Key Takeaways

- Shifting toward diversified lending, technology upgrades, and efficient integration of acquisitions strengthens earnings stability, operational efficiency, and revenue growth potential.

- A strong, low-cost deposit base and focus on scalable digital delivery position the bank for long-term margin protection and competitive advantage.

- Elevated exposure to commercial real estate, ongoing credit quality concerns, and integration risks threaten profitability amid rising competition and digital transformation pressures.

Catalysts

About Independent Bank- Operates as the bank holding company for Rockland Trust Company that provides commercial banking products and services to individuals and small-to-medium sized businesses in the United States.

- Ongoing U.S. population migration to secondary and smaller metropolitan areas, alongside strong small business formation in core markets, positions Independent Bank to benefit from outsized loan and deposit growth from community banking and small business lending-positively impacting long-term revenue and fee income.

- Sustained investment in core banking technology and a major platform conversion (FIS IBS scheduled for May 2026), paired with a commitment to digital delivery, should enhance operational efficiency and scalability-supporting improved net margins and cost-to-income ratios over time.

- Proactive reduction in commercial real estate (CRE) concentration and strategic shift toward C&I lending diversifies the loan portfolio, reducing earnings volatility and lowering the risk of outsized credit losses-bolstering earnings stability and lowering future credit costs.

- Rapid integration of the Enterprise Bank acquisition, with targeted cost synergies (~30% of expense base) expected in 2026 and a larger, more diversified deposit/loan base, offers scale benefit and cross-sell opportunities-enhancing net interest income and noninterest revenue growth potential.

- Resilient, lower-cost core deposit franchise (seen in consistent growth and disciplined funding costs) provides a structural advantage in a high-rate and competitive environment-helping protect and expand net interest margin and supporting long-term earnings power.

