Key Takeaways

- Expanding production, technological advances, and a diversified commodity mix position the company for stable cash flow, durable growth, and reduced earnings volatility.

- Efficient capital allocation, inventory depth, and a focus on shareholder returns support long-term financial sustainability and create value for investors.

- Persistently low gas prices, operational risks, regulatory pressures, and inventory decline threaten Coterra's margins and growth, despite efforts to expand production and diversify sales.

Catalysts

About Coterra Energy- An independent oil and gas company, engages in the exploration, development, and production of oil, natural gas, and natural gas liquids in the United States.

- Coterra's strategic focus on consistently expanding both oil and gas production across the Permian, Marcellus, and Anadarko enables the company to capture rising global energy demand-especially with supportive trends like LNG export growth and US power generation relying on natural gas-positioning revenue for durable growth.

- The deployment of advanced drilling and completion technologies, including successful wellbore redesigns, simul-frac fleets, and longer laterals, has reduced per-foot costs (notably a 12% YoY cost drop in the Permian) and improved capital efficiency, creating sustainable improvements in net margins and free cash flow.

- The company's diversified commodity mix and focus on differentiated, higher-value marketing strategies (such as long-term gas sales to power plants and select LNG contracts) help stabilize cash flow and realized prices, mitigating earnings volatility and expanding gross margins through commodity cycles.

- Coterra's substantial Tier 1 inventory and ongoing delineation of new zones across its asset base mean the company can continue to allocate capital efficiently at low reinvestment rates, supporting long-term production sustainability and above-average returns on invested capital, which underpin positive outlooks for earnings and free cash flow.

- Prudent capital allocation, as seen by prioritizing rapid deleveraging followed by anticipated increases in share buybacks and dividends, enhances the EPS growth profile and shareholder value creation, particularly as the balance sheet strengthens and more free cash flow is directed to shareholder returns.

Coterra Energy Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Coterra Energy's revenue will grow by 15.2% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 25.3% today to 19.5% in 3 years time.

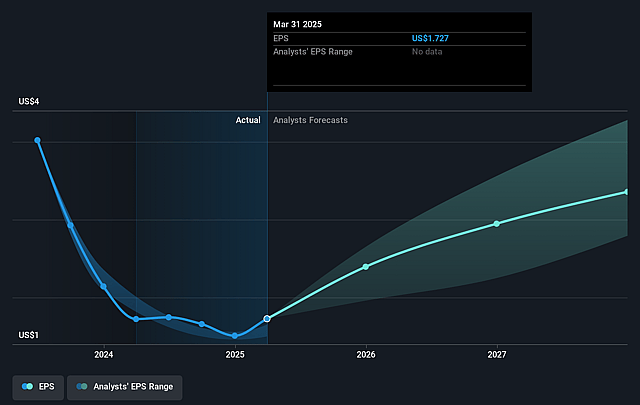

- Analysts expect earnings to reach $1.9 billion (and earnings per share of $2.62) by about August 2028, up from $1.6 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $3.4 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 18.8x on those 2028 earnings, up from 11.2x today. This future PE is greater than the current PE for the US Oil and Gas industry at 12.8x.

- Analysts expect the number of shares outstanding to grow by 3.6% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.1%, as per the Simply Wall St company report.

Coterra Energy Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's expanded activity in the Marcellus and increasing natural gas production guidance comes amid ongoing weakness and volatility in natural gas prices, and there is risk of oversupply in the U.S. market; if structural low prices persist, this could compress long-term revenues and net margins.

- Despite recent successes in remediation, mechanical and pressure issues in Culberson (Windham Harkey wells) have not fully resolved, and original predrill oil volumes may not be achieved, suggesting operational risks and potential underperformance in future output and cash flow durability.

- Management's expectation that federal lease sales in New Mexico will meaningfully add to the asset base hinges on winning competitive bids in an environment of rising acreage prices and new regulations, which could inflate acquisition and compliance costs, impacting future capital efficiency and earnings.

- Growing focus on differentiated power and LNG sales is positive, but Coterra repeatedly emphasizes unwillingness to commit to long-term in-basin pricing or infrastructure expansion without price premiums; this may limit market access and flexibility as demand growth increasingly comes from outside core basins, risking lost revenue opportunities if the global energy transition accelerates.

- Plans for steady production growth and robust free cash flow are premised on "stable operational cadence" and high-quality inventory, yet management acknowledges that a future decline in Tier 1 inventory will increase cost structures; if Coterra cannot replace reserves fast enough or if key wells underperform, this would raise costs and depress margins over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $33.52 for Coterra Energy based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $40.0, and the most bearish reporting a price target of just $26.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $9.5 billion, earnings will come to $1.9 billion, and it would be trading on a PE ratio of 18.8x, assuming you use a discount rate of 7.1%.

- Given the current share price of $23.1, the analyst price target of $33.52 is 31.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.