Key Takeaways

- Strategic acquisitions and efficiency measures drive significant production growth and cost savings, boosting revenue, net margins, and overall earnings.

- Focus on disciplined capital deployment and increased dividends enhances shareholder value, supporting steady financial growth and investor confidence.

- Strategic integration and market reliance issues could affect short-term growth, financial stability, and profitability, risking investor confidence and potential liquidity opportunities.

Catalysts

About Matador Resources- An independent energy company, engages in the acquisition, exploration, development, and production of oil and natural gas resources in the United States.

- The acquisition of Ameredev properties, which contain high-quality rock, is expected to drive significant production growth for Matador Resources. The company anticipates approximately 30% production growth in the first quarter of 2025 compared to the same period in the previous year. This is likely to boost revenue significantly.

- The adoption of efficiency measures, such as batch drilling and sim

- and trimul-frac technologies, has led to substantial cost savings. These efficiency gains are expected to continue reducing drilling and completion costs, positively impacting net margins and overall earnings.

- The reduction of operating expenses on newly acquired properties by approximately $2 million per month and the reuse of produced water for fracturing operations demonstrate improved cost management, which should enhance future net margins and cash flow.

- Matador Resources' focus on profitable growth at a measured pace and disciplined capital deployment, including the consideration of expanding its midstream business, is expected to contribute to steady financial growth and increased free cash flow.

- The company's strategic decision to withhold immediate stock buybacks and instead focus on a consistent increase in dividends reflects a commitment to returning value to long-term shareholders, which could lead to higher stock valuation through enhanced investor confidence in stable future earnings growth.

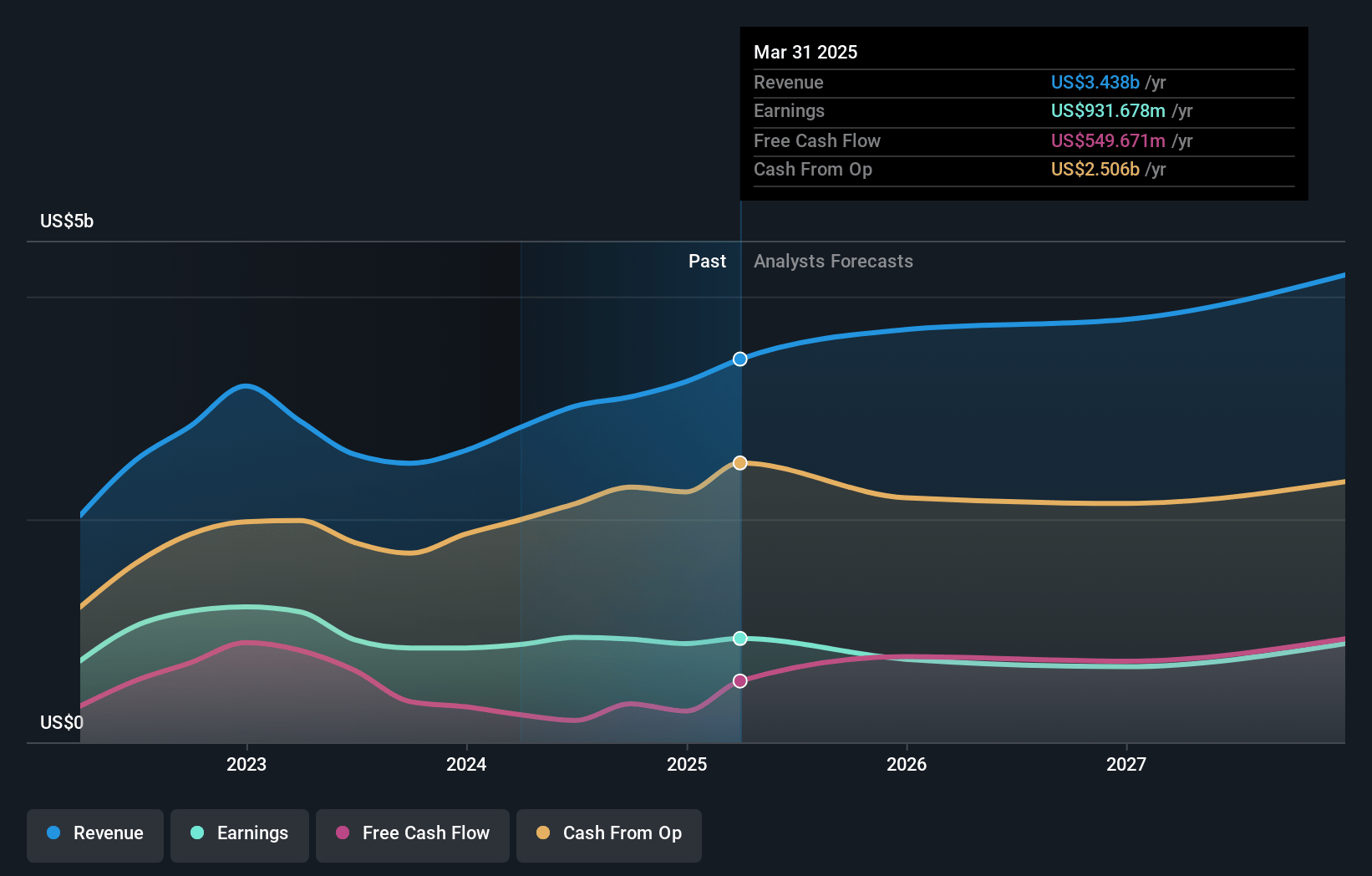

Matador Resources Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Matador Resources's revenue will grow by 16.2% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 27.4% today to 18.3% in 3 years time.

