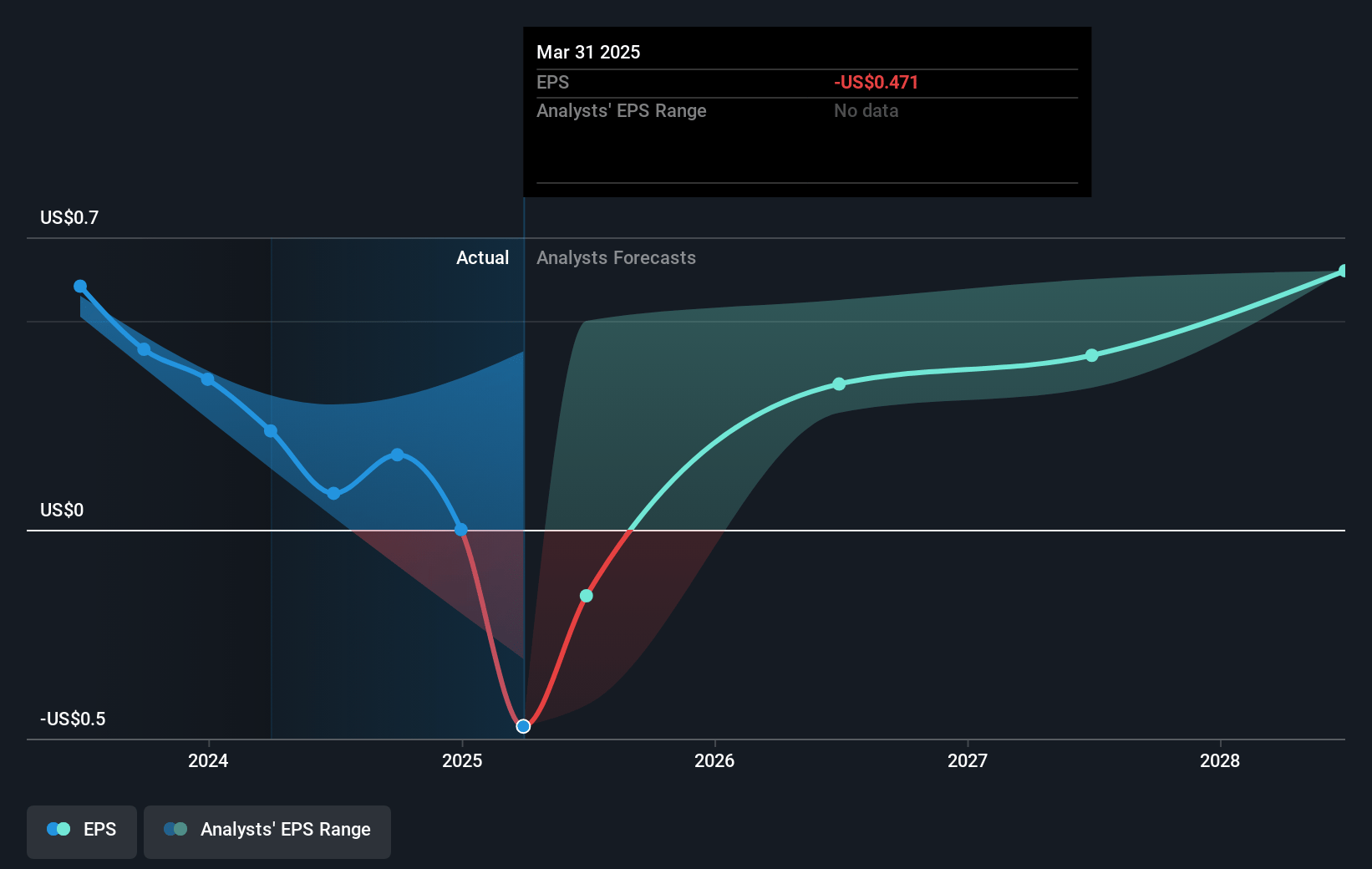

How have these above catalysts been quantified?- Analysts are assuming Coty's revenue will grow by 4.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 2.6% today to 6.7% in 3 years time.

- Analysts expect earnings to reach $469.8 million (and earnings per share of $0.59) by about November 2027, up from $157.5 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $531 million in earnings, and the most bearish expecting $360 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 22.4x on those 2027 earnings, down from 41.3x today. This future PE is lower than the current PE for the US Personal Products industry at 26.8x.

- Analysts expect the number of shares outstanding to decline by 2.75% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.08%, as per the Simply Wall St company report.

Coty Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- There may be uncertainty surrounding Coty's medium-term outlook, as investors have noted confusion about any potential shifts in growth algorithms, which may impact revenue forecasts and investor confidence.

- There are potential risks associated with retailer inventory levels and sell-in vs. sell-out dynamics, particularly if retailers have overstocked during the holiday season, which could negatively impact revenue growth.

- Coty's exposure to fluctuations in the Asian market, particularly China and Travel Retail Asia, can be a significant risk, as these regions have shown volatile performance, impacting overall revenue and growth prospects.

- Any imposition of new tariffs, particularly on imported goods to the U.S., could affect Coty's cost structure, potentially impacting net margins if production isn't adjusted or pricing strategies aren't effectively implemented.

- A potential slowdown or shift in the overall beauty market growth could pose a risk to Coty's ability to maintain or exceed industry performance, potentially affecting revenue targets and EBITDA growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $10.44 for Coty based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $15.0, and the most bearish reporting a price target of just $7.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $7.0 billion, earnings will come to $469.8 million, and it would be trading on a PE ratio of 22.4x, assuming you use a discount rate of 8.1%.

- Given the current share price of $7.47, the analyst's price target of $10.44 is 28.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives