Last Update 21 Nov 25

EQBK: Recent Acquisitions And Portfolio Restructuring Will Drive Premium Multiples

Analysts have modestly raised their price target for Equity Bancshares, citing confidence in management's recent acquisitions and portfolio restructuring. These actions are expected to boost profitability and support a new target of $54, up from previous targets near $45.

Analyst Commentary

Recent analyst reports provide a balanced outlook on Equity Bancshares, reflecting confidence in the company’s growth strategies alongside acknowledgment of potential risks that could impact valuation and performance over the coming months.

Bullish Takeaways

- Bullish analysts expect management’s execution on recent acquisitions and significant portfolio restructuring to drive profitability into top quartile levels. This is anticipated to support a higher valuation.

- Expansion into larger Midwest metropolitan areas is anticipated to spur mid-single-digit organic loan growth. This expansion is expected to help reinforce stable core net interest margins despite broader market rate pressures.

- Synergies from recent deals are projected to deliver premium multiples for shares, supported by disciplined pricing strategies that should help mitigate acquirer-related valuation overhangs.

- Analysts anticipate that ongoing execution of compelling deals will continue to enhance the company’s growth, supporting sustained upside in the near-term outlook.

Bearish Takeaways

- Bearish analysts note that, while acquisitions are expected to have a net positive impact on earnings, the corresponding effect on tangible book value could offset some valuation gains in the near term.

- There are concerns about the durability of profitability improvements if synergies from recent transactions or anticipated loan growth fall short of expectations.

- The stability of premium net interest margins may be challenged if broader interest rate cuts by the Federal Reserve exceed current forecasts.

What's in the News

- Equity Bancshares completed a repurchase of 183,232 shares, representing 1.04% of outstanding shares, for $6.8 million as part of the buyback announced on October 8, 2024 (Key Developments).

- The company announced a share repurchase program that allows the buyback of up to 1,000,000 shares of common stock, expiring on September 30, 2026 (Key Developments).

- On September 11, 2025, the Board of Directors declared a quarterly cash dividend of $0.18 per share, payable on October 15, 2025, to stockholders of record as of September 30, 2025 (Key Developments).

- The Board of Directors authorized a new buyback plan on September 11, 2025 (Key Developments).

Valuation Changes

- Fair Value remained steady at $50.20, indicating no change since the last assessment.

- Discount Rate has risen slightly from 7.06% to 7.19%, which suggests a modest increase in the cost of capital assumptions.

- Revenue Growth forecasts are unchanged at approximately 34.17%.

- Net Profit Margin remains effectively stable at 45.66%.

- Future P/E ratio has increased slightly from 6.90x to 6.93x, reflecting a minor shift in market expectations for earnings.

Key Takeaways

- Expansion into high-growth mid-sized markets and strategic M&A enhance geographic reach, scale, and long-term revenue opportunities.

- Investment in digital banking and diversified services improves income mix, operational efficiency, and supports stable earnings growth with strong risk management.

- Rising digital competition, demographic shifts, sector concentration, and regulatory costs threaten long-term growth, profitability, and customer retention for the bank.

Catalysts

About Equity Bancshares- Operates as the bank holding company for Equity Bank that provides a range of banking, mortgage banking, and financial services to individual and corporate customers.

- The company's recent merger with NBC Bank expands its geographic reach into Oklahoma City-one of the Midwest's fastest-growing metro areas-positioning Equity Bancshares to benefit from rising demand for community-focused banking solutions in mid-sized markets; this is likely to drive above-average loan growth and revenue expansion over the long term.

- Accelerated adoption of digital banking tools and improved treasury, debit/credit, mortgage, trust, and wealth management offerings have resulted in increased non-interest income, while ongoing investments in digital platforms are expected to lower operational costs and improve net margins.

- The strong pipeline of commercial and C&I loan originations, alongside continued small business growth in regional economies, supports future commercial lending volume and fee income, which should stabilize and grow both revenue and earnings.

