Key Takeaways

- Terminal expansion and fleet growth position Navigator Holdings to capitalize on increased ethylene demand, boosting future revenue and earnings.

- Strategic refinancing and a diversified cargo mix improve financial flexibility and net margins, fostering robust earnings growth.

- Geopolitical tensions, refinancing needs, and market competition may pressure revenue and margins, while U.S. production and export dynamics pose operational risks.

Catalysts

About Navigator Holdings- Engages in owning and operating a fleet of liquefied gas carriers worldwide.

- The expansion of Navigator Holdings' Morgan's Point terminal, which was completed on time and on budget, increases ethylene export capacity from 125 tons per hour to 375 tons per hour. This should lead to increased future revenue as the company contracts out more capacity and benefits from higher throughput volumes.

- The acquisition of three secondhand handysize ethylene carriers and the order of two new midsize ethylene carriers are expected to increase Navigator Holdings' fleet capacity. This will support future earnings growth by enabling the company to capitalize on rising export demand and maintain high vessel utilization rates.

- Navigator Holdings expects a positive impact on revenue from increased U.S. natural gas liquids production and the expansion of U.S. export terminal capacity, leading to greater transport demand for ethane and ethylene over the next four years.

- Strategic refinancing efforts, including extending debt maturities and reducing interest expenses, are anticipated to improve Navigator Holdings' net margins and overall financial flexibility, supporting future earnings growth.

- The company plans to maintain high time charter equivalent (TCE) rates and vessel utilization, which supports stable revenue streams. Additionally, the broadened cargo mix with increased petrochemical transport could enhance net margins due to higher earnings potential from diversified cargo offerings.

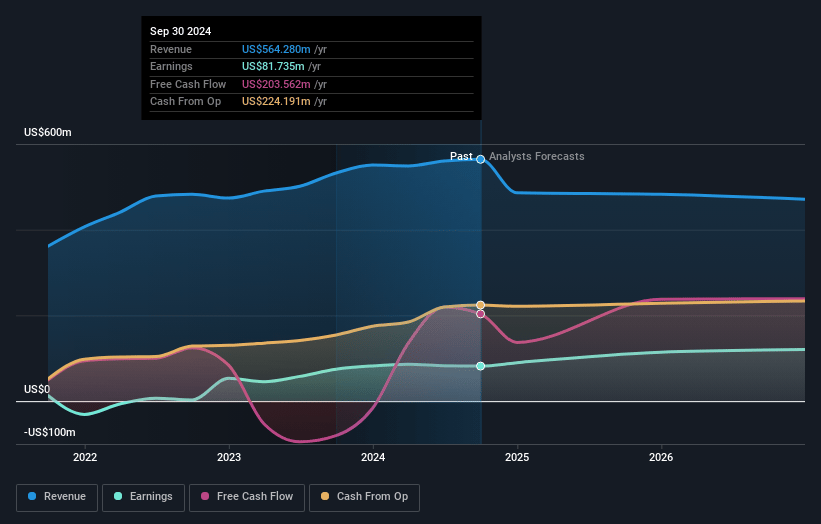

Navigator Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Navigator Holdings's revenue will decrease by 5.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 15.1% today to 29.0% in 3 years time.

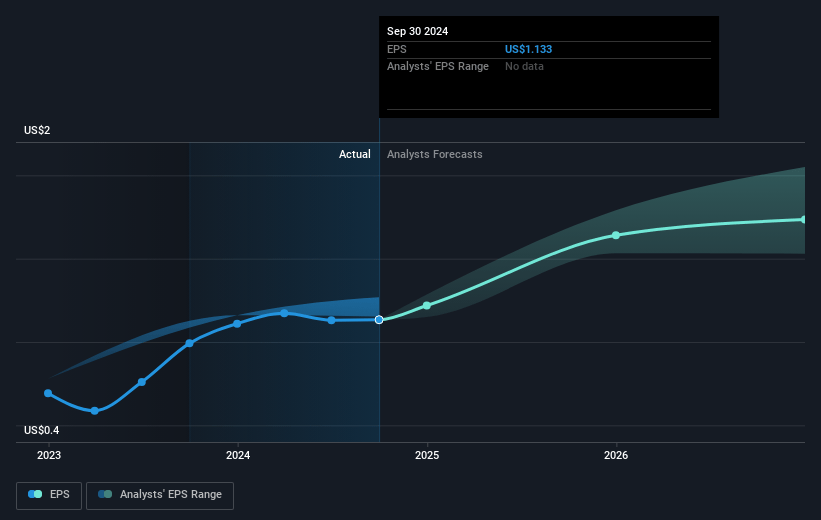

- Analysts expect earnings to reach $138.0 million (and earnings per share of $1.98) by about April 2028, up from $85.6 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.2x on those 2028 earnings, up from 9.8x today. This future PE is greater than the current PE for the US Oil and Gas industry at 11.4x.

- Analysts expect the number of shares outstanding to decline by 5.39% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.4%, as per the Simply Wall St company report.

Navigator Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- U.S. cracker turnarounds have led to reduced domestic supply and higher domestic prices, which narrow the ethylene arbitrage and could limit volume growth and revenue potential for the ethylene export terminal.

- The issuance of $100 million in new unsecured bonds at 7.25% and the need for refinancing existing debt could increase interest expenses, affecting net margins and overall earnings if interest rates rise further.

- Geopolitical tensions, such as conflicts in the Red Sea or trade frictions affecting tariffs on ethylene, could negatively impact Navigator Holdings' ability to transport petrochemicals and thus affect its revenue.

- The handysize order book, while currently attractive, may see increased competition if new orders are placed in anticipation of a stronger market, potentially pressuring future charter rates and revenue.

- The dependence on continued growth in U.S. NGL production and export terminal capacity expansions poses a risk; any slowdown or delays in these areas could impact Navigator's revenue from transport demands.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $22.167 for Navigator Holdings based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $475.6 million, earnings will come to $138.0 million, and it would be trading on a PE ratio of 12.2x, assuming you use a discount rate of 9.4%.

- Given the current share price of $12.08, the analyst price target of $22.17 is 45.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.