Narratives are currently in beta

Key Takeaways

- Ongoing innovation in laundry and personal care products, including new premium offerings, is expected to drive sales growth and expand market share globally.

- Strategic international market expansion and increased marketing investments aim to enhance brand visibility, supporting pricing power and future revenue growth.

- Weak performance in gummy vitamins and increased promotion in litter threaten revenue growth, margins, and stability amid competitive pressures and declining consumption trends.

Catalysts

About Church & Dwight- Develops, manufactures, and markets household, personal care, and specialty products.

- Church & Dwight's ongoing innovation in the laundry detergent category with new products like ARM & HAMMER Deep Clean and POWER SHEETS is expected to drive future sales growth as these products capture consumer interest and expand market share. This focus on premium product offerings is likely to positively impact revenue.

- The company's expansion efforts in international markets, evidenced by organic growth of 8.1% in Q3 within its International business, underscores its strategy of leveraging global market opportunities, which could significantly enhance future revenue streams.

- Continued growth and market share gains of power brands like BATISTE and THERABREATH, along with new product introductions such as BATISTE Sweat Activated and THERABREATH Deep Clean Oral Rinse, suggest a strong pipeline for long-term revenue growth across various personal care categories.

- Church & Dwight's commitment to increased marketing investment, projected to exceed 11% of sales, aims to sustain and enhance market share gains. This strategic spending could bolster brand visibility and support pricing power, potentially improving net margins and sales volume.

- Stabilization actions within the underperforming Gummy Vitamins business, including new packaging, upgraded formulas, and increased marketing investments, offer potential for turnaround and eventual profit growth in 2025, positively impacting overall earnings.

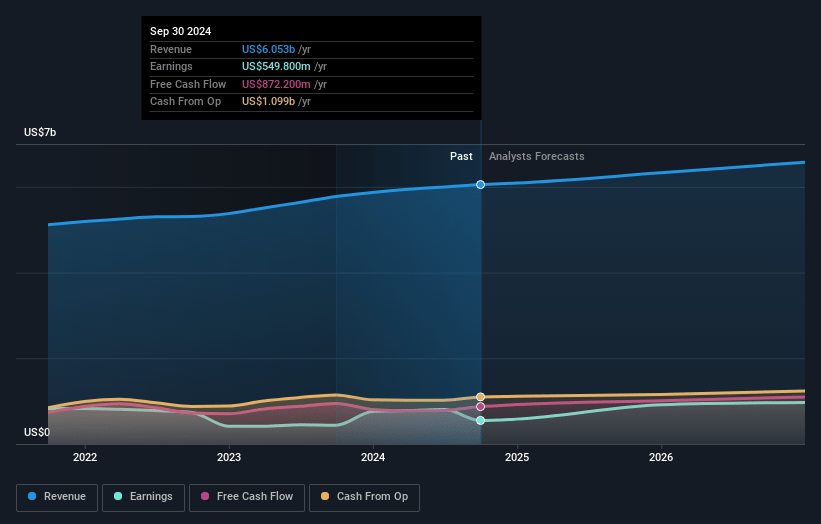

Church & Dwight Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Church & Dwight's revenue will grow by 3.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 9.1% today to 14.8% in 3 years time.

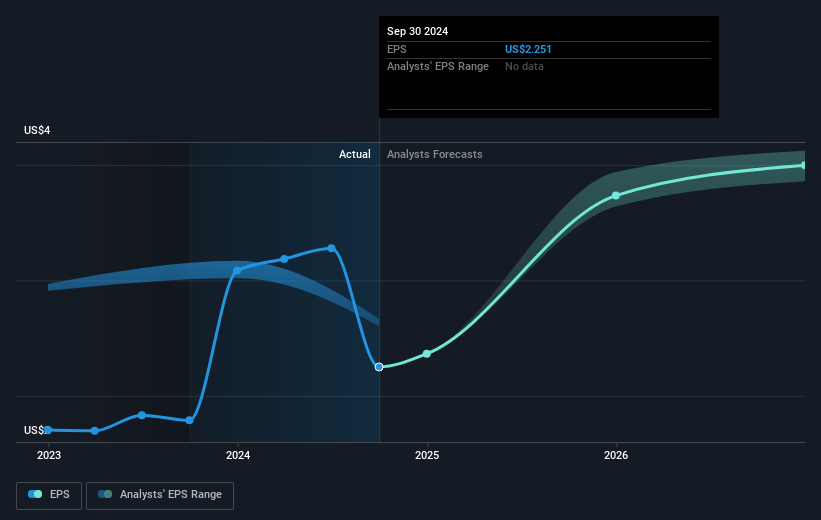

- Analysts expect earnings to reach $1.0 billion (and earnings per share of $4.19) by about November 2027, up from $549.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 30.1x on those 2027 earnings, down from 47.8x today. This future PE is greater than the current PE for the US Household Products industry at 17.9x.

- Analysts expect the number of shares outstanding to decline by 0.84% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.92%, as per the Simply Wall St company report.

Church & Dwight Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The Gummy Vitamins business continues to be a drag on organic growth, with a significant decline in consumption leading to reduced long-term growth and profit expectations. This resulted in a $357 million write-down, indicating potential continued issues impacting revenues and margins.

- The vitamin impairment led to a reported loss per share for the quarter, highlighting ongoing weaknesses that could impact future earnings if not addressed.

- Increasing promotional levels, particularly in the Litter category, driven by competitor actions, could pressure margins and compromise profitability if the company chooses to match promotions to maintain market share.

- Observations of slowing category consumption trends in certain products like liquid laundry detergent and litter, even with overall advancements, suggest potential risks to achieving expected revenue growth rates in a competitive and cautious market environment.

- A more fragile state in core categories, compounded by a perceived reliance on the growth of certain brands like THERABREATH and HERO, may challenge broader growth expectations and put additional pressure on margins and earnings stability if other legacy segments do not perform as expected.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $106.46 for Church & Dwight based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $124.0, and the most bearish reporting a price target of just $68.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $6.8 billion, earnings will come to $1.0 billion, and it would be trading on a PE ratio of 30.1x, assuming you use a discount rate of 5.9%.

- Given the current share price of $107.26, the analyst's price target of $106.46 is 0.8% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives