Key Takeaways

- Expansion in PFA technology and the Hugo robotic platform are key drivers of Medtronic’s future growth, offering significant revenue opportunities.

- Strategic focus on emerging markets and new technologies like RDN is expected to boost revenue, market share, and operational efficiency.

- Competitive pressures, regulatory delays, and distributor issues could impact Medtronic's market share, revenue growth, margin expansion, and projected earnings.

Catalysts

About Medtronic- Develops, manufactures, and sells device-based medical therapies to healthcare systems, physicians, clinicians, and patients worldwide.

- Medtronic's Cardiac Ablation Solutions business is experiencing rapid growth, with expectations of continued double-digit growth driven by the pulsed field ablation (PFA) technology. This advancement is projected to significantly boost revenue as they expand their PFA portfolio globally.

- The launch and international expansion of Medtronic's Hugo soft tissue robotic platform are on track, which is anticipated to be a growth driver for the Surgical business in fiscal '26 and beyond. Successful deployment and increased utilization could positively impact revenue growth.

- Medtronic's Renal Denervation (RDN) technique for hypertension is poised for U.S. market entry with Medicare coverage anticipated within the next year. This development could serve as a major growth driver, boosting both revenue and market share.

- High growth rates in emerging markets such as India, Eastern Europe, and Southeast Asia suggest that continued expansion in these regions could enhance Medtronic's revenue streams and increase earnings.

- Continued improvements in gross and operating margins through disciplined pricing and COGS (Cost of Goods Sold) efficiency programs are expected to provide leveraged earnings growth and support increased investments in growth drivers.

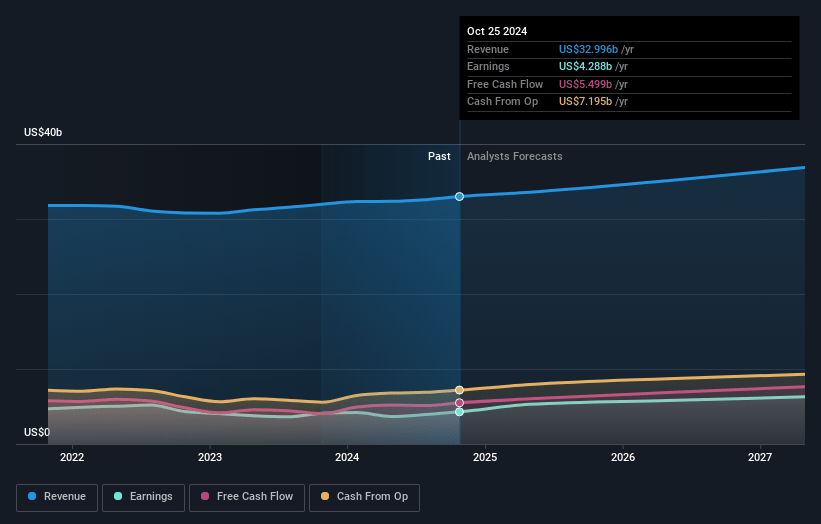

Medtronic Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Medtronic's revenue will grow by 4.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 12.8% today to 16.0% in 3 years time.

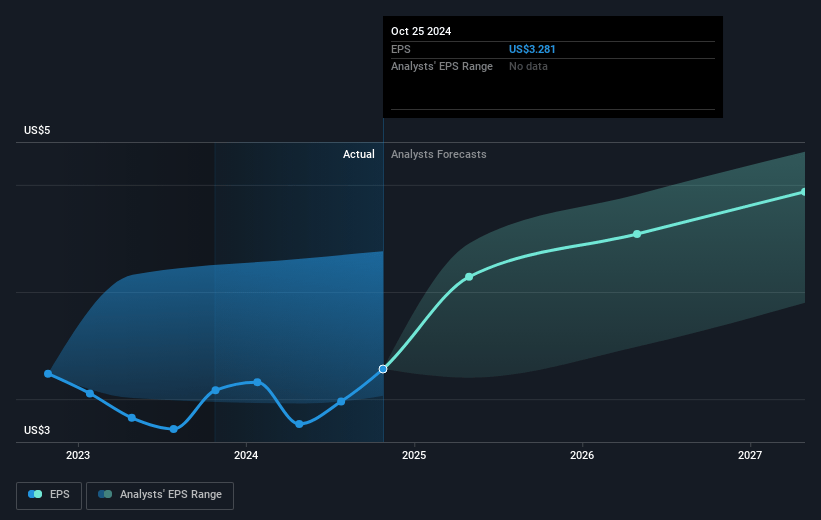

- Analysts expect earnings to reach $6.1 billion (and earnings per share of $4.88) by about April 2028, up from $4.3 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $7.5 billion in earnings, and the most bearish expecting $5.0 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 25.9x on those 2028 earnings, up from 25.5x today. This future PE is lower than the current PE for the US Medical Equipment industry at 31.6x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.35%, as per the Simply Wall St company report.

Medtronic Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- There is a risk related to U.S. distributor dynamics, which recently impacted the Surgical portfolio's performance due to changes in buying patterns. This situation could affect Medtronic's revenue projections if not resolved as anticipated.

- Exchange rate fluctuations have been a headwind and are expected to have a significant financial impact, which could impact gross margins and earnings.

- The lag in the regulatory process for RDN coverage and adoption in the U.S. and other international markets could slow down expected revenue increases in these regions.

- Concerns over execution in integrating new acquisitions and the subsequent balance between investing in growth drivers and margin expansion could affect operating margins and net earnings.

- General competitive pressures, especially in key areas like Surgical Innovations with the lag in the Hugo robotic surgery system, could impact Medtronic's ability to maintain its market share, thus affecting revenue and earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $96.832 for Medtronic based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $112.46, and the most bearish reporting a price target of just $85.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $38.2 billion, earnings will come to $6.1 billion, and it would be trading on a PE ratio of 25.9x, assuming you use a discount rate of 8.4%.

- Given the current share price of $84.6, the analyst price target of $96.83 is 12.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.