Key Takeaways

- Strategic acquisition and expanding partnerships are expected to enhance operational efficiencies, diversify revenue streams, and support steady earnings growth.

- Strong contractual commitments and financial health bolster revenue stability, shareholder value, and investor confidence.

- Potential setbacks in water solutions and refinancing risks could strain growth, while substantial capital expenditures may impact free cash flow.

Catalysts

About Aris Water Solutions- An environmental infrastructure and solutions company, provides water handling and recycling solutions to oil and natural gas operators in the United States.

- Strategic acquisition of the McNeill Ranch provides long-term operational advantages and potential cost savings by eliminating royalties, which will positively impact net margins and future free cash flow.

- Expansion into industrial water treatment and beneficial reuse projects in collaboration with major partners like ExxonMobil and Chevron, indicating potential to diversify revenue streams and enhance overall company earnings.

- High level of contracted water volumes, with over 80% of forecasted Water Solutions volumes under long-term contracts, provides revenue visibility and stability, which supports future earnings growth.

- Anticipated production growth from long-term contracted customers in the Permian Basin, with a forecasted increase in produced water volumes and Water Solutions activity, is expected to boost revenue and support steady EBITDA growth.

- Significant increase in dividend payouts and low leverage indicate solid financial health and a focus on returning value to shareholders, which can positively impact earnings per share and attract investor confidence.

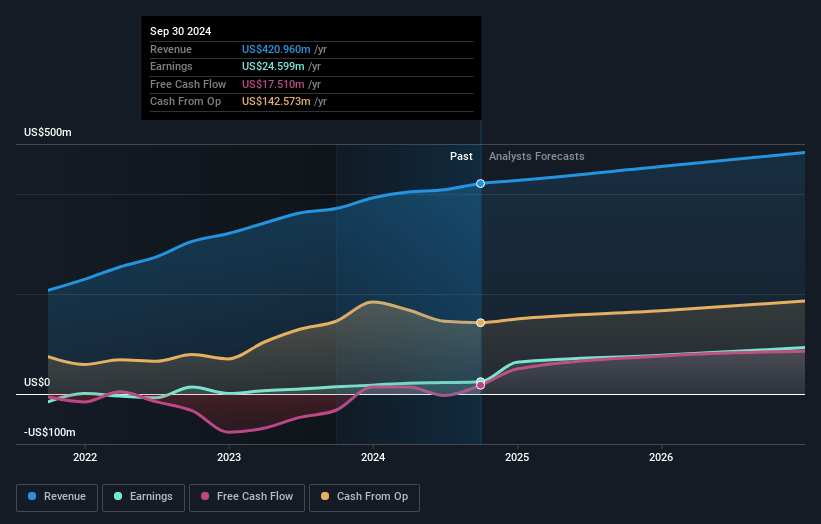

Aris Water Solutions Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Aris Water Solutions's revenue will grow by 11.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.7% today to 19.8% in 3 years time.

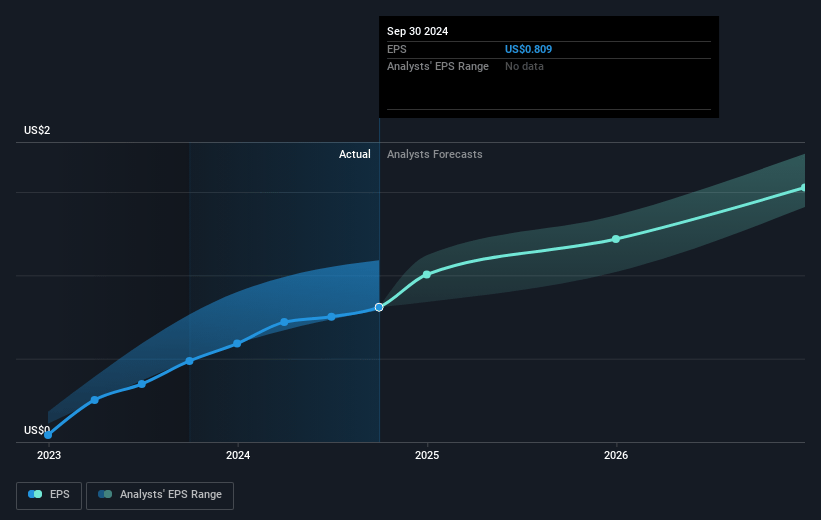

- Analysts expect earnings to reach $118.4 million (and earnings per share of $1.67) by about March 2028, up from $24.9 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 19.7x on those 2028 earnings, down from 34.9x today. This future PE is greater than the current PE for the US Energy Services industry at 12.6x.

- Analysts expect the number of shares outstanding to grow by 1.39% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.72%, as per the Simply Wall St company report.

Aris Water Solutions Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The potential delays in water solutions volumes due to unexpected well completion downtime and weather-related impacts could negatively affect projected revenue and EBITDA growth.

- The forecasted decrease in skim oil prices by approximately 7% could impact net margins and overall earnings from the Water Solutions business.

- Significant upcoming capital expenditures, like the development of the McNeill Ranch, could strain free cash flow if not properly underwritten by long-term contracts with strong margins.

- The need to refinance $400 million of senior notes, scheduled to go current in April, introduces refinancing risk which could affect net margins if interest rates are unfavorable.

- The approval and implementation timeframe for beneficial reuse and mineral extraction projects might be delayed, affecting projected future revenues and diversification efforts until regulatory permits are granted and technological systems are fully operational.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $30.273 for Aris Water Solutions based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $35.0, and the most bearish reporting a price target of just $25.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $597.5 million, earnings will come to $118.4 million, and it would be trading on a PE ratio of 19.7x, assuming you use a discount rate of 8.7%.

- Given the current share price of $28.04, the analyst price target of $30.27 is 7.4% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives