Narratives are currently in beta

Key Takeaways

- Expansion of facilities aims to drive revenue growth through increased patient volume and network access.

- Strategic investments and efficiency improvements are set to enhance earnings and profitability amidst rising healthcare demand.

- Operational disruptions from hurricanes, Medicare denial trends, and Medicaid changes pose significant risks to HCA Healthcare's revenue and financial stability.

Catalysts

About HCA Healthcare- Through its subsidiaries, owns and operates hospitals and related healthcare entities in the United States.

- HCA Healthcare's expansion of inpatient beds and outpatient facilities, with plans to add significant capacity and create greater access across their networks, is expected to drive revenue growth through increased patient volume.

- The strategic investments and development projects under way, amounting to approximately $6 billion, should enhance earnings as these projects come online over the next few years and meet the growing demand for healthcare services.

- An anticipated continued volume growth of 3% to 4% in 2025, which exceeds the company's long-term demand assumptions, is expected to contribute positively to future revenue and support earnings growth.

- Efforts to improve operational efficiency, such as the reduction in contract labor and improvements in labor costs, are anticipated to favorably impact net margins, enhancing the profitability of the company.

- Recovery from recent hurricanes, with expectations that affected hospitals will become more productive than pre-storm, suggests potential future revenue and earnings recovery as facilities return to full operation.

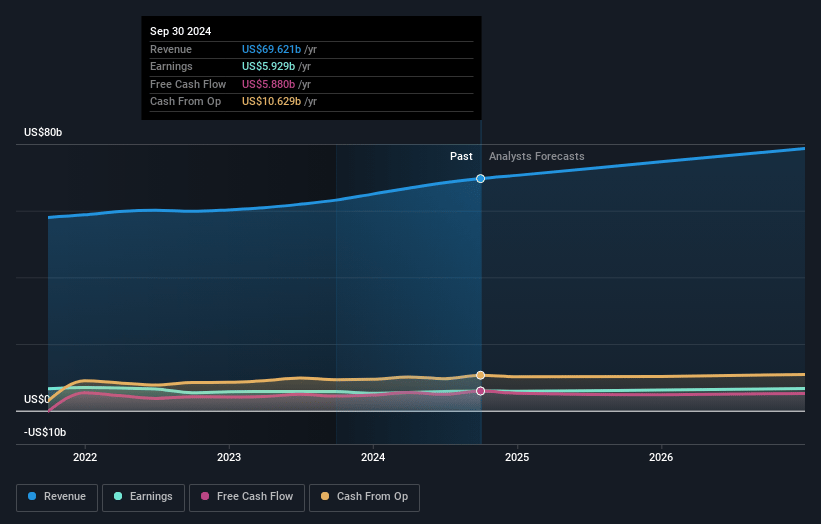

HCA Healthcare Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming HCA Healthcare's revenue will grow by 6.0% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 8.5% today to 8.3% in 3 years time.

