Key Takeaways

- Strategic cost reductions, including in workers' compensation and headcount optimization, are enhancing profitability and improving net margins.

- Leveraging its strong franchise model and diversification through acquisitions positions HireQuest for continued earnings growth and expanded market presence.

- Economic uncertainties and industry challenges pose risks to HireQuest's revenue growth and profitability, notably impacted by a significant noncash impairment charge.

Catalysts

About HireQuest- Provides temporary staffing services in the United States.

- HireQuest is positioned for revenue growth as the temporary staffing market stabilizes and begins to see a leveling out of compressed demand, potentially driving an increase in system-wide sales.

- The company has achieved significant cost reductions, particularly in workers' compensation expenses, decreasing nearly 67% year-over-year, which could improve net margins by lowering SG&A expenses.

- By capitalizing on its existing franchise model, which has demonstrated strength and versatility against industry headwinds, HireQuest could continue to outperform peers in terms of earnings growth.

- The company's strategic focus on expense management, including a reduction in salaries through headcount optimization, could enhance profitability, positively impacting net margins.

- HireQuest plans to leverage acquisitions and expand into permanent placement and executive recruiting, aiming for diversified growth opportunities that could increase future earnings.

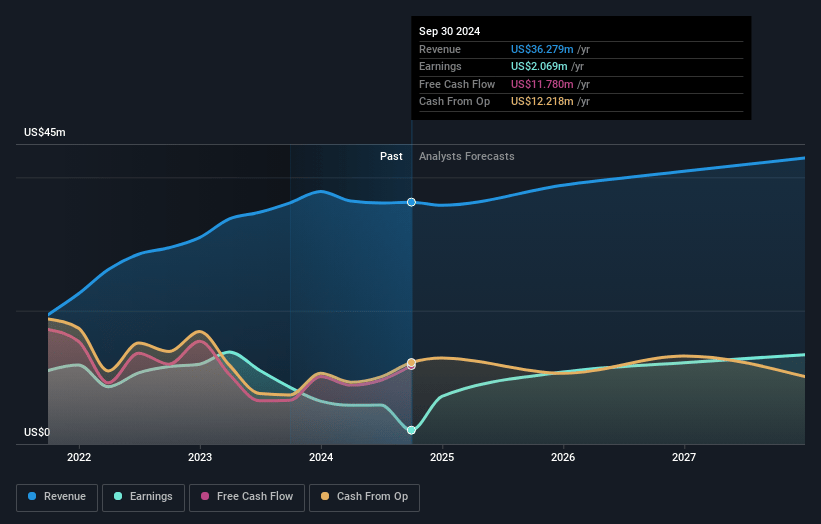

HireQuest Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming HireQuest's revenue will grow by 5.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.7% today to 30.9% in 3 years time.

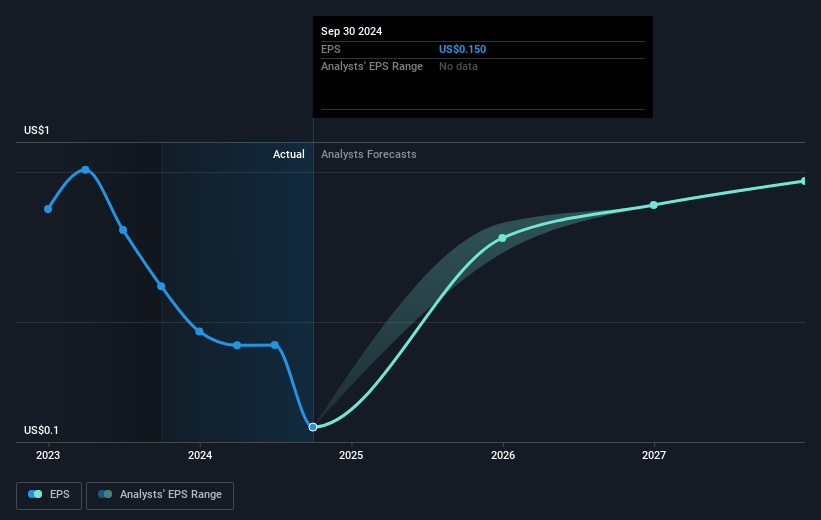

- Analysts expect earnings to reach $13.1 million (and earnings per share of $0.95) by about March 2028, up from $2.1 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 24.7x on those 2028 earnings, down from 89.4x today. This future PE is greater than the current PE for the US Professional Services industry at 21.7x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.69%, as per the Simply Wall St company report.

HireQuest Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The staffing industry has faced a difficult environment recently, with employers remaining cautious in their hiring decisions due to the presidential election and an unpredictable economic landscape, potentially affecting HireQuest's future revenue growth.

- The influx of undocumented workers into the lower-tier labor force creates uncertainty about labor dynamics, which could impact the demand for HireQuest’s temporary staffing solutions and ultimately their revenue.

- The market for permanent placement and executive recruiting, a significant growth opportunity for HireQuest, has faced industry-wide challenges and a downturn, which has affected the company’s profitability through the need for a noncash impairment charge, impacting net margins.

- The $6 million noncash impairment charge related to MRI Network assets significantly impacted HireQuest's profitability in the quarter, highlighting potential volatility in earnings results due to the unpredictability of asset performance.

- Changes in interest rates, particularly their potential increase, might lead to uncertainty in the commercial real estate and construction sectors, which are significant drivers of HireQuest's business, potentially affecting future revenues.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $19.0 for HireQuest based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $42.4 million, earnings will come to $13.1 million, and it would be trading on a PE ratio of 24.7x, assuming you use a discount rate of 6.7%.

- Given the current share price of $13.21, the analyst price target of $19.0 is 30.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.