Last Update 15 Dec 25

Fair value Increased 0.84%WFC: Future Returns Will Reflect Fee Strength Amid Ongoing Execution Risks

We raise our Wells Fargo price target modestly to $94.50 from $93.71, reflecting analysts' increased confidence in fee driven earnings strength, improving profitability metrics, and higher medium term return targets following a series of post Q3 estimate and target upgrades.

Analyst Commentary

Recent Street research indicates a generally constructive stance on Wells Fargo, with a series of price target increases following the Q3 print. Analysts are sharpening their focus on the bank's ability to translate fee driven strength and capital return into sustainably higher returns on tangible common equity and, ultimately, valuation re rating.

Bullish Takeaways

- Bullish analysts highlight the Q3 core EPS beat, driven by stronger than expected fee revenue and reserve releases, as evidence that earnings power is tracking ahead of prior expectations.

- The introduction of a new medium term ROTCE target in the high teens is viewed as a key catalyst. This reinforces confidence that improving efficiency and capital deployment can support a higher valuation multiple.

- Upward revisions to outer year EPS estimates, including assumptions for stronger second half fee revenues and a faster pace of share buybacks, underpin higher price targets and a more constructive total return outlook.

- Stronger fee performance relative to expectations in Q3 is seen as an important sign of revenue diversification, reducing reliance on net interest income and improving the durability of the growth narrative.

Bearish Takeaways

- Bearish analysts remain cautious on the sustainability of fee strength and reserve driven beats, emphasizing that future quarters will need to demonstrate cleaner, recurring earnings to justify further upside.

- There is ongoing concern that net interest income estimates may still be conservative, but with limited perceived upside. This constrains how much earnings revisions can drive additional multiple expansion.

- Some see the new, higher return targets as ambitious, arguing that execution risk around cost control, regulatory progress, and balance sheet optimization could cap valuation at only a modest premium to peers.

- A subset of more cautious voices continues to favor other large banks, viewing Wells Fargo as a relative rather than absolute outperformer until it proves more consistent progress against its medium term objectives.

What's in the News

- Wells Fargo CEO Charlie Scharf said the bank is not under pressure to pursue acquisitions now that a key regulatory penalty has been lifted, and he emphasized organic growth opportunities across existing businesses (Reuters).

- The company announced a new $570 million, energy net positive campus in Las Colinas, Irving, Texas, bringing together 4,500 employees and underscoring its long term commitment to the Dallas Fort Worth region and sustainable operations.

- Wells Fargo reached a proposed $33 million global settlement, subject to court approval, in consolidated lawsuits alleging it assisted subscription related entities that misled consumers by facilitating bank accounts and fund transfers.

- From July 1 to September 30, 2025, Wells Fargo repurchased over 74 million shares across two buyback authorizations, deploying roughly $6 billion and bringing total buybacks since July 2023 to more than $30 billion.

- The company reaffirmed 2025 guidance that net interest income should be roughly in line with 2024, and it reported Q3 2025 net loan charge offs of $942 million, down from $1.11 billion a year earlier.

Valuation Changes

- Fair Value: risen slightly to $94.50 from $93.71, reflecting modestly higher projected intrinsic value.

- Discount Rate: edged down marginally to 8.19 percent from 8.21 percent, implying a slightly lower required return on equity risk.

- Revenue Growth: trimmed slightly to 6.94 percent from 7.01 percent, indicating a modestly more conservative top line outlook.

- Net Profit Margin: increased fractionally to 25.26 percent from 25.24 percent, signaling a small improvement in expected profitability.

- Future P/E: moved up modestly to 13.38x from 13.26x, suggesting a slightly higher valuation multiple applied to forward earnings.

Key Takeaways

- Regulatory restrictions lifted, enabling aggressive balance sheet growth and expansion across deposits, lending, and wealth management for diversified and robust revenue streams.

- Strategic digital initiatives, expense discipline, and technology investments are driving scalable growth, higher margins, and improved customer satisfaction, strengthening long-term competitiveness.

- Competitive and regulatory pressures, slow digital transformation, and changing consumer preferences threaten Wells Fargo's profitability, efficiency, and long-term deposit and revenue growth.