- Strategic consolidation through disciplined M&A (with a pipeline of acquisition targets in the $250 million–$1.5 billion range) provides opportunities for scale, cost synergies, and improved operating leverage, supporting sustained net margin and EPS growth.

- Capital flexibility from recent capital raises and a robust TCE ratio (10%+) allows the company to maintain conservative credit standards and proactively manage credit risk, supporting stable earnings and potential for higher book value compounding.

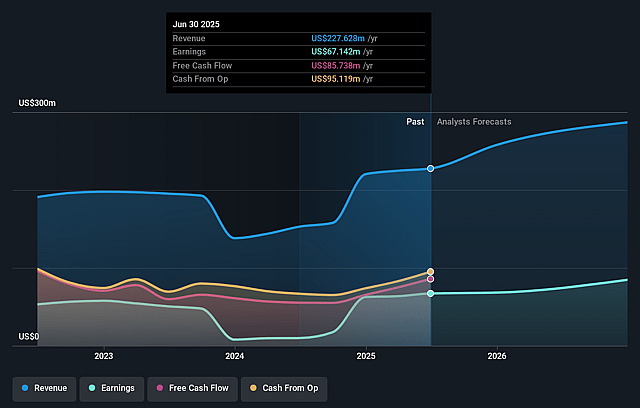

Equity Bancshares Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Equity Bancshares's revenue will grow by 23.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 29.5% today to 34.6% in 3 years time.

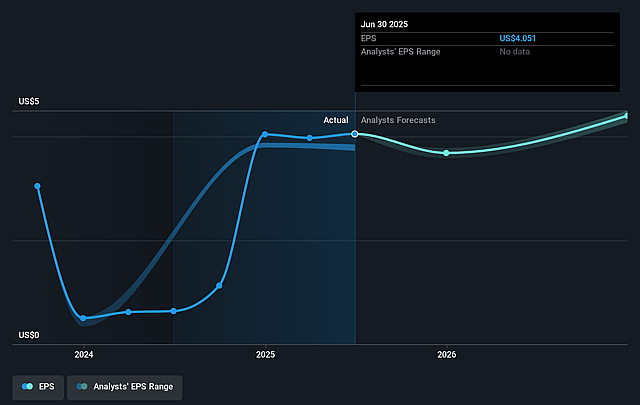

- Analysts expect earnings to reach $146.6 million (and earnings per share of $5.31) by about September 2028, up from $67.1 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 9.4x on those 2028 earnings, down from 12.0x today. This future PE is lower than the current PE for the US Banks industry at 11.9x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.04%, as per the Simply Wall St company report.

Equity Bancshares Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Accelerated shift to digital banking and increased consumer preference for seamless, technology-driven banking services may favor larger national banks and fintechs, potentially leading to customer attrition and stagnating revenue growth for Equity Bancshares if it cannot keep pace with innovation.

- Ongoing demographic trends, such as rural depopulation and the aging of populations in Midwest and South Central U.S. markets, could gradually erode the bank's core customer base, posing long-term risks to both deposit and loan growth (revenue impact).

- High reliance on commercial real estate (CRE) and sector-specific exposures (e.g., the cited QSR relationship and agriculture lending) increases vulnerability to sector downturns, which could result in elevated credit losses and higher non-performing assets, negatively affecting net earnings and asset quality.

- Industry-wide consolidation and M&A activity may favor banks that can achieve rapid scale and digital efficiencies; as a smaller regional player, Equity Bancshares could face rising operational costs and lose market share if unable to compete on technology and pricing, putting downward pressure on net margins.

- Prolonged cost pressures from tightening regulatory and compliance requirements could disproportionately impact smaller community banks like Equity Bancshares, driving up operational expenses and squeezing net margins and profitability over time.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $48.75 for Equity Bancshares based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $54.0, and the most bearish reporting a price target of just $45.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $423.2 million, earnings will come to $146.6 million, and it would be trading on a PE ratio of 9.4x, assuming you use a discount rate of 7.0%.

- Given the current share price of $41.83, the analyst price target of $48.75 is 14.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.