Narratives are currently in beta

Key Takeaways

- Successful milestones and low carbon technologies may boost production, improve operational efficiencies, and enhance revenue and net margins.

- Asset sales and synergies from acquisitions could increase liquidity, support share repurchases, and positively impact future earnings and EPS.

- Challenges such as acquisition delays, execution risks, and legislative controls heighten uncertainty, threatening Chevron's profitability and impacting cash flow and margins.

Catalysts

About Chevron- Through its subsidiaries, engages in the integrated energy and chemicals operations in the United States and internationally.

- Chevron's successful project milestones, such as increased production in the Permian and Gulf of Mexico, are expected to boost production to 300,000 barrels per day by 2026, potentially driving revenue growth.

- The expansion of Chevron’s CO2 storage portfolio and the implementation of low carbon intensity technologies in Colorado could enhance operational efficiencies and reduce costs, potentially improving net margins.

- Synergies from the PDC Energy acquisition have already exceeded expectations, generating over $1 billion in free cash flow, which could positively impact future earnings.

- Asset sales in Canada, Alaska, and Congo are expected to generate $8 billion before taxes, potentially increasing liquidity and funding share repurchases, thereby enhancing earnings per share (EPS).

- Structural cost reductions projected at $2 billion to $3 billion by 2026, through portfolio optimization and technological innovations, might lower operating expenses and further support net profit margins.

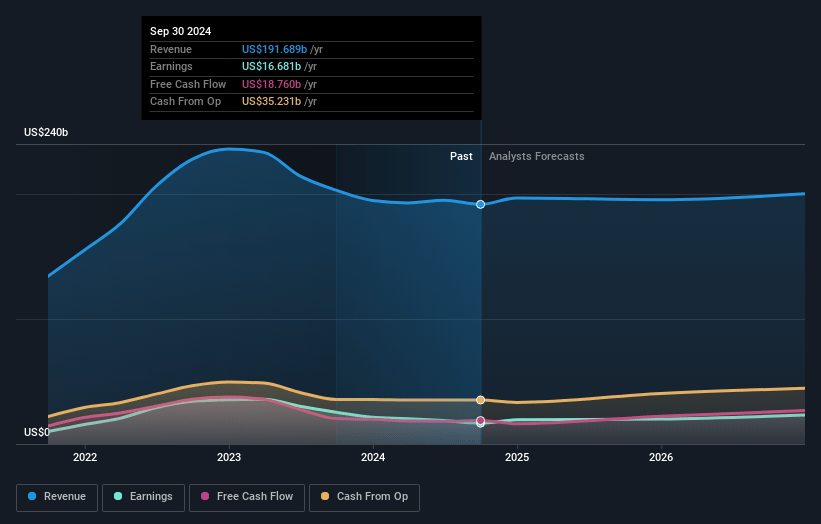

Chevron Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Chevron's revenue will decrease by -3.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 8.7% today to 13.0% in 3 years time.

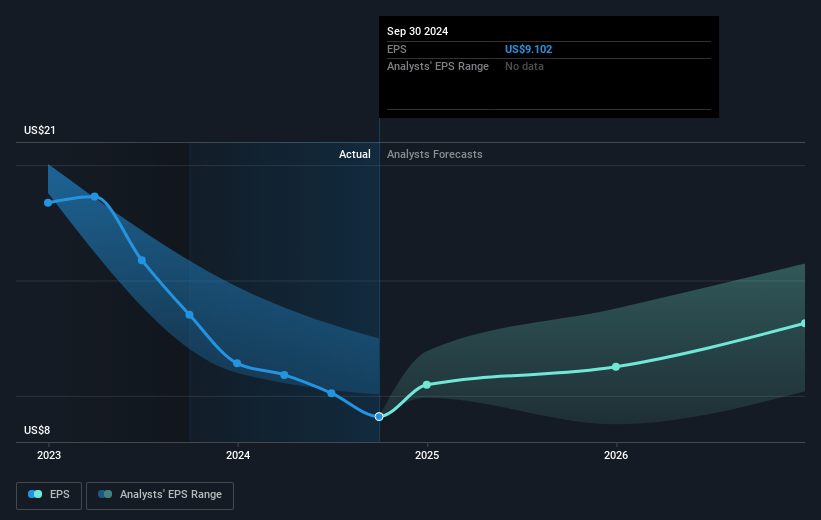

- Analysts expect earnings to reach $22.2 billion (and earnings per share of $13.16) by about November 2027, up from $16.7 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $30.5 billion in earnings, and the most bearish expecting $16.6 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 15.9x on those 2027 earnings, down from 17.1x today. This future PE is greater than the current PE for the US Oil and Gas industry at 11.0x.

- Analysts expect the number of shares outstanding to decline by 2.1% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.14%, as per the Simply Wall St company report.

Chevron Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The ongoing arbitration related to the Hess acquisition introduces uncertainty and could delay potential value realization, impacting revenue and net margins due to integration costs and potential synergies being postponed.

- Significant complex commissioning work remains at TCO, which represents execution risk. Any slippage in schedules can impact cash flow and net margins due to delay in startup procedures.

- Increased maintenance and shutdown schedules, including planned maintenance in U.S. downstream operations and international upstream operations, could lower production levels and impact short-term revenues.

- Lower refining margins and high depreciation, depletion, and amortization (DD&A) at TCO have already affected adjusted earnings, indicating a vulnerability in refining profitability and a potential drag on net margins.

- Potentially higher costs related to state-imposed legislative controls in California, such as the new bureaucratic measures in the refining sector, could affect profitability and operational margins due to increased regulatory compliance costs.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $170.44 for Chevron based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $194.0, and the most bearish reporting a price target of just $145.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $171.1 billion, earnings will come to $22.2 billion, and it would be trading on a PE ratio of 15.9x, assuming you use a discount rate of 7.1%.

- Given the current share price of $158.72, the analyst's price target of $170.44 is 6.9% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives