Key Takeaways

- Strong growth in Milk Makeup and Obagi Medical, with store expansion and innovation driving increased future revenue and market share.

- Operational efficiencies and improved cash flow enhance financial flexibility, allowing for further sales and marketing investments, boosting top-line growth.

- Regulatory investigation, macroeconomic factors, and strategic execution risks challenge Waldencast's liquidity, revenue growth, and profitability, requiring careful management and optimization of strategic initiatives.

Catalysts

About Waldencast- Operates in the beauty and wellness industry in the United States, Canada, Europe, the Middle East, India, Australia, and New Zealand.

- Strong growth in both Milk Makeup and Obagi Medical brands, with Milk Makeup expanding into Ulta Beauty stores, leading to expected mid-teens revenue growth. This channel expansion is likely to drive increased future revenue.

- Operational efficiencies and sturdy gross margins facilitated by the Waldencast flywheel effect are expected to provide room for further investments in sales and marketing, aiding top-line momentum, thus impacting future net margins positively.

- Successful execution of innovation strategies, including new product launches in both the skincare and makeup segments, are likely to boost future revenue and market share.

- Securing a new $205 million, 5-year credit facility extends debt maturity and enhances financial flexibility, potentially improving future earnings by reducing financial risks.

- Expected improvements in cash generation following the resolution of nonrecurring regulatory expenses will enable stronger cash flow, which could be utilized for growth investments or debt reduction.

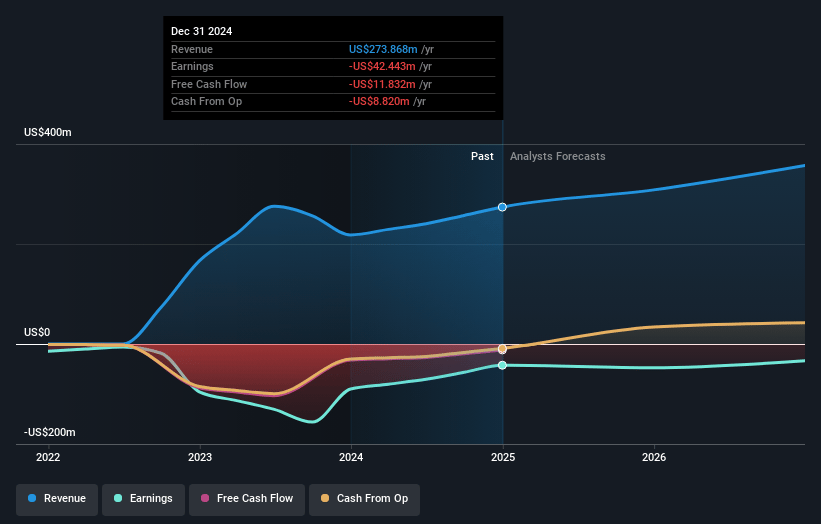

Waldencast Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Waldencast's revenue will grow by 14.6% annually over the next 3 years.

- Analysts are not forecasting that Waldencast will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Waldencast's profit margin will increase from -15.5% to the average US Personal Products industry of 5.5% in 3 years.

- If Waldencast's profit margin were to converge on the industry average, you could expect earnings to reach $22.6 million (and earnings per share of $0.18) by about May 2028, up from $-42.4 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 34.9x on those 2028 earnings, up from -7.2x today. This future PE is greater than the current PE for the US Personal Products industry at 21.3x.

- Analysts expect the number of shares outstanding to grow by 1.45% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.02%, as per the Simply Wall St company report.

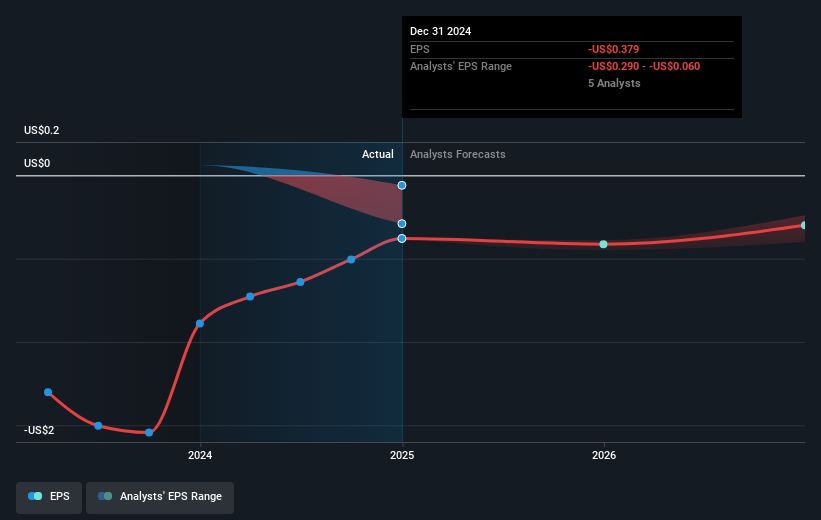

Waldencast Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Waldencast's ongoing regulatory investigation has resulted in significant cash usage for nonrecurring expenses, potentially limiting liquidity and impacting net earnings until the matter is resolved.

- The macroeconomic environment and retail inventory adjustments have led to slowed market growth and could affect revenue growth, especially as competitive and consumer market conditions may change unpredictably.

- The aggressive expansion into Ulta may cannibalize existing sales from Sephora, leading to dilution of revenue per outlet and potentially reducing overall profitability if not managed carefully.

- There is execution risk associated with Milk Makeup's strategic plans, especially as they expand into the complexion category and seek to maintain strong brand equity through new innovation, potentially affecting profit margins if the innovations don't meet market expectations.

- Significant reliance on growth strategies such as marketing investments and international expansion requires careful management of operational costs and investment returns, which, if not optimized, could lead to stagnation in EBITDA margin improvement and overall net profit growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $4.88 for Waldencast based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $6.0, and the most bearish reporting a price target of just $3.4.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $412.3 million, earnings will come to $22.6 million, and it would be trading on a PE ratio of 34.9x, assuming you use a discount rate of 8.0%.

- Given the current share price of $2.74, the analyst price target of $4.88 is 43.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.