Key Takeaways

- Robust backlog growth and strategic initiatives in high-demand sectors are expected to drive strong future revenue and profitability for Jacobs.

- Operational efficiencies and strategic investments in consulting could enhance net margins and support long-term earnings and EPS growth.

- Delays in customer spending and procurement influenced by macroeconomic factors may impede Jacobs' sequential revenue growth despite a strong project backlog.

Catalysts

About Jacobs Solutions- Engages in the infrastructure and advanced facilities, and consulting businesses in the United States, Europe, Canada, India, Asia, Australia, New Zealand, the Middle East, and Africa.

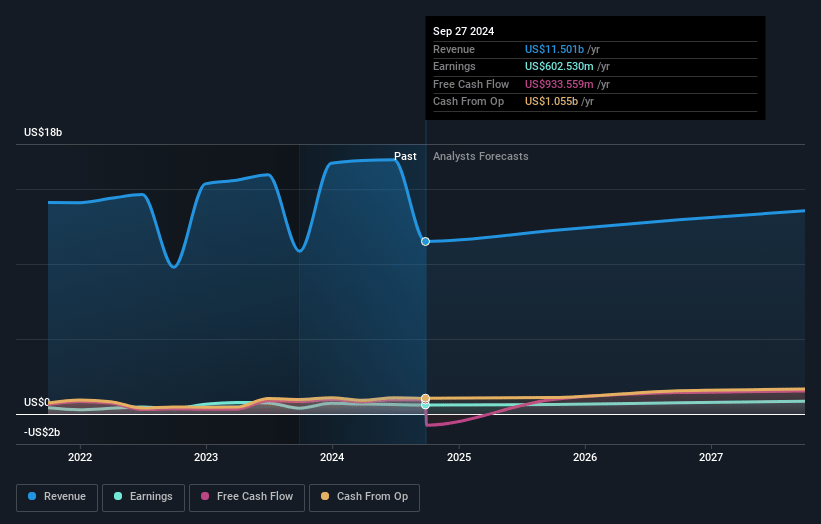

- The significant growth in Jacobs' backlog, which reached a record $22.2 billion (up 20% year-over-year), suggests strong future revenue streams as these projects are realized. This backlog growth indicates robust demand across Jacobs' end markets, providing visibility into future revenue growth.

- Jacobs' initiatives in high-demand sectors such as Water and Environmental, Life Sciences, and Advanced Manufacturing, including data centers and semiconductor facilities, are expected to drive further revenue growth and profitability due to the essential nature of these projects and the company's leading position in these markets.

- The company's efforts to expand adjusted EBITDA margin through improved utilization rates and operational efficiencies—including digital enablement and global delivery models—should positively impact net margins and overall earnings, setting the stage for improved financial performance.

- Planned increased investment in PA Consulting reflects Jacobs' strategy to deepen their capabilities in consulting and advisory services, particularly in Energy & Utilities and Life Sciences. This could drive higher-margin revenue and support the company's long-term earnings growth.

- Jacobs' commitment to capital returns, evidenced by record share repurchases and the planned distribution of Amentum shares, coupled with anticipated strong free cash flow generation, suggests potential upside to earnings per share (EPS) growth as the company continues to manage its capital structure efficiently.

Jacobs Solutions Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Jacobs Solutions's revenue will grow by 11.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.0% today to 7.1% in 3 years time.

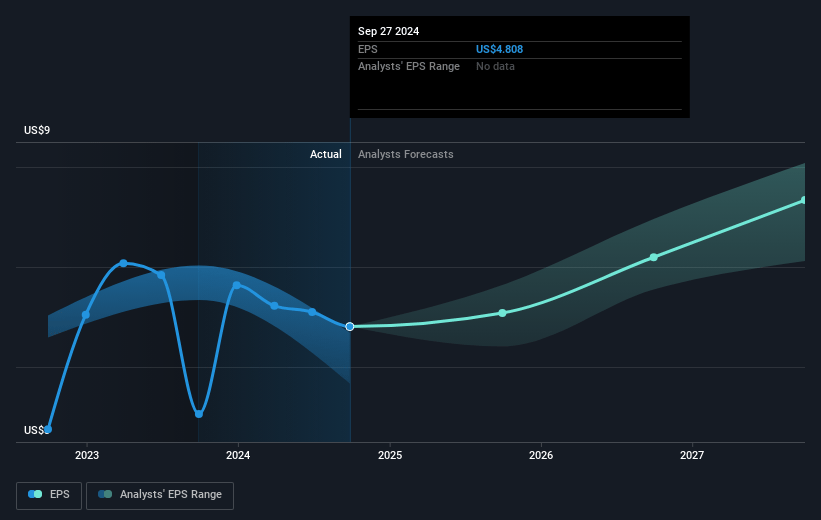

- Analysts expect earnings to reach $1.0 billion (and earnings per share of $8.93) by about May 2028, up from $303.6 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $724 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 18.8x on those 2028 earnings, down from 48.2x today. This future PE is lower than the current PE for the US Professional Services industry at 21.2x.

- Analysts expect the number of shares outstanding to decline by 3.86% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.77%, as per the Simply Wall St company report.

Jacobs Solutions Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Concerns over the legal reserve involving a joint venture project could affect perceptions of Jacobs' risk management practices, potentially impacting net revenue if similar issues arise in the future.

- Foreign exchange headwinds were noted as having negatively impacted revenue growth in Q2, which could continue to affect earnings if currency volatility persists.

- Despite a strong backlog of projects, delays in customer spending decisions and procurement cycles driven by macroeconomic factors could impede the expected sequential revenue growth in the second half of 2025.

- Although Jacobs is experiencing significant growth in certain regions, such as the Middle East and India, potential geopolitical and market instabilities in these areas could pose risks to sustained revenue growth.

- While Jacobs has diversified its project portfolio, further reliance on large-scale, long-duration contracts might limit near-term revenue recognition and affect overall earnings if market demands shift.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $144.494 for Jacobs Solutions based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $175.0, and the most bearish reporting a price target of just $123.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $14.2 billion, earnings will come to $1.0 billion, and it would be trading on a PE ratio of 18.8x, assuming you use a discount rate of 6.8%.

- Given the current share price of $119.47, the analyst price target of $144.49 is 17.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.