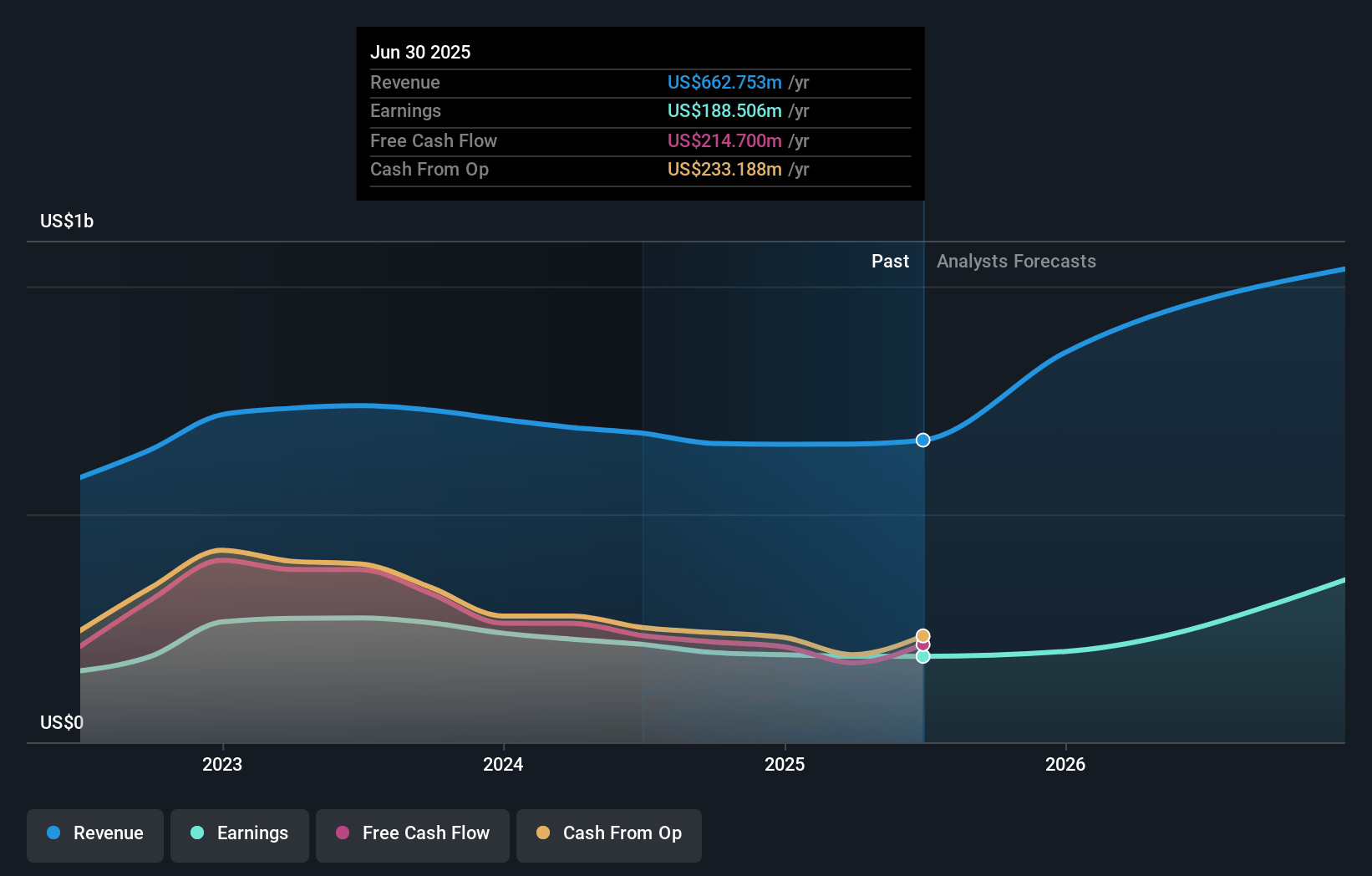

Independent Bank Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Independent Bank's revenue will grow by 32.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 28.4% today to 39.4% in 3 years time.