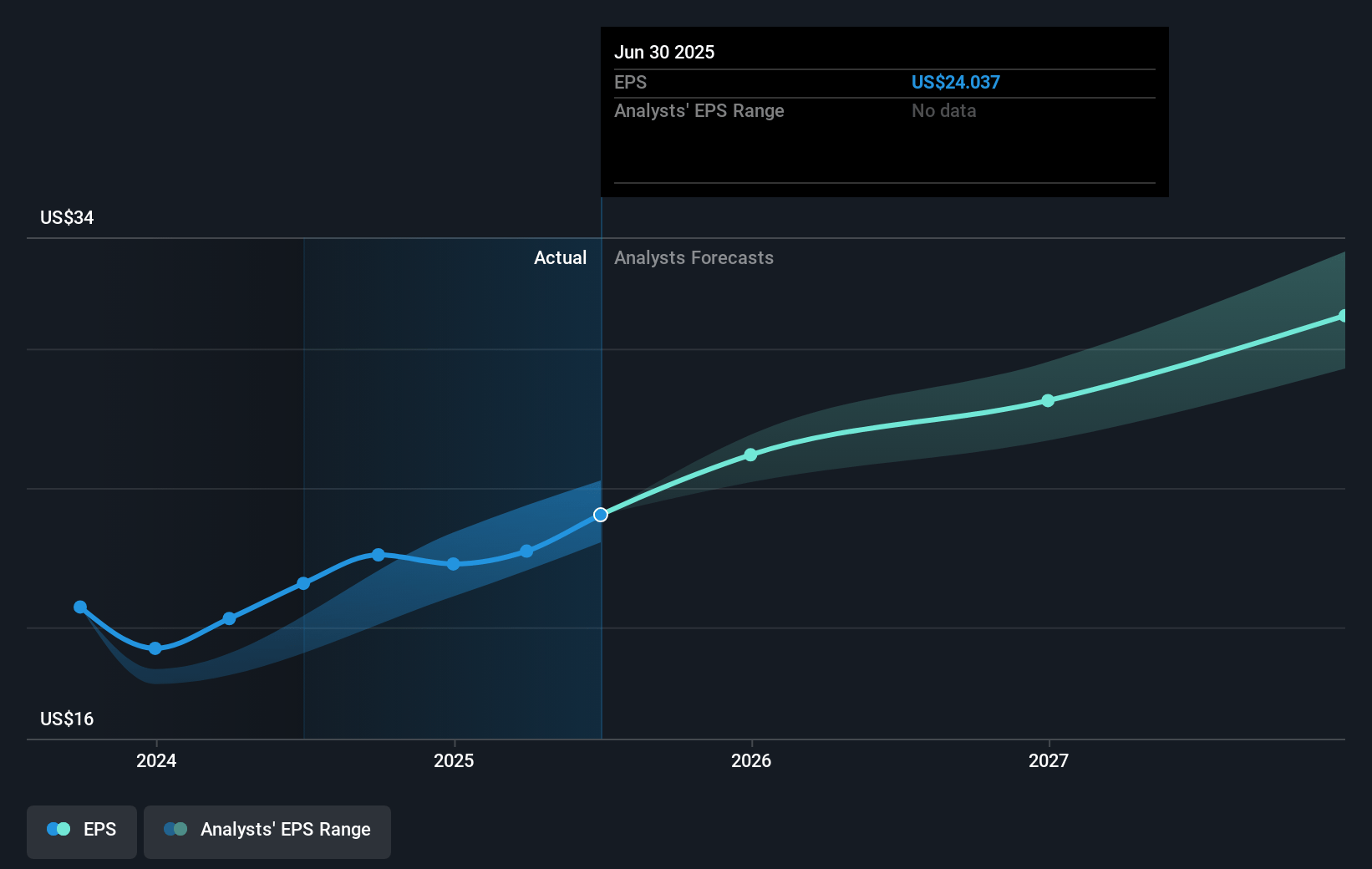

- Analysts expect earnings to reach $6.9 billion (and earnings per share of $30.09) by about November 2027, up from $5.9 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 16.1x on those 2027 earnings, up from 14.9x today. This future PE is lower than the current PE for the US Healthcare industry at 24.8x.

- Analysts expect the number of shares outstanding to decline by 3.19% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.19%, as per the Simply Wall St company report.

HCA Healthcare Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The impact of two major hurricanes on HCA Healthcare's facilities caused significant losses in revenue and increased operating expenses, which could impact net margins.

- There are ongoing operational challenges and expected additional costs due to infrastructure damage at key hospitals, potentially limiting revenue recovery in affected areas.

- The Medicare Advantage denial trends put financial pressure from potentially unpaid claims, especially for short-stay admissions, influencing overall earnings and operational efficiency.

- Ongoing state Medicaid redeterminations and subsequent decline in Medicaid admissions may lead to reduced revenue from this patient segment.

- Prolonged repair timelines and uncertain insurance claim recoveries from hurricane damage introduce risks to cash flow and capital expenditure plans.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $406.3 for HCA Healthcare based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $460.0, and the most bearish reporting a price target of just $316.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $82.9 billion, earnings will come to $6.9 billion, and it would be trading on a PE ratio of 16.1x, assuming you use a discount rate of 6.2%.

- Given the current share price of $349.32, the analyst's price target of $406.3 is 14.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives