Key Takeaways

- The expansion of Amwell's platform in the Military Health System is expected to boost subscription revenue and enhance margins significantly.

- Divesting Amwell Psychiatric Care strengthens the balance sheet, allowing focus on higher-margin core services and improved net margins.

- Flat revenue growth, declining visit volumes, and client attrition highlight challenges in sustaining revenue; reliance on military contracts and cost cuts may risk future growth.

Catalysts

About American Well- An enterprise platform and software company, delivers digitally enabling hybrid care in the United States and internationally.

- The staged launch and expansion of Amwell's platform across the Military Health System, their most significant growth initiative, is expected to significantly increase subscription revenue, with the full deployment anticipated to be completed this year. This will likely lead to increased revenues and margins as well as a higher quality revenue mix due to the size and strategic importance of such contracts.

- Amwell aims to achieve positive cash flow by 2026 through increasing subscription software revenues and aligning costs, expecting a meaningful margin expansion with an over 60% improvement in adjusted EBITDA in the coming year, impacting their net margins and earnings positively.

- The divestiture of Amwell Psychiatric Care, which was not integral to the company's core offering, has bolstered Amwell's balance sheet by adding $30 million in cash and allowed them to focus on higher margin core subscription services, likely leading to improved net margins and operating income.

- Amwell is focused on expanding its existing contracts and signing new ones, notably in the government sector, with significant opportunities in the pipeline. Successful execution could considerably enhance their revenue growth and subscription revenue mix.

- Increasing the mix of recurring subscription revenue, partly through strategic partnerships like the one with Vida Health, is expected to not only drive revenue growth but also improve earnings visibility, predictability, and profitability by enhancing the quality of revenue and expanding profit margins.

American Well Future Earnings and Revenue Growth

Assumptions

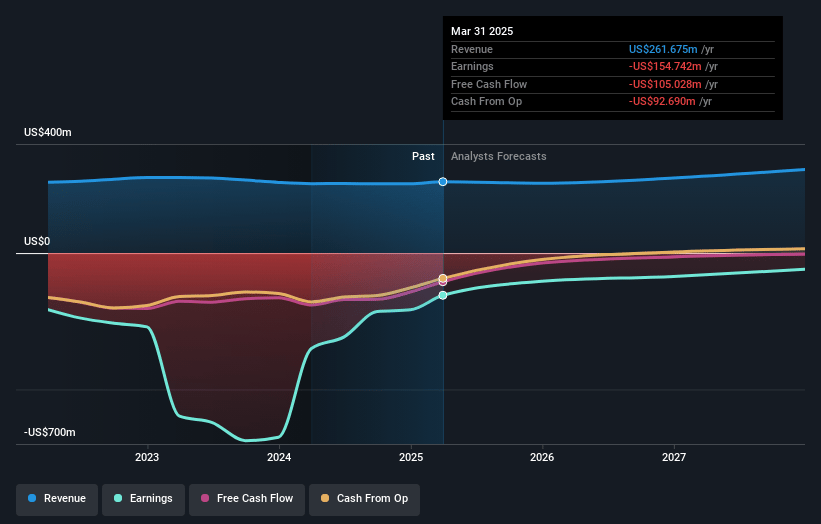

How have these above catalysts been quantified?- Analysts are assuming American Well's revenue will grow by 6.0% annually over the next 3 years.

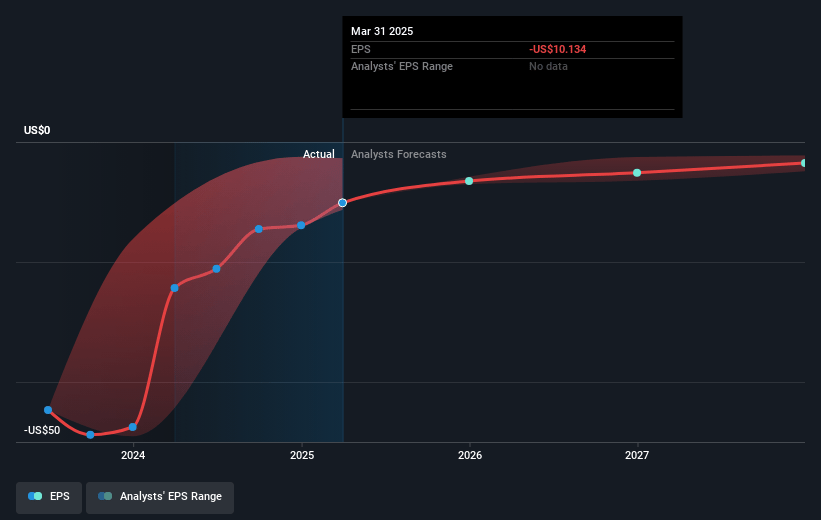

- Analysts are not forecasting that American Well will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate American Well's profit margin will increase from -81.8% to the average US Healthcare Services industry of 14.7% in 3 years.

- If American Well's profit margin were to converge on the industry average, you could expect earnings to reach $44.6 million (and earnings per share of $2.48) by about May 2028, up from $-208.1 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 5.5x on those 2028 earnings, up from -0.5x today. This future PE is lower than the current PE for the US Healthcare Services industry at 53.8x.

- Analysts expect the number of shares outstanding to grow by 5.31% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.62%, as per the Simply Wall St company report.

American Well Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Amwell's revenue growth has been stagnant, with Q4 2024 revenue flat compared to the previous year, indicating challenges in driving top-line growth which could impact future earnings.

- A significant decline of 18% in visit volumes compared to the previous year suggests potential challenges in maintaining customer engagement and sustaining revenue streams from visit-based services.

- The company experienced material attrition among its major clients in 2024, affecting the stability of its revenue base and posing a risk to future revenue continuity.

- The dependency on a successful renewal and execution of the Military Health System contract exposes the company to significant risk if there are delays or changes to government funding, which could impact projected revenues.

- Cost reduction initiatives, while improving EBITDA, could lead to underinvestment in areas critical for growth and innovation, potentially impacting long-term revenue growth prospects and margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $11.0 for American Well based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $15.0, and the most bearish reporting a price target of just $7.5.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $303.2 million, earnings will come to $44.6 million, and it would be trading on a PE ratio of 5.5x, assuming you use a discount rate of 7.6%.

- Given the current share price of $7.3, the analyst price target of $11.0 is 33.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.