Key Takeaways

- Strategic partnerships and acquisitions are poised to drive revenue growth, market expansion, and enhanced earnings through cross-selling opportunities and new market entries.

- Efficiency gains and financial strategies, such as automation and share repurchases, are anticipated to improve operational margins and enhance earnings per share.

- Heavy reliance on large healthcare deals and share repurchases may risk financial stability, while regulatory shifts and international expansion pose potential growth challenges.

Catalysts

About SS&C Technologies Holdings- Provides software products and software-enabled services to financial services and healthcare industries.

- The strategic lift-out agreement with Insignia Financial in Australia, with expected significant revenue contributions starting in the second half of 2025, indicates potential for substantial revenue growth and market expansion in the superannuation sector.

- Continuous investment in sales and marketing, which has increased significantly over the past few years, is expected to drive higher organic growth by improving client acquisition and market penetration, likely impacting revenue positively.

- The acquisition of Battea and its integration presents cross-selling opportunities that could drive additional revenue, especially with the rise in class action lawsuits, potentially impacting SS&C’s earnings positively.

- Automation through the Blue Prism initiative is creating substantial cost savings, projected to save between $150 million to $200 million, which can improve operational efficiencies and increase net margins.

- The company’s planned share repurchases and prudent tax strategies are likely to enhance earnings per share (EPS), as evidenced by share buybacks and the adjustment of the tax rate contributing to higher reported EPS.

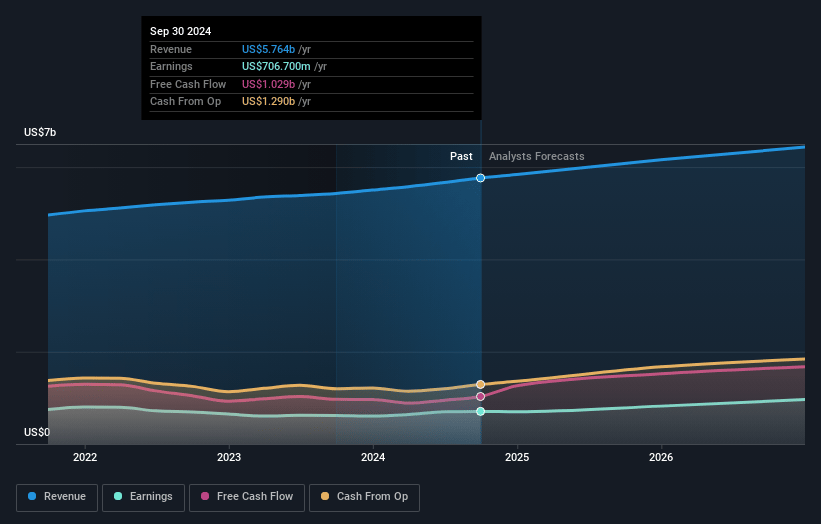

SS&C Technologies Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming SS&C Technologies Holdings's revenue will grow by 4.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 12.9% today to 16.4% in 3 years time.

- Analysts expect earnings to reach $1.1 billion (and earnings per share of $4.26) by about April 2028, up from $760.5 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $961.8 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 25.6x on those 2028 earnings, up from 24.5x today. This future PE is greater than the current PE for the US Professional Services industry at 19.7x.

- Analysts expect the number of shares outstanding to decline by 0.34% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.04%, as per the Simply Wall St company report.

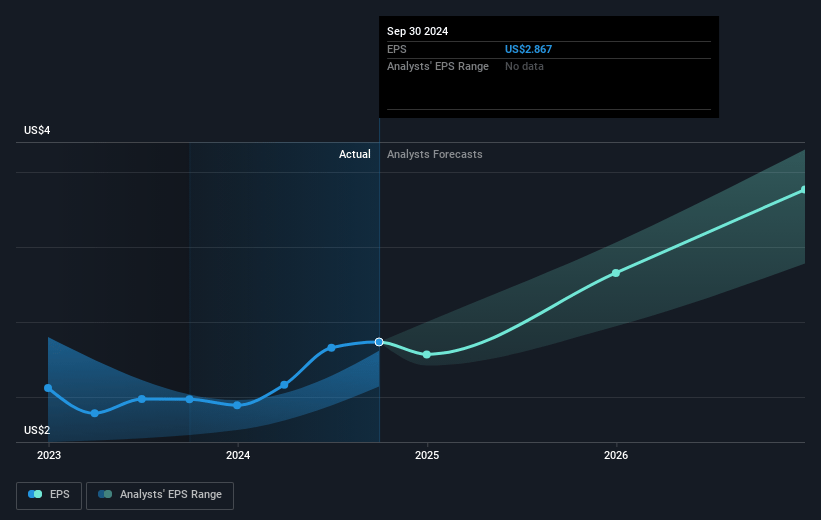

SS&C Technologies Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The concentration of large, lumpy deals in the healthcare segment suggests potential volatility and unpredictability in future revenues. A few large license deals improved Q4, but the business could face challenges if such deals do not repeat consistently. (Impact: Revenue volatility)

- The company's high dependency on share repurchases over debt reduction as capital allocation may reduce financial flexibility. While beneficial short-term, it could expose the company to risks if market conditions change or debt levels become unsustainable. (Impact: Long-term financial health)

- Cost increases in incentives, compensation, and wages added $72 million in expenses in Q4 '24, which could pressure net margins if not matched by proportional revenue growth. (Impact: Net margins)

- The potential shift in regulations, such as those mentioned in the European Commission's decision to cut corporate reporting requirements, might reduce demand for regulatory or compliance-related services offered by SS&C. (Impact: Revenue from regulatory services)

- Execution risk in international expansions, like the new opportunities in Australia's superannuation market, may lead to unanticipated costs or slower-than-expected growth if the company fails to integrate or ramp up operations effectively. (Impact: Earnings and operational efficiency)

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $95.717 for SS&C Technologies Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $105.0, and the most bearish reporting a price target of just $75.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $6.8 billion, earnings will come to $1.1 billion, and it would be trading on a PE ratio of 25.6x, assuming you use a discount rate of 7.0%.

- Given the current share price of $75.49, the analyst price target of $95.72 is 21.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.