Catalysts

About Wells Fargo- A financial services company, provides diversified banking, investment, mortgage, and consumer and commercial finance products and services in the United States and internationally.

- The removal of the asset cap and resolution of multiple regulatory orders unlocks Wells Fargo's ability to aggressively grow its balance sheet-including deposits, loans, and trading assets-after years of constraint, likely resulting in higher revenue and earnings growth over the coming quarters and years.

- A strong focus on digital banking and client experience improvements has driven consistent gains in mobile banking adoption, digital account openings, and customer satisfaction, positioning Wells Fargo for scalable growth and cost efficiencies-supporting both revenue growth and net margin expansion as more banking activity shifts online.

- Ongoing U.S. economic growth, solid labor markets, and steady consumer spending trends support loan and deposit demand, with management noting growth in checking accounts, credit cards, and auto lending-all likely to sustain and broaden Wells Fargo's revenue base as population and wealth rise.

- The strategic buildout of wealth management and advisory businesses, including significant net asset flows and affluent client acquisition, should increase fee-based income, support revenue diversification, and drive higher margins, reducing earnings volatility from cyclical lending operations.

- Management reiterated a continued commitment to expense discipline and scalable technology investments, including early-stage AI initiatives, which should offset investment for growth and enable structurally lower efficiency ratios-positively impacting net margins and long-term earnings power.

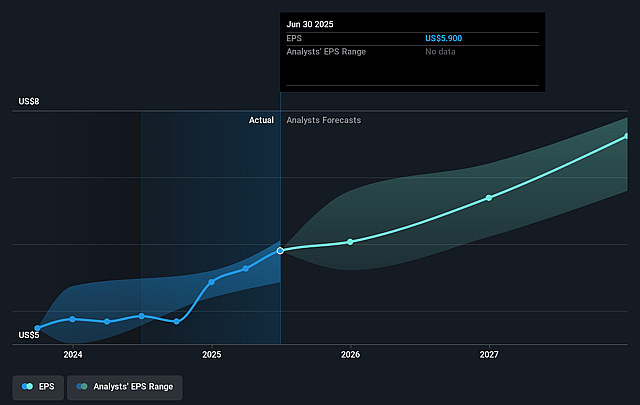

Wells Fargo Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Wells Fargo's revenue will grow by 5.3% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 25.1% today to 24.4% in 3 years time.

- Analysts expect earnings to reach $22.1 billion (and earnings per share of $7.34) by about September 2028, up from $19.5 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 14.3x on those 2028 earnings, up from 13.3x today. This future PE is greater than the current PE for the US Banks industry at 11.9x.

- Analysts expect the number of shares outstanding to decline by 3.79% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.26%, as per the Simply Wall St company report.

Wells Fargo Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Intense competition from both traditional banks and non-bank lenders, combined with limited spread widening in commercial lending, could constrain loan yields and net interest margins, pressuring both revenue growth and future profitability.

- While Wells Fargo is investing heavily in technology and digital platforms, the ramp-up in AI and digital initiatives is still in very early stages; if execution lags or if fintech and big tech competitors outpace Wells Fargo's digital transformation, the company risks customer attrition, lower deposit growth, and higher cost-to-income ratios, negatively impacting earnings and margins over the long term.

- Persistent regulatory and compliance obligations remain a risk despite the removal of the asset cap, as ongoing consent orders continue to require substantial resources, limiting the speed at which Wells Fargo can reduce compliance costs and reinvest in growth, potentially weighing on net margins and efficiency improvements.

- Structural changes in consumer behavior, including the rise of digitally native younger customers who may choose fintechs or non-bank platforms over traditional banks, could limit Wells Fargo's ability to grow core deposits and cross-sell products, challenging long-term revenue and deposit growth.

- The medium

- to long-term interest rate environment remains highly uncertain; any period of sustained low or volatile rates, or increased competition driving up deposit costs, could compress net interest income and slow earnings expansion despite recent improvements in fee income and trading revenues.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $87.0 for Wells Fargo based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $95.0, and the most bearish reporting a price target of just $72.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $90.6 billion, earnings will come to $22.1 billion, and it would be trading on a PE ratio of 14.3x, assuming you use a discount rate of 8.3%.

- Given the current share price of $80.76, the analyst price target of $87.0 is 7.2% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Wells Fargo?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.