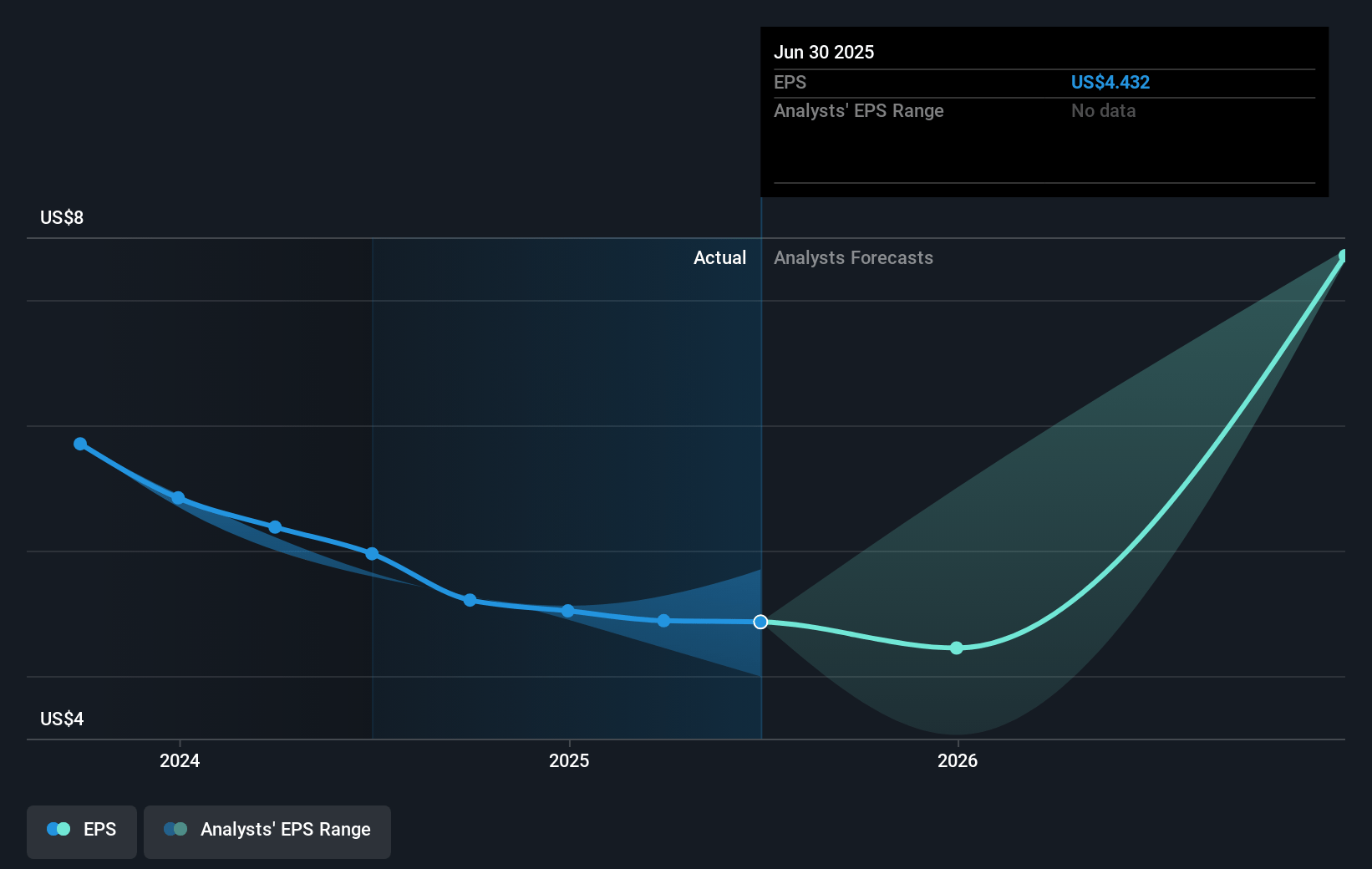

- Analysts expect earnings to reach $613.0 million (and earnings per share of $11.25) by about July 2028, up from $188.5 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 7.8x on those 2028 earnings, down from 18.2x today. This future PE is lower than the current PE for the US Banks industry at 11.9x.

- Analysts expect the number of shares outstanding to grow by 0.34% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.4%, as per the Simply Wall St company report.

Independent Bank Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The continued high concentration in commercial real estate (CRE), especially office loans, exposes Independent Bank to sector-specific risk-management acknowledged ongoing work is needed to reduce this exposure, and with CRE concentration expected to temporarily rise further due to the Enterprise acquisition, the risk of future credit losses remains, potentially pressuring net interest margin and earnings.

- Ongoing credit quality concerns, particularly in the bank's office loan portfolio-with recent loan downgrades, the need for restructuring and payment deferrals, and several large, criticized assets maturing soon-suggest credit costs may increase in the future, which could negatively impact loan loss provisions and net income.

- Integration risk from the recent Enterprise acquisition and planned core technology migration (to FIS IBS in 2026) brings execution uncertainty; delays or higher-than-expected costs could weigh on expense management, synergy realization, and ultimately, on net margins and earnings.

- Rising competitive pressure in both C&I lending and deposit gathering-evidenced by heightened competition from other banks re-entering CRE and aggressive market rates for deposits-could erode loan yields and require higher funding costs, thus compressing net interest margin and overall profitability.

- Secular industry shifts toward digital banking and fintech competition pose long-term threats; if Independent Bank does not make sufficient progress in digital infrastructure or loses market share to more technologically advanced or fee-based service competitors, revenue growth and expense efficiency could be negatively impacted over time.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $79.0 for Independent Bank based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.6 billion, earnings will come to $613.0 million, and it would be trading on a PE ratio of 7.8x, assuming you use a discount rate of 6.4%.

- Given the current share price of $68.51, the analyst price target of $79.0 is 13.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.