Key Takeaways

- Transitioning its digital supply chain strategy boosts potential earnings and revenue growth through enhanced supply chain resilience and innovation.

- Focus on AI-driven process improvements and disciplined capital deployment is set to enhance net margins and shareholder value.

- Declines in consulting demand, goodwill impairment, and tariff uncertainty are impacting revenue, profitability, and future earnings, with recontracting adding margin pressure.

Catalysts

About Premier- Operates as a healthcare improvement company in the United States.

- Premier's successful transition of its digital supply chain strategy beyond the pilot phase, marked by signing agreements with major partners, indicates future revenue growth opportunities through innovation in supply chain resiliency, enhancing earnings potential.

- Premier's emphasis on AI-enabling manual back-office processes and enhancing supply chain data for total non-labor health care spend could lead to cost savings and improved net margins due to increased efficiency.

- The appointment of David Zito as President of Performance Services, with his expertise in financial turnaround and revenue diversification strategies, is anticipated to invigorate revenue growth and potentially improve net margins within the segment.

- Premier's ongoing efforts to address drug shortages through its provider-focused data and market intelligence may enhance revenue by offering unique solutions that strengthen relationships with health care providers.

- Planned share buybacks and disciplined capital deployment, including a $1 billion authorization and dividend distributions, are expected to support increased earnings per share (EPS) and overall shareholder value.

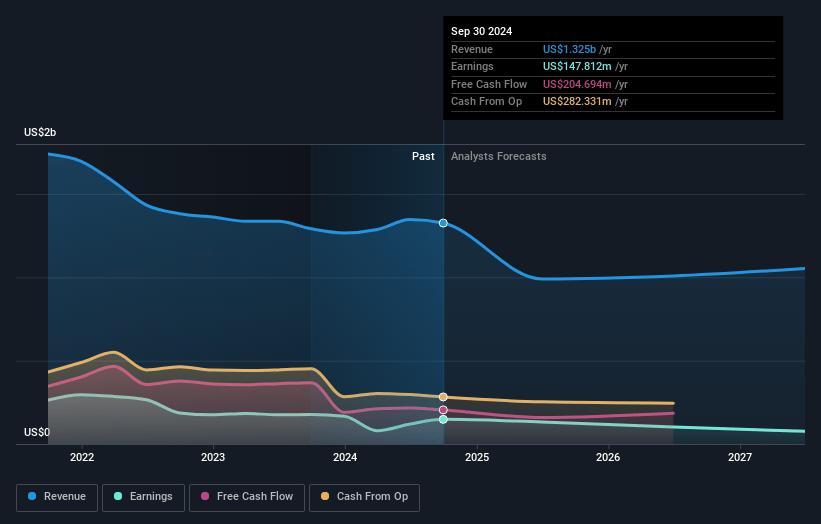

Premier Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Premier's revenue will decrease by 7.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.1% today to 9.9% in 3 years time.

- Analysts expect earnings to reach $100.1 million (and earnings per share of $1.14) by about April 2028, up from $39.3 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $141.4 million in earnings, and the most bearish expecting $80.5 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 17.3x on those 2028 earnings, down from 47.4x today. This future PE is lower than the current PE for the US Healthcare industry at 23.6x.

- Analysts expect the number of shares outstanding to decline by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.21%, as per the Simply Wall St company report.

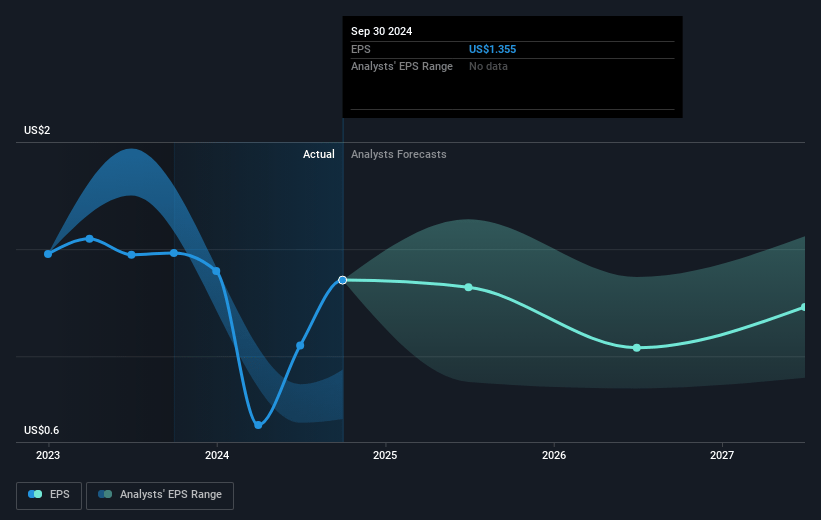

Premier Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's second quarter revenue and adjusted EBITDA were below expectations, primarily due to a decline in net administrative fees revenue in Supply Chain Services and lower demand in consulting services, which could negatively impact future revenue and net margins.

- There was a $127 million impairment charge related to goodwill in the Performance Services segment, indicating challenges in data and technology, which could affect future earnings and profitability.

- Revenue in the Performance Services segment declined by 19% due to lower consulting services demand and an unfavorable product mix in applied sciences, potentially impacting revenue projections.

- The company is in the process of recontracting its GPO members, which involves increasing the blended fee share to the low 60% range and potentially to the high 60s, impacting net administrative fees and overall net margins.

- There is uncertainty regarding tariffs and their potential impact on the supply chain, with possible implications for contract pricing and cost variability, which could affect the company's future revenues and net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $19.786 for Premier based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $22.5, and the most bearish reporting a price target of just $19.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.0 billion, earnings will come to $100.1 million, and it would be trading on a PE ratio of 17.3x, assuming you use a discount rate of 6.2%.

- Given the current share price of $20.39, the analyst price target of $19.79 is 3.1% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.