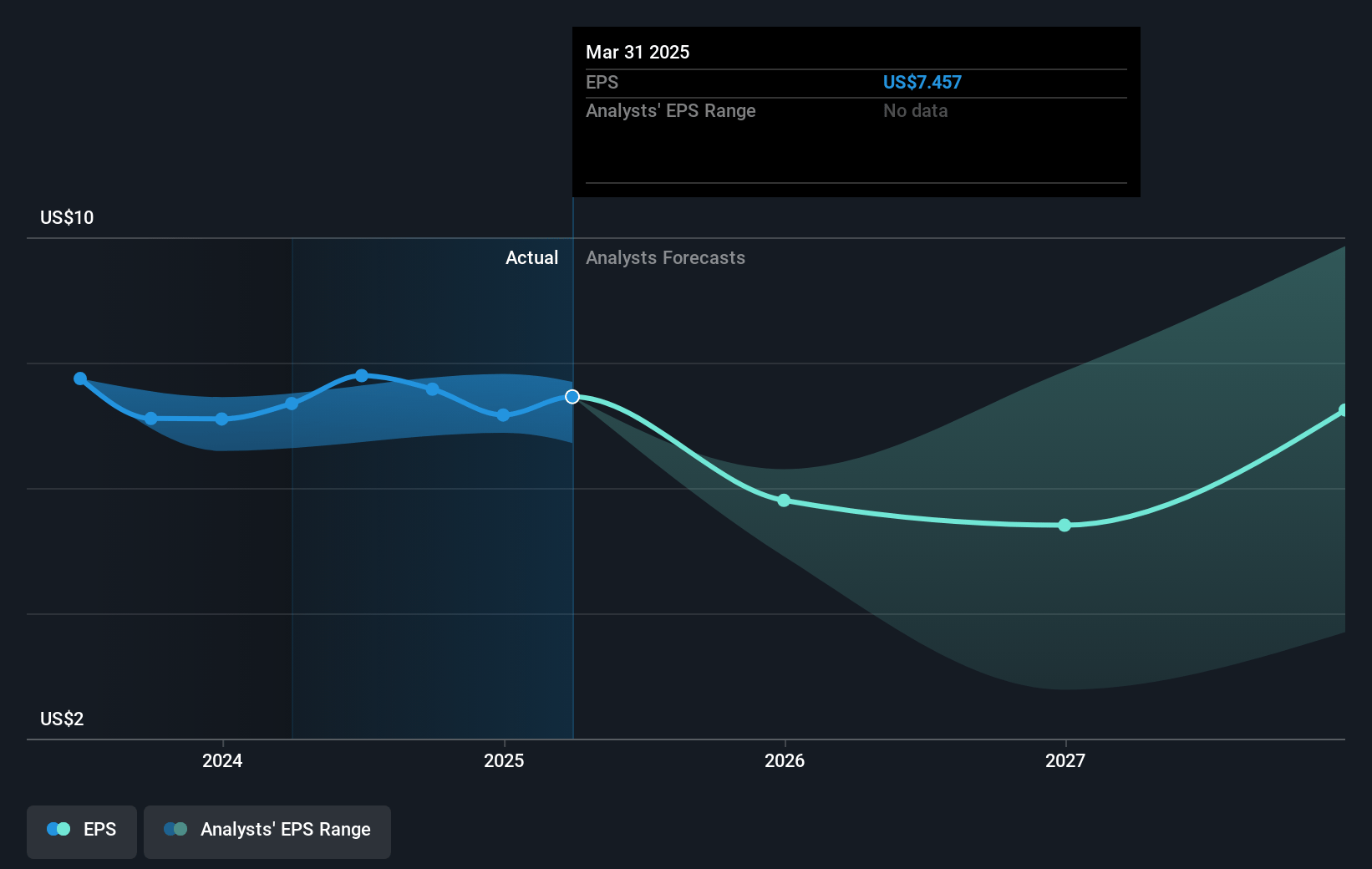

- Analysts expect earnings to reach $927.0 million (and earnings per share of $7.39) by about March 2028, up from $885.3 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.9x on those 2028 earnings, up from 7.2x today. This future PE is greater than the current PE for the US Oil and Gas industry at 12.7x.

- Analysts expect the number of shares outstanding to grow by 0.34% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.4%, as per the Simply Wall St company report.

Matador Resources Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The integration of the Ameredev properties introduces a timing issue, impacting the sequential production growth comparisons. This could lead to investor concerns about consistency in production and potentially affect short-term revenue projections.

- There is an ongoing reliance on volatile commodity prices, specifically oil and gas, which are unpredictable and can significantly impact net margins and overall financial stability.

- The focus on year-over-year growth, while possibly obscuring sequential growth concerns, could mask short-term fluctuations and deter analysts concentrating on quarterly earnings, potentially affecting stock price volatility and short-term earnings expectations.

- With a substantial investment in the Ameredev deal, any missteps in realizing the anticipated operational efficiencies or unexpected integration costs could strain profitability and net margins.

- The company’s strategy to retain assets like Cotton Valley, instead of divesting amid favorable market conditions, could lead to missed opportunities for immediate liquidity, impacting free cash flow and potential debt reduction capabilities.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $74.294 for Matador Resources based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $90.0, and the most bearish reporting a price target of just $62.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $5.1 billion, earnings will come to $927.0 million, and it would be trading on a PE ratio of 12.9x, assuming you use a discount rate of 8.4%.

- Given the current share price of $50.56, the analyst price target of $74.29 is 31.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.