Key Takeaways

- Prioritizing debt repayment over reinvestment or shareholder returns indicates a conservative strategy, possibly reducing appeal to growth-focused investors.

- Natural gas market challenges and limited production growth could pressure EQT's future revenue and profitability.

- EQT's focus on operational efficiency, strategic production tactics, and proactive financial management could enhance profitability, maintain investor confidence, and promote revenue growth.

Catalysts

About EQT- Engages in the production, gathering, and transmission of natural gas.

- The reduction to two frac crews in 2025, despite efficiency gains, suggests a prioritization of cost savings over production growth, which might lead to reduced revenue growth as EQT maintains current production levels instead of expanding.

- Increasing concerns about natural gas supply and demand imbalances, coupled with potential headwinds from new Permian pipelines and additional global LNG capacity post-2026, could negatively affect future gas prices and consequently pressure EQT's revenue and profitability.

- EQT's decision not to grow production into high prices without clear demand signals raises questions about foregone revenue opportunities, potentially impacting future earnings as the market lacks new significant supply sources.

- The reliance on efficiency gains and compression projects for operational improvements creates uncertainty in future capital expenditures and production outcomes, which could hinder expected cost reductions and affect profit margins if these projects face delays or underdeliver.

- The stated intention to primarily use free cash flow for debt repayment rather than reinvesting in growth or increasing shareholder returns reflects a conservative capital strategy, potentially limiting immediate earnings per share growth and reducing attractiveness to growth-focused investors.

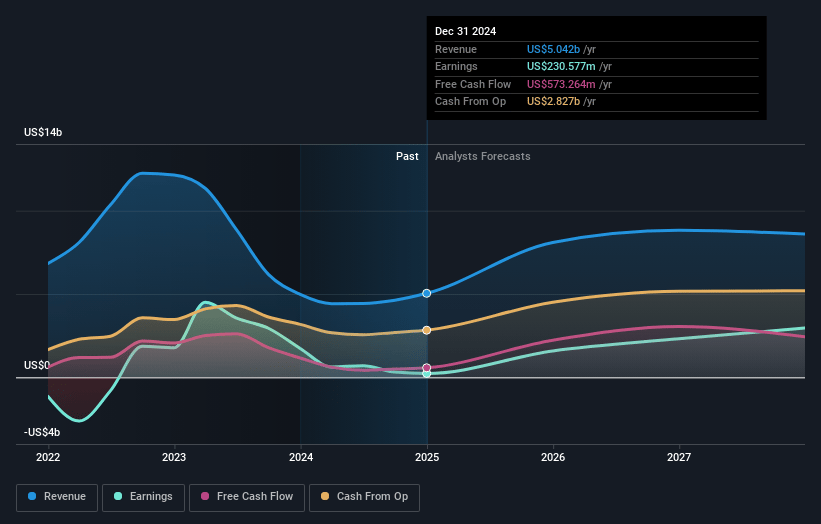

EQT Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on EQT compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming EQT's revenue will grow by 16.8% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 4.6% today to 10.1% in 3 years time.

- The bearish analysts expect earnings to reach $813.7 million (and earnings per share of $1.34) by about April 2028, up from $230.6 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 52.0x on those 2028 earnings, down from 132.1x today. This future PE is greater than the current PE for the US Oil and Gas industry at 11.4x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.06%, as per the Simply Wall St company report.

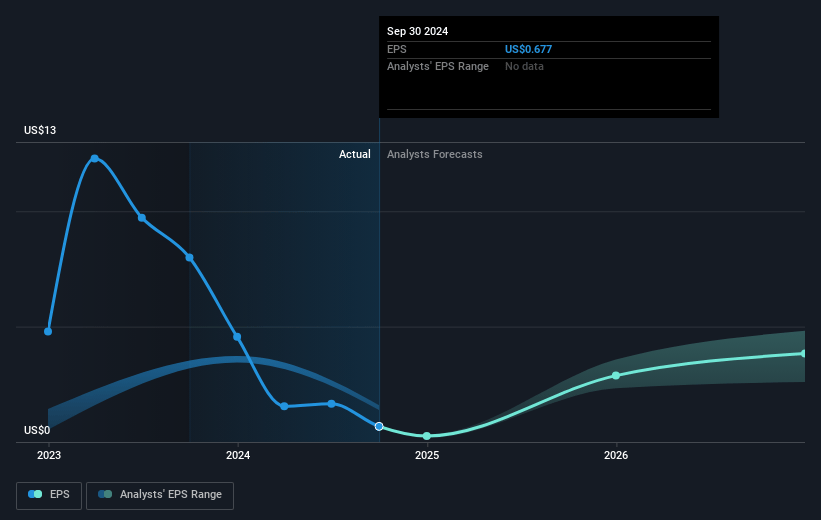

EQT Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- EQT's rapid integration of Equitrans and the realization of more than $200 million of annualized base synergies could lead to improved cost efficiency, positively impacting net margins and earnings.

- The transformational gains in operational efficiency, including a 20% increase in completed lateral footage per day and lower well costs, suggest EQT could maintain high production levels without increased capital expenditure, potentially enhancing profit margins.

- The company's strategy of tactical curtailment and exposing production to high local pricing during strong demand periods resulted in substantial revenue uplift, indicating that EQT may sustain or grow its earnings despite market volatility.

- EQT's ability to generate significant free cash flow, even with relatively low gas prices, highlights its strong earnings power and may maintain investor confidence in the company's financial stability.

- With a proactive approach to balance sheet management and anticipation of substantial free cash flow, EQT is positioned to reduce its debt quickly, improving its financial flexibility and potentially benefiting overall profitability and revenue growth opportunities.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for EQT is $47.16, which represents one standard deviation below the consensus price target of $55.64. This valuation is based on what can be assumed as the expectations of EQT's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $73.0, and the most bearish reporting a price target of just $35.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $8.0 billion, earnings will come to $813.7 million, and it would be trading on a PE ratio of 52.0x, assuming you use a discount rate of 7.1%.

- Given the current share price of $50.98, the bearish analyst price target of $47.16 is 8.1% lower. The relatively low difference between the current share price and the analyst bearish price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystLowTarget holds no position in NYSE:EQT. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.