Key Takeaways

- Increased focus on adaptable, ergonomic office solutions and premium product lines supports HNI’s profitability and resilience in evolving work environments.

- Strategic acquisitions, production efficiencies, and digital sales expansion are set to drive margin gains, stable earnings, and long-term growth opportunities.

- Shifting work trends, economic uncertainty, market competition, and challenging housing conditions threaten HNI’s growth, profit margins, and long-term demand for its core products.

Catalysts

About HNI- Engages in the manufacture, sale, and marketing of workplace furnishings and residential building products primarily in the United States and Canada.

- Demand for adaptable office solutions is expected to increase as organizations modernize spaces to accommodate flexible and hybrid work models, providing ongoing revenue tailwinds for HNI’s Workplace Furnishings segment.

- Companies are placing greater emphasis on employee well-being, leading to increased investment in ergonomic and health-focused furnishings, positioning HNI for sustained volume growth and potential pricing power, which should boost gross margins and net earnings.

- Operational synergies from strategic acquisitions (such as KII) and ongoing investments in production efficiency, particularly in the Mexico facility, are expected to contribute material EPS and free cash flow gains through 2026 via lower costs and improved margins.

- HNI’s strong positioning in premium and high-margin product lines, especially in resilient end markets like residential remodel-retrofit and custom high-end products, supports above-average profitability and earnings stability even in mixed macro environments.

- Expansion and strengthening of digital sales channels and dealer networks are projected to accelerate top-line growth by tapping new customer segments and markets, while supporting cost efficiency improvements and maintaining a strong balance sheet for reinvestment.

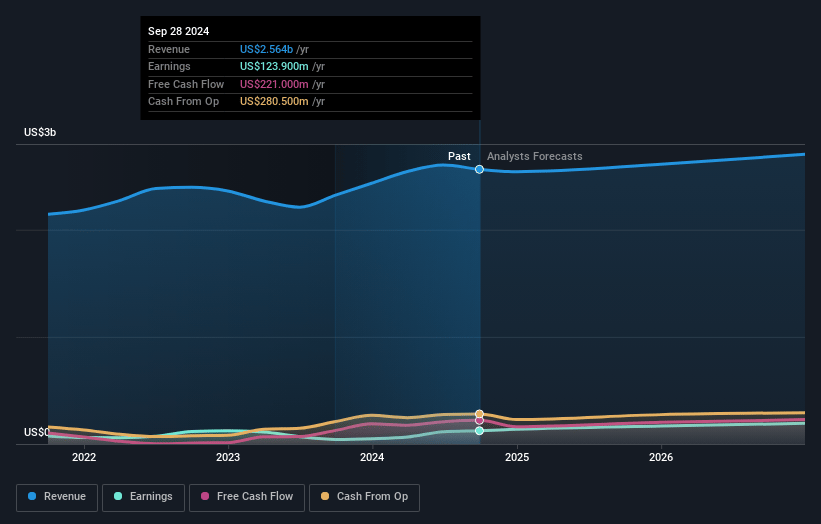

HNI Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming HNI's revenue will grow by 4.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.3% today to 8.4% in 3 years time.

- Analysts expect earnings to reach $239.3 million (and earnings per share of $5.0) by about May 2028, up from $135.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 13.9x on those 2028 earnings, down from 16.3x today. This future PE is lower than the current PE for the US Commercial Services industry at 26.1x.

- Analysts expect the number of shares outstanding to decline by 1.57% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.91%, as per the Simply Wall St company report.

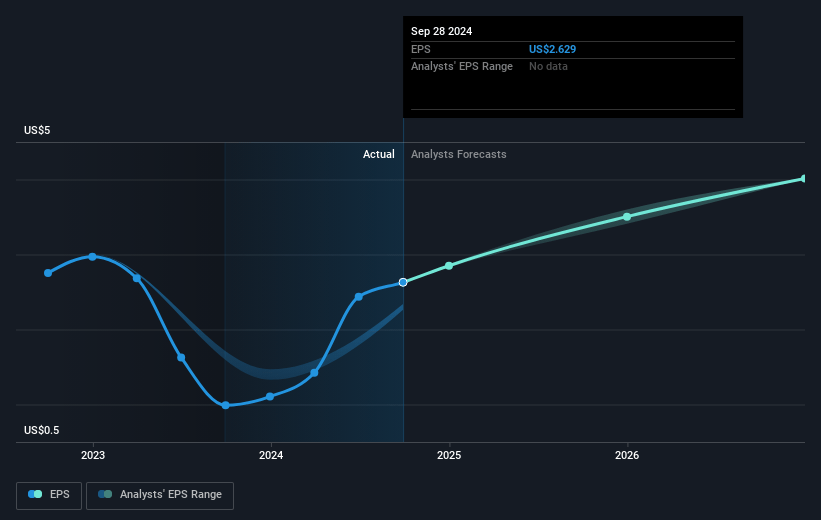

HNI Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Persistent macroeconomic uncertainty and demand volatility, particularly in the small

- and medium-sized business (SMB) sector, could lead to inconsistent order activity and pressure on revenue growth in HNI’s Workplace Furnishings segment.

- The ongoing shift toward hybrid and remote work may structurally reduce long-term demand for traditional office furniture, potentially limiting revenue growth and contributing to downward pressure on long-term earnings.

- Rising tariffs, inflation expectations, and associated pricing actions introduce margin compression risk and may not be fully offset by surcharges or list price adjustments, pressuring net margins and profitability.

- Challenging housing market dynamics—including elevated interest rates, weak builder sentiment, and subdued consumer confidence—pose a long-term risk to growth in the Residential Building Products segment, potentially slowing sales and earnings momentum if housing recovery remains delayed.

- Increasing industry competition, pricing pressure from larger or more vertically integrated rivals, and architectural shifts toward more modular or lower-spend workspaces could erode HNI’s market share and gross margins over time, impacting both revenue and net earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $62.0 for HNI based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $2.9 billion, earnings will come to $239.3 million, and it would be trading on a PE ratio of 13.9x, assuming you use a discount rate of 6.9%.

- Given the current share price of $47.44, the analyst price target of $62.0 is 23.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.