Narratives are currently in beta

Key Takeaways

- Revenue decline in Talent Solutions and shrinking margins may impact Robert Half's growth and earnings prospects.

- Rising SG&A costs and economic uncertainty could further pressure profitability and hiring demand.

- Protiviti's growth, efficient resource management, and favorable economic conditions position Robert Half for increased revenue and profitability amid strong talent demand.

Catalysts

About Robert Half- Provides talent solutions and business consulting services in North America, South America, Europe, Asia, and Australia.

- Robert Half's revenue guidance suggests a year-over-year decline, indicating potential challenges in growth recovery across its Talent Solutions division, which might dampen future revenue prospects.

- The company is experiencing downward pressure on gross margins within its Talent Solutions division due to a decrease in higher-margin permanent placement revenues, which could impact future earnings.

- SG&A costs as a percentage of revenues have been rising, indicating a potential drag on net margins and overall profitability moving forward.

- Protiviti is facing potential revenue growth constraints due to the winding down of large projects, which may lessen its contribution to overall company earnings in upcoming quarters.

- Economic uncertainty, especially surrounding the upcoming U.S. elections, might delay hiring demand, potentially affecting future revenue flow and growth rate expectations across Robert Half's divisions.

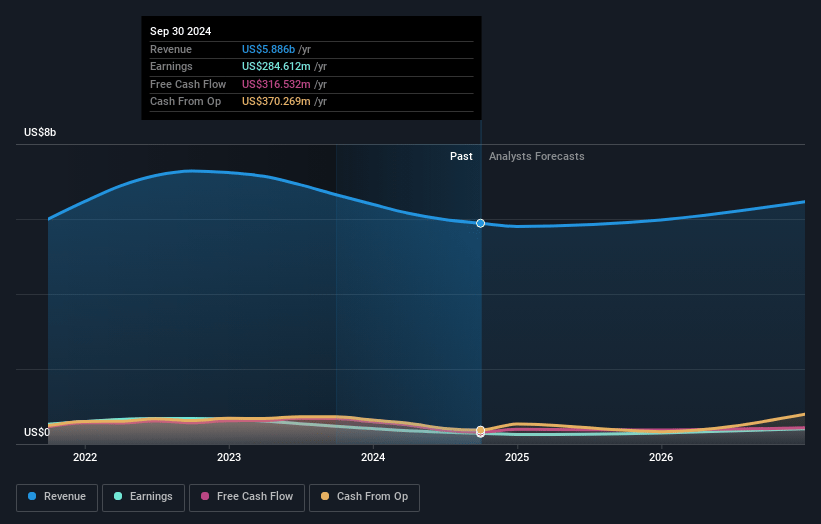

Robert Half Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Robert Half's revenue will grow by 5.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.8% today to 6.9% in 3 years time.

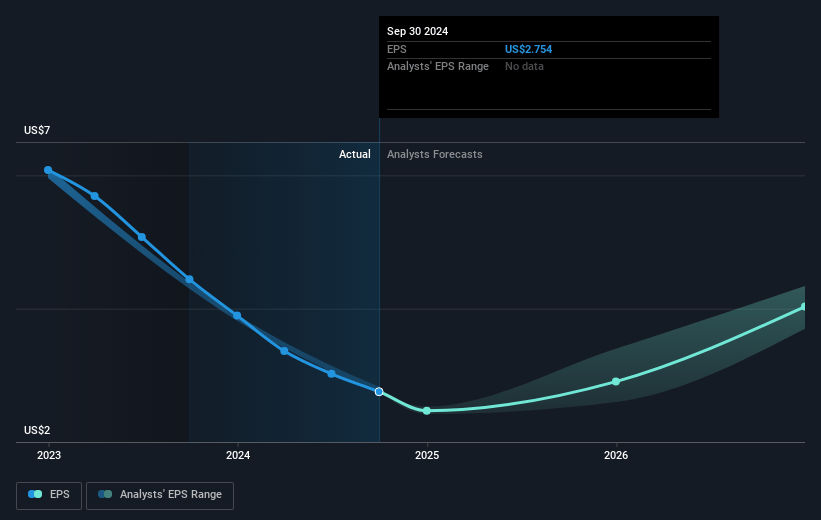

- Analysts expect earnings to reach $467.1 million (and earnings per share of $4.99) by about November 2027, up from $284.6 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 15.5x on those 2027 earnings, down from 27.4x today. This future PE is lower than the current PE for the US Professional Services industry at 26.9x.

- Analysts expect the number of shares outstanding to decline by 2.65% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.31%, as per the Simply Wall St company report.

Robert Half Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Protiviti, Robert Half's consulting division, reported very strong results with sequential and year-on-year revenue growth, particularly in the United States, indicating strong performance and resilience even as other parts of the company may face challenges. This could positively impact overall company revenue and earnings.

- Protiviti's significant use of contract talent solutions represents a key competitive advantage that contributes to efficient resource management and may drive future revenue as Protiviti's demand continues to grow. This could lead to improved profit margins.

- Business confidence is reported to be improving, supported by progress on inflation and a global rate-cutting cycle, which may enhance client demand for Robert Half's services and drive increased revenue as economic conditions become more favorable.

- The company has maintained and effectively managed its internal staffing, focusing on retaining top producers and enhancing productivity through technology investments, which positions Robert Half to capitalize on growth opportunities and improve net margins as demand rebounds.

- The labor market remains tight, particularly for highly skilled roles, and unfulfilled demand for talent combined with Robert Half's strong brand and recruitment capabilities could lead to sustained or increased client engagement, boosting revenue and supporting margin improvement.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $64.7 for Robert Half based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $80.0, and the most bearish reporting a price target of just $53.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $6.8 billion, earnings will come to $467.1 million, and it would be trading on a PE ratio of 15.5x, assuming you use a discount rate of 6.3%.

- Given the current share price of $76.8, the analyst's price target of $64.7 is 18.7% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives