Key Takeaways

- RCM Health Care and Corrections sectors show growth potential, boosting revenue through strategic partnerships and market expansion.

- Cost-saving measures and large-scale projects in Energy Services and Aerospace & Defense indicate increased margins and future profitability.

- Operational inefficiencies, discrete item impacts, and higher SG&A expenses threaten profitability, while elevated DSO indicates financial liquidity challenges.

Catalysts

About RCM Technologies- Provides business and technology solutions in the United States, Canada, Puerto Rico, and Europe.

- RCM Health Care is positioned for growth through deepening partnerships with school districts and increasing demand for behavioral health services, which should positively impact revenue.

- Corrections client sector demonstrates impressive growth potential, suggesting expanding revenue opportunities in that market.

- Positive growth in managed service contracts, alongside cost savings measures such as offshore delivery and productivity tools, indicates potential for increased net margins and earnings.

- Advancements in Energy Services with significant new large-scale projects and teaming agreements suggest future revenue growth.

- Aerospace & Defense group expansion with new multiyear contracts and increased headcount suggests continued revenue growth and increased profitability through 2025 and 2026.

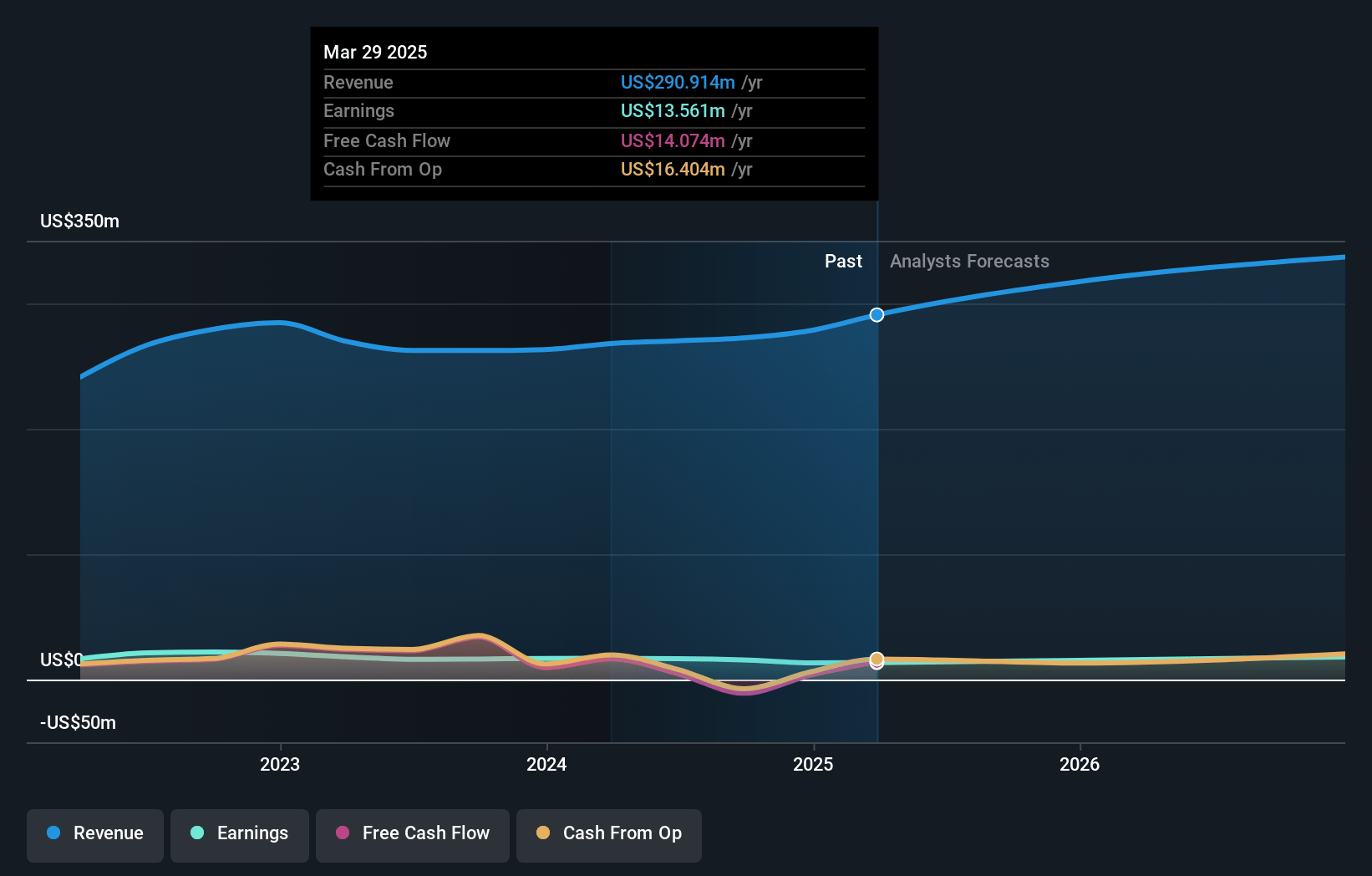

RCM Technologies Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming RCM Technologies's revenue will grow by 6.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.8% today to 6.3% in 3 years time.

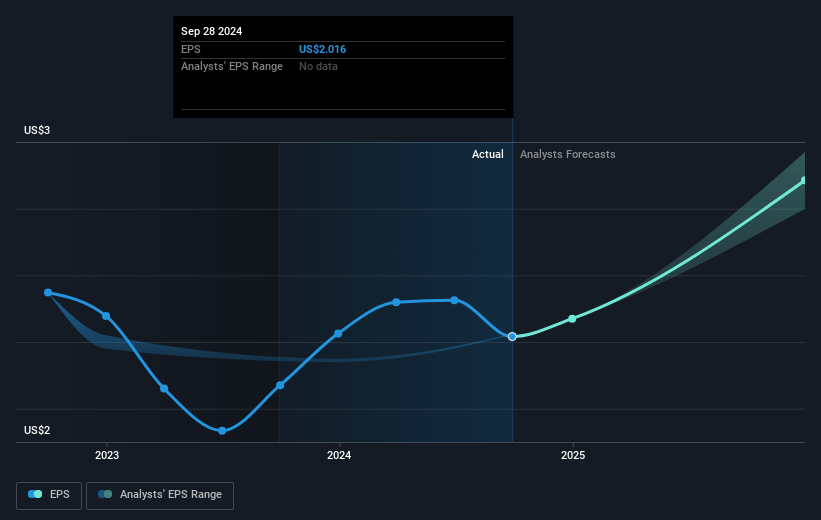

- Analysts expect earnings to reach $21.4 million (and earnings per share of $2.57) by about April 2028, up from $13.3 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.0x on those 2028 earnings, up from 9.2x today. This future PE is lower than the current PE for the US Professional Services industry at 20.8x.

- Analysts expect the number of shares outstanding to decline by 2.13% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.98%, as per the Simply Wall St company report.

RCM Technologies Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's profitability was impacted by significant discrete items in Q4, including project cancellations and rework issues, leading to reduced gross profit by approximately $900,000. This poses a risk to future net margins and earnings if such occurrences continue.

- The volatility in the engineering segment's gross margins, where margins fell from 27.0% to 19.7% year-over-year, indicates susceptibility to fluctuations in project mix and unexpected costs, potentially affecting overall profitability.

- The abrupt cancellation of an industrial process equipment order and significant rework in the Technical Publications group points to potential operational inefficiencies or client pressures that could negatively affect revenue consistency and predictability.

- The company faced higher SG&A expenses due to unusually high self-insured medical costs as well as costs associated with a class action lawsuit, indicating potential for further unexpected costs that could impact net margins.

- Elevated Day Sales Outstanding (DSO) periods, despite some improvement, suggest challenges in accounts receivable management which could strain cash flow and financial liquidity if not addressed effectively.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $30.0 for RCM Technologies based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $339.5 million, earnings will come to $21.4 million, and it would be trading on a PE ratio of 12.0x, assuming you use a discount rate of 7.0%.

- Given the current share price of $16.18, the analyst price target of $30.0 is 46.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.