Narratives are currently in beta

Key Takeaways

- Unified IT stack and 5G expansion enhance customer experience, competitive position, and revenue through improved offerings and service expansion.

- Strategic cost savings and modern technology transitions boost operational efficiency, stabilize customer base, and positively impact earnings and margins.

- Economic challenges and intense competition in key markets may slow revenue growth, with pricing strategies and energy costs impacting margins and earnings.

Catalysts

About Tele2- Provides fixed and mobile connectivity, handset related data services, and entertainment services in Sweden, Lithuania, Latvia, and Estonia.

- The transition to a unified IT stack for consumer services allows Tele2 to improve customer experience, potentially driving revenue through enhanced service offerings and cross-selling with a 360 customer view and unified channel engagement.

- The introduction of annual pricing aligned with inflation and product innovations could enable more comprehensive and transparent pricing, bolstering future ASPU (Average Spend Per User) and revenue growth.

- The ongoing rollout and investment in the 5G network, which is continuing to expand coverage, can enhance Tele2's competitive position and data-driven service offerings, potentially increasing revenue through new service expansion.

- Cost savings from the Strategy Execution Program, including SEK 225 million in annual run rate savings achieved, should positively impact net margins and earnings through improved operational efficiency.

- The movement of customers to more modern technologies (e.g., OTT for TV customers) could stabilize and potentially grow the customer base while lowering operational costs, impacting earnings positively.

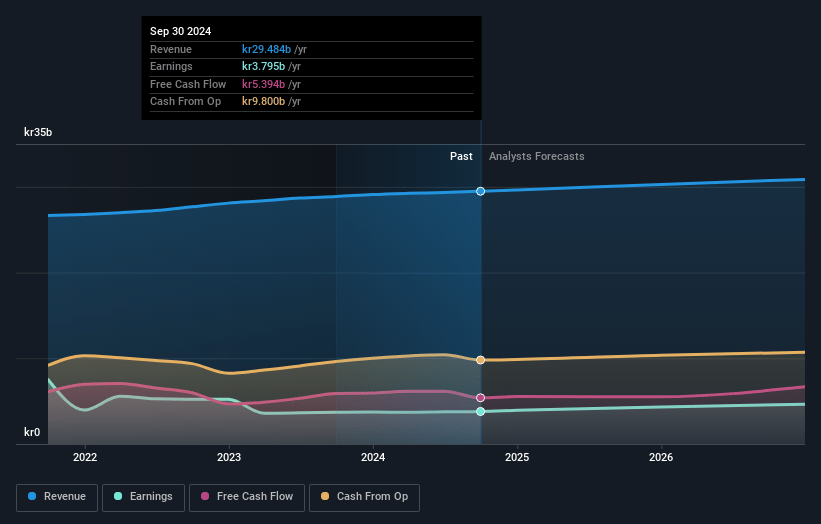

Tele2 Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Tele2's revenue will grow by 2.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 12.9% today to 15.6% in 3 years time.

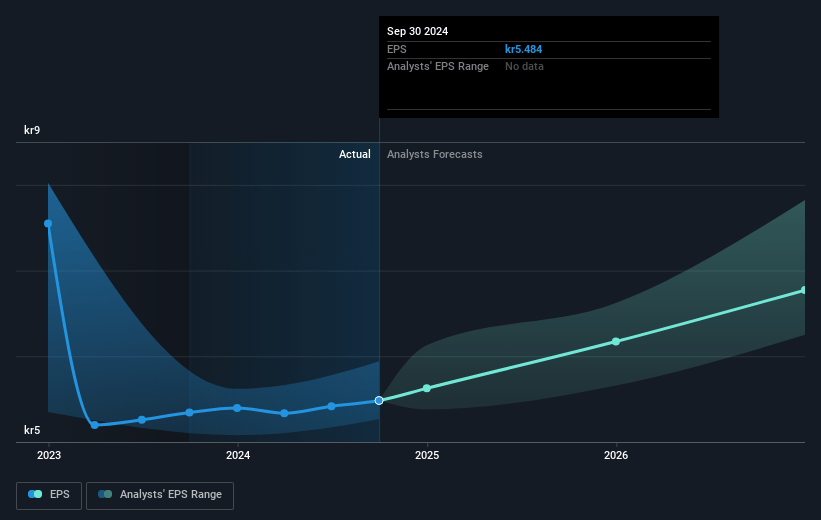

- Analysts expect earnings to reach SEK 4.9 billion (and earnings per share of SEK 7.04) by about January 2028, up from SEK 3.8 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as SEK 4.4 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 18.8x on those 2028 earnings, down from 19.9x today. This future PE is greater than the current PE for the GB Wireless Telecom industry at 18.6x.

- Analysts expect the