Key Takeaways

- Investments in technology solutions and integrated platforms aim to drive revenue growth, improve efficiency, and attract new clients in the healthcare sector.

- Stabilizing and increasing bill rates are expected to enhance gross margins and profitability amid demand recovery in staffing segments.

- Wage inflation and declining international nurse assignments pose challenges, leading to increased costs, narrower margins, and potential revenue impacts from key client changes and labor disruption reliance.

Catalysts

About AMN Healthcare Services- Provides healthcare workforce solutions and staffing services to acute and sub-acute care hospitals and other healthcare facilities in the United States.

- AMN Healthcare's investments in technology solutions such as ShiftWise Flex and the Passport app are expected to drive future revenue growth by improving client engagement and operational efficiency through enhanced visibility, cost control, and staffing management capabilities.

- The rollout of integrated platforms like WorkWise is anticipated to attract new clients and boost revenue by offering comprehensive workforce management solutions, which can cater to long-term objectives for cost-effective flexibility in the healthcare sector.

- Stabilizing bill rates for Nurse and Allied staffing and increasing bill rates in locum tenens are likely to positively impact AMN's gross margins and overall profitability as demand recovery progresses in these segments.

- Increasing utilization of innovative technology offerings like Televate for virtual support in the schools business may generate additional revenue streams and strengthen AMN’s competitive positioning in specialized markets.

- As healthcare organizations recognize Travel Nurses as viable alternatives to costly overtime and permanent hiring, any demand recovery in travel nurse staffing, which constituted 30% of AMN's 2024 revenue, could significantly enhance AMN’s revenue and earnings.

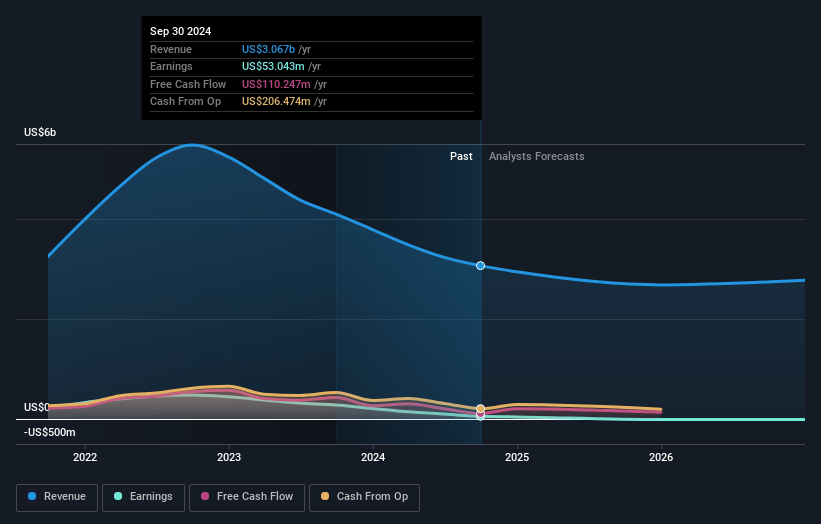

AMN Healthcare Services Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming AMN Healthcare Services's revenue will decrease by 1.2% annually over the next 3 years.

- Analysts are not forecasting that AMN Healthcare Services will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate AMN Healthcare Services's profit margin will increase from -4.9% to the average US Healthcare industry of 4.6% in 3 years.

- If AMN Healthcare Services's profit margin were to converge on the industry average, you could expect earnings to reach $133.5 million (and earnings per share of $3.51) by about April 2028, up from $-147.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 10.2x on those 2028 earnings, up from -4.7x today. This future PE is lower than the current PE for the US Healthcare industry at 23.2x.

- Analysts expect the number of shares outstanding to grow by 0.5% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.81%, as per the Simply Wall St company report.

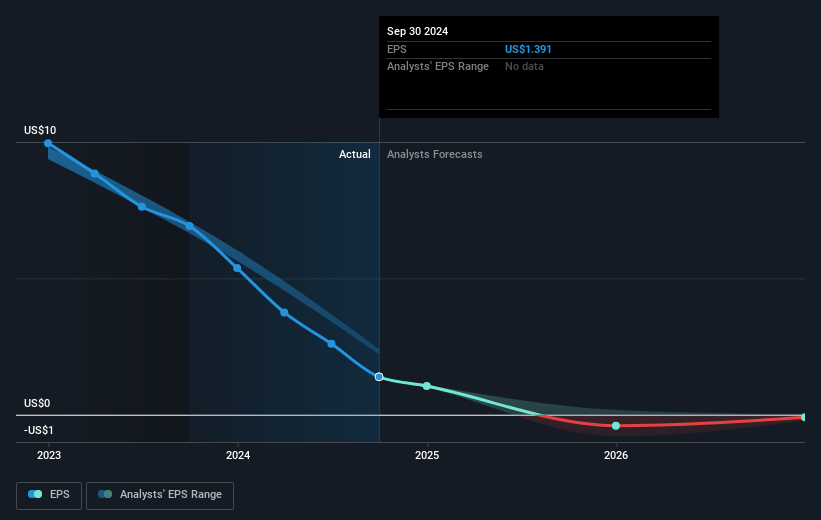

AMN Healthcare Services Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company faces challenges with staffing gross margins, which declined through 2024, leading to narrower net margins. This was exacerbated by increased unfilled orders and vendor-neutral programs due to candidates rejecting low pay rates.

- Wage inflation remains high in healthcare, especially for qualified professionals, which could lead to increased costs and thus lower net margins.

- International nurse assignments are expected to decline due to visa retrogression, potentially affecting revenue from this segment and impacting overall earnings.

- A potential decline in large client utilization could result in reduced revenue for AMN Healthcare, as these clients are an essential part of the current revenue base.

- Continued reliance on labor disruption revenue indicates potential vulnerability if these events do not occur or decrease in frequency, impacting both revenue stability and predictability of future earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $28.571 for AMN Healthcare Services based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $33.0, and the most bearish reporting a price target of just $25.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $2.9 billion, earnings will come to $133.5 million, and it would be trading on a PE ratio of 10.2x, assuming you use a discount rate of 7.8%.

- Given the current share price of $18.22, the analyst price target of $28.57 is 36.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.