Key Takeaways

- Expansion of the MindBody system and enhancements to the Evolve plan are expected to drive significant revenue and profit growth.

- Recruitment of new leadership aims to improve operational efficiencies and boost margins through technology and digital enhancements.

- Supply chain issues, declining international revenue, increased expenses, and the need for significant investments pose risks to future growth and profitability.

Catalysts

About LifeVantage- Engages in the identification, research, development, formulation, and sale of advanced nutrigenomic activators, dietary supplements, nootropics, pre- and pro-biotics, weight management, and skin and hair care products.

- The successful launch of the MindBody GLP-1 system, which has already led to significant revenue growth, is expected to continue driving revenue increases as the product expands its market presence and capitalizes on strong demand.

- The international rollout of the MindBody system in March and achieving the goal of consistent supply will support future revenue growth. Expanding into new markets where the U.S. represents more than 80% of revenue offers significant potential for growth.

- Enhancements to the Evolve compensation plan, including a new sharing bonus and accelerators for new consultants, are expected to drive increased enrollments and enhance revenue and profit growth by broadening the consultant base and channels.

- Strong cross-selling opportunities and increased subscription rates from the MindBody system, along with the amplified benefits of product combinations, are expected to boost both revenue and net margins as customers invest more in complementary products.

- The recruitment of a new Chief Information and Innovation Officer, Todd Thompson, with a strong track record in scaling operations, is expected to enhance operational efficiencies, thus supporting improved net margins and earnings through better technology and digital experience enhancements.

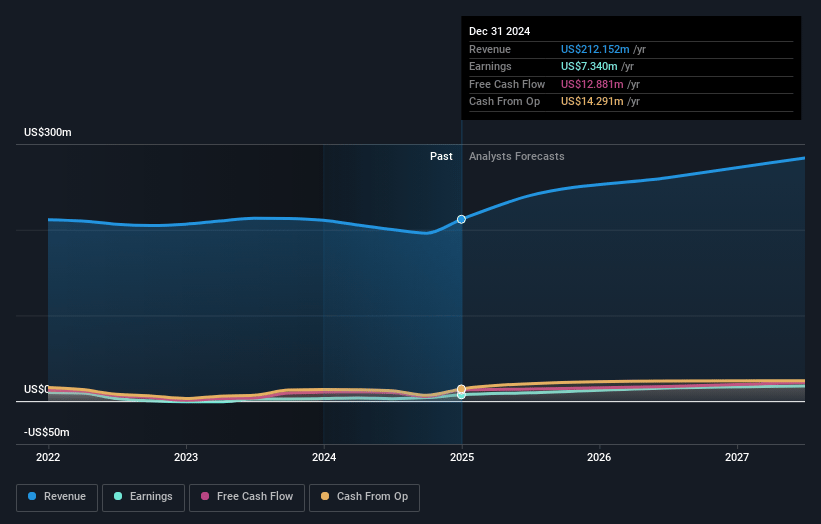

LifeVantage Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming LifeVantage's revenue will grow by 12.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.5% today to 7.3% in 3 years time.

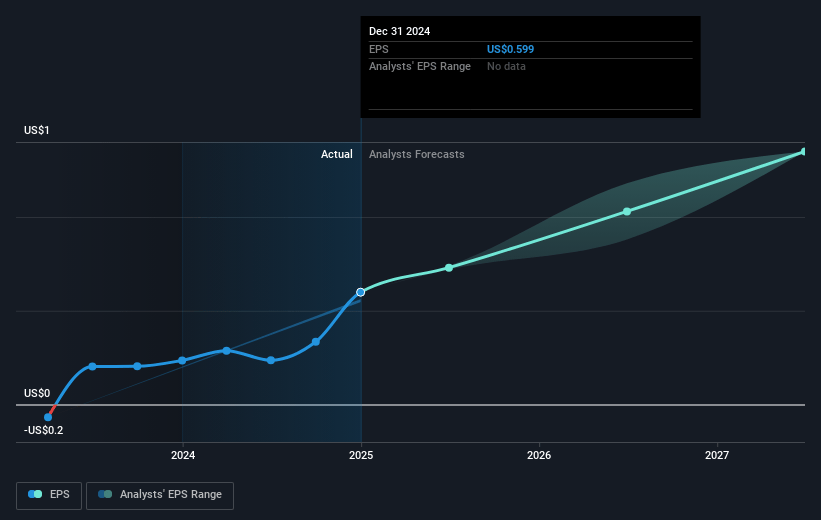

- Analysts expect earnings to reach $22.2 million (and earnings per share of $1.35) by about April 2028, up from $7.3 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 21.5x on those 2028 earnings, up from 21.2x today. This future PE is greater than the current PE for the US Personal Products industry at 21.2x.

- Analysts expect the number of shares outstanding to decline by 1.18% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.0%, as per the Simply Wall St company report.

LifeVantage Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The discontinuation of inventory during the MindBody launch period led to a loss in momentum and potential sales, revealing possible vulnerabilities in supply chain management, which could impact future revenue growth.

- The decline in revenue from Asia Pacific and Europe, driven by a decrease in total active accounts and negative impacts from foreign currency fluctuations, indicates risks in international market performance, potentially impacting overall revenue diversification.

- The increased commission and incentive expenses, resulting from elevated costs associated with promotional programs and changes in revenue mix, could adversely affect profit margins if not managed effectively.

- The need for significant investments in brand awareness, infrastructure, and inventory to support international expansion could potentially strain financial resources and impact net margins if anticipated growth fails to materialize.

- The dependency on the positive reception and continued performance of the new MindBody system and related product stacks could pose risks if consumer interest wanes or competitive products emerge, potentially affecting earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $32.5 for LifeVantage based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $303.2 million, earnings will come to $22.2 million, and it would be trading on a PE ratio of 21.5x, assuming you use a discount rate of 7.0%.

- Given the current share price of $12.4, the analyst price target of $32.5 is 61.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.