Key Takeaways

- Demographic trends and strategic investments in care models position DaVita for long-term growth and margin expansion in the kidney care market.

- Operational resilience, digitalization, and disciplined capital allocation support margin preservation and incremental shareholder value amid regulatory and industry shifts.

- Multiple operational, regulatory, and external challenges threaten DaVita’s profit stability, volume growth, and future earnings predictability across both domestic and international segments.

Catalysts

About DaVita- Provides kidney dialysis services for patients suffering from chronic kidney failure in the United States.

- Demographic factors such as the growing elderly population and continued rise in diabetes and hypertension are expected to expand the chronic kidney disease patient base, which should drive long-term volume growth in treatments and increase future revenue streams.

- DaVita’s continued investment in in-home dialysis, value-based care models, and strategic partnerships (including Integrated Kidney Care and managed care contracts) position the company to benefit from industry trends favoring coordinated, efficient, and higher-margin care, offering potential for net margin expansion and more predictable earnings.

- Regulatory and Medicare reimbursement changes (such as the inclusion of oral phosphate binders in the Medicare bundle) are already generating incremental high-margin revenue, and the transition appears to be trending to the high end of DaVita’s prior profit expectations, supporting higher operating income and EPS guidance.

- Improved operational efficiency, cost control, and digitalization efforts (including rapid recovery from the recent cyberattack and reductions in G&A expenses) indicate an ability to manage costs and safeguard margins even in the face of external disruptions.

- Strategic international acquisitions (such as the Latin America expansion) and a disciplined capital allocation strategy—with accelerated share buybacks—are likely to provide an incremental lift to future earnings per share and support long-term value creation for shareholders.

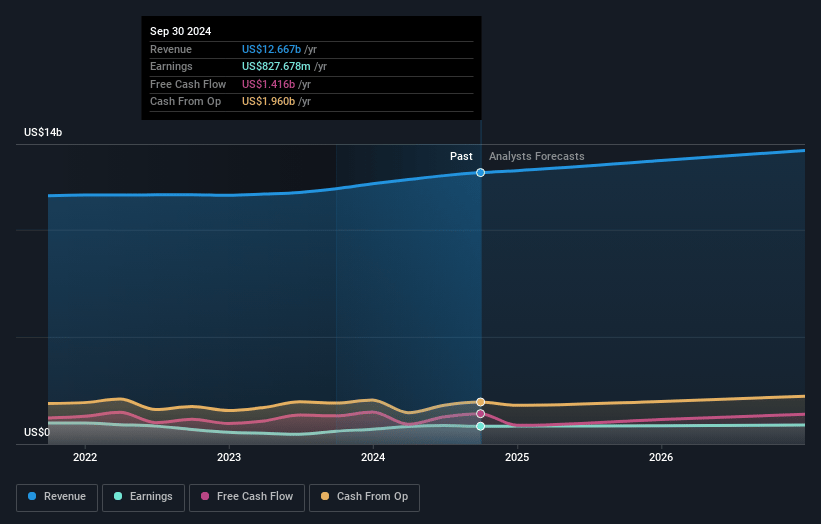

DaVita Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming DaVita's revenue will grow by 4.4% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 6.6% today to 5.7% in 3 years time.

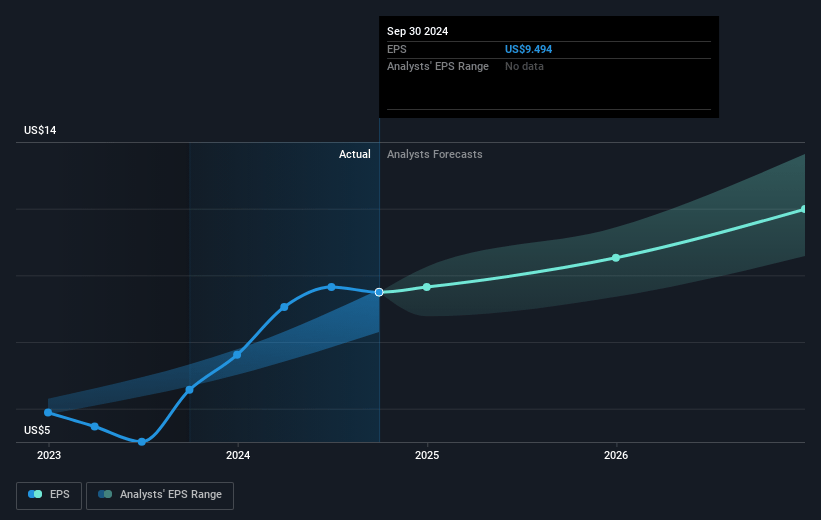

- Analysts expect earnings to reach $847.6 million (and earnings per share of $12.12) by about May 2028, down from $859.6 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 14.3x on those 2028 earnings, up from 12.3x today. This future PE is lower than the current PE for the US Healthcare industry at 21.0x.

- Analysts expect the number of shares outstanding to decline by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.14%, as per the Simply Wall St company report.

DaVita Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The recent cybersecurity incident not only disrupted operations but is expected to result in both one-time and ongoing regulatory and legal expenses, as well as potential reputational risk, which could weigh on net margins and increase compliance costs over the long term.

- Lower-than-expected treatment volumes due to elevated patient mortality (specifically related to a severe flu season) and ongoing periodic supply chain disturbances (e.g., PD supply shortages) highlight the company’s sensitivity to external shocks and may result in slower volume growth and persistent volatility in revenue.

- Dependence on Medicare reimbursement and changes in policy, such as the risk of expiration of enhanced premium tax credits, could expose DaVita to cumulative operating income declines ($75–$120 million over three years), impacting predictability and stability of future earnings.

- The integrated kidney care (IKC) segment continues to operate at a loss and faces heightened competition from new entrants who are taking aggressive pricing stances, potentially requiring DaVita to increase investment or cut prices; this could limit near

- to medium-term profit improvement for this strategic growth area.

- Ongoing international expansion, including recent acquisitions, introduces additional risks related to regulatory restrictions, integration challenges (such as mandated divestitures and compliance in markets like Brazil), and potential foreign currency or operational hurdles, increasing the risk to both margin and earnings stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $163.889 for DaVita based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $186.0, and the most bearish reporting a price target of just $145.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $14.7 billion, earnings will come to $847.6 million, and it would be trading on a PE ratio of 14.3x, assuming you use a discount rate of 7.1%.

- Given the current share price of $139.9, the analyst price target of $163.89 is 14.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.