Narratives are currently in beta

Key Takeaways

- Transition to electric frac fleets and long-term contracts enhance operational efficiency, revenue stability, and future margins.

- Share repurchases and strategic acquisitions aim to improve earnings, revenue growth, and shareholder value.

- Focus on electrification and next-gen equipment risks financial strain if returns fall short, amid market softness and operational unpredictability.

Catalysts

About ProPetro Holding- Operates as an integrated oilfield services company.

- The transition to next-generation FORCE electric frac fleets is expected to enhance operational efficiencies and reduce fuel costs, positively impacting future revenue and net margins.

- Long-term contracts, such as the three-year agreement with ExxonMobil for hydraulic fracturing services using the FORCE electric fleets, help derisk future earnings and provide revenue stability.

- The strategic fleet transition away from conventional Tier II diesel-only equipment to dual-fuel and electric options is anticipated to drive higher utilization and margins, given the shift in customer preferences.

- ProPetro's ongoing share repurchase program, approved for $100 million additional buybacks, is aimed at improving earnings per share by reducing the share count and returning capital to shareholders.

- Continued focus on value-enriching mergers and acquisitions, like Silvertip in the wireline market and AquaProp in sand solutions, are expected to contribute positively to both top-line revenue growth and net margins.

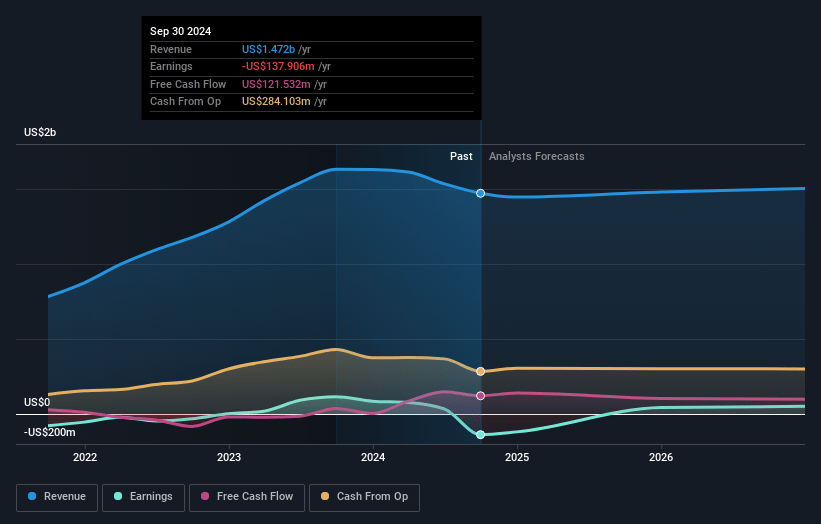

ProPetro Holding Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming ProPetro Holding's revenue will grow by 1.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from -9.4% today to 6.9% in 3 years time.

- Analysts expect earnings to reach $104.2 million (and earnings per share of $1.07) by about November 2027, up from $-137.9 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.2x on those 2027 earnings, up from -5.8x today. This future PE is lower than the current PE for the US Energy Services industry at 16.6x.

- Analysts expect the number of shares outstanding to decline by 1.75% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.29%, as per the Simply Wall St company report.

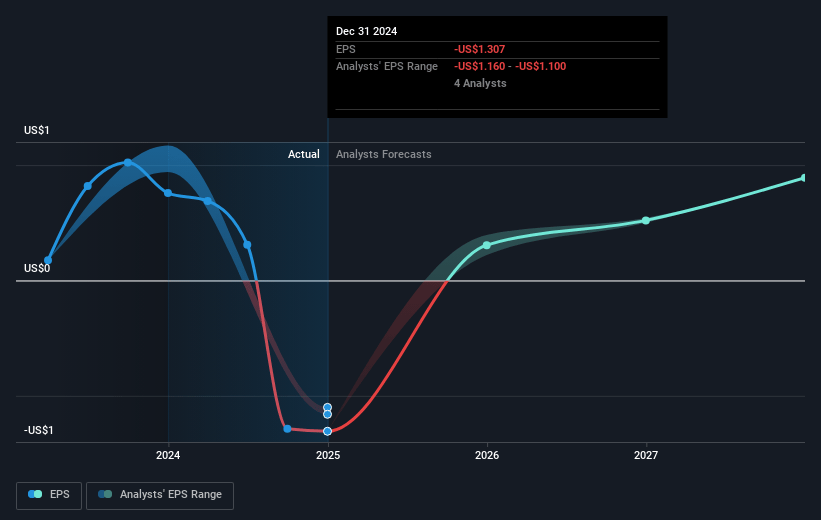

ProPetro Holding Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's focus on electrification and next-generation equipment carries significant capital expenditure, which could strain financial resources and impact future earnings if the expected transition does not yield anticipated returns.

- Persistent market softness, particularly in Tier II diesel-only equipment and wireline offerings, poses a challenge for sustaining revenue growth, as these segments continue to experience pricing pressure.

- Dependency on weather conditions and seasonal holiday impacts can lead to unpredictable fluctuations in fleet utilization and operational downtime, potentially affecting quarterly revenue and EBITDA consistency.

- The company faces macroeconomic and industry-specific headwinds that could hinder demand for its oilfield services and result in reduced market activity, directly impacting revenue and net margins.

- Execution of the dynamic capital allocation strategy, including M&A activities and maintenance of shareholder returns, entails execution risks and could stretch the company's capacity to manage costs effectively, affecting net margins and cash flow.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $10.31 for ProPetro Holding based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $12.0, and the most bearish reporting a price target of just $8.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $1.5 billion, earnings will come to $104.2 million, and it would be trading on a PE ratio of 12.2x, assuming you use a discount rate of 8.3%.

- Given the current share price of $7.77, the analyst's price target of $10.31 is 24.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives