Narratives are currently in beta

Key Takeaways

- Strong demand in key markets, alongside new business in energy efficiency, is set to drive revenue growth and improve margins through lucrative business segments.

- Significant opportunities from federal acts and digital modernization pave the way for increased revenue and higher operating margins via government and IT contracts.

- Reliance on government contracts and delayed awards could risk revenue growth, while sustainable tax strategies are needed to maintain net margins amidst competitive bidding challenges.

Catalysts

About ICF International- Provides management, technology, and policy consulting and implementation services to government and commercial clients in the United States and internationally.

- Strong demand in the energy, environment, infrastructure, and disaster recovery markets is expected to drive robust revenue growth, particularly through increased work for commercial energy clients and new clients in energy efficiency and grid resilience. This growth is likely to boost overall revenue and net margins due to higher-margin business portions.

- ICF's record new business development pipeline of $10.6 billion and a healthy 12-month book-to-bill ratio of 1.31 create a solid foundation for future revenue growth and potential earnings expansion over the coming years.

- Ongoing opportunities from the Infrastructure Investment and Jobs Act (IIJA) and Inflation Reduction Act (IRA) are expected to generate significant new business, impacting revenue positively, particularly through government client engagements in climate and clean energy projects.

- Continued investments and expansion in capabilities related to energy efficiency, climate resilience, and disaster recovery, fueled by organic growth and potential tuck-in acquisitions, are likely to improve net margins due to a favorable business mix shift toward more profitable services.

- Potential growth in federal digital modernization efforts, especially with increased focus on AI and data initiatives, suggests additional avenues for revenue increase and higher operating margins, as ICF aims to secure larger IT modernization contracts in the federal space.

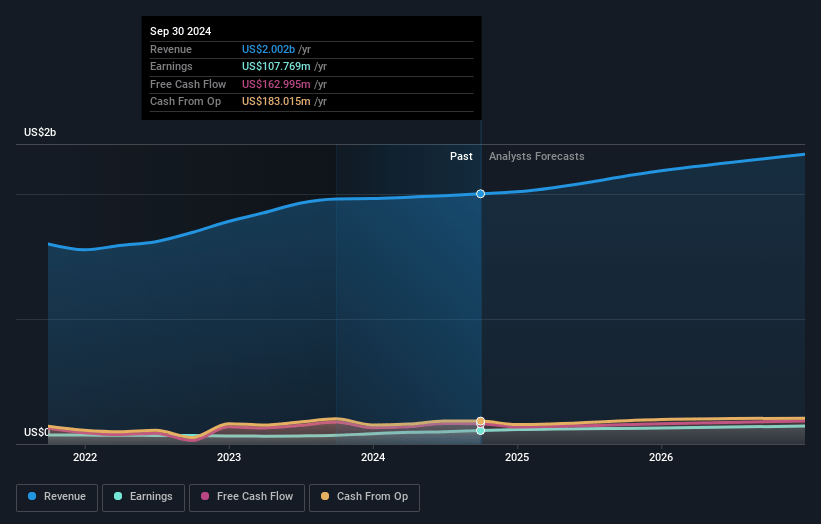

ICF International Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming ICF International's revenue will grow by 6.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.4% today to 6.4% in 3 years time.

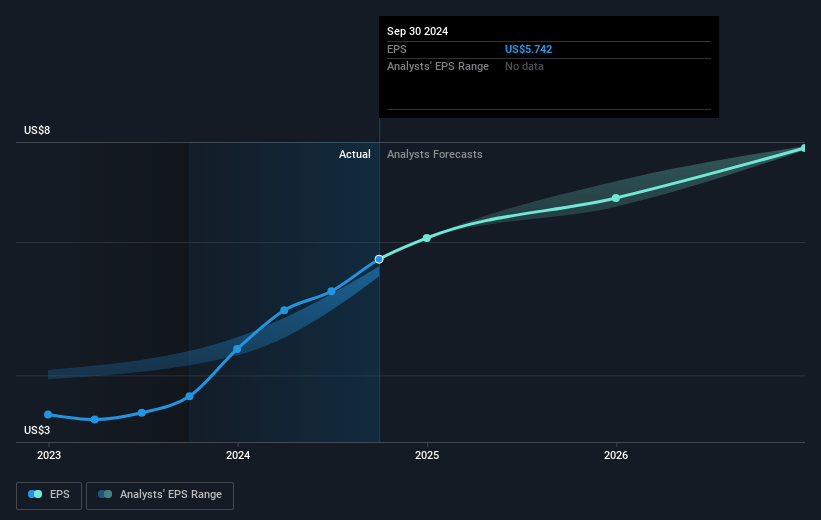

- Analysts expect earnings to reach $157.1 million (and earnings per share of $8.02) by about November 2027, up from $107.8 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 27.9x on those 2027 earnings, down from 29.1x today. This future PE is greater than the current PE for the US Professional Services industry at 26.9x.

- Analysts expect the number of shares outstanding to grow by 1.44% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.6%, as per the Simply Wall St company report.

ICF International Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The decline in revenues from the health and social programs market, including reductions in pass-through revenues and challenges with contract ramp-ups, could pose a risk to future revenue growth.

- Slow ramp-up and delays in key award decisions for certain contracts might result in reduced gross revenue, directly affecting the company's overall revenue projections for 2024.

- Significant reliance on contract awards from government-related programs, such as those related to IIJA and IRA, might create volatility in future revenues if expectations for these awards are not met.

- The tax rate decrease from onetime benefits may not be sustainable long-term, which could affect net margins if advantageous tax optimization strategies are not continually implemented.

- Competitive bidding and elongated capture phases for large federal IT contracts could introduce execution risk and uncertainty in achieving anticipated increases in earnings from these contracts.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $190.5 for ICF International based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $223.0, and the most bearish reporting a price target of just $174.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $2.4 billion, earnings will come to $157.1 million, and it would be trading on a PE ratio of 27.9x, assuming you use a discount rate of 6.6%.

- Given the current share price of $167.34, the analyst's price target of $190.5 is 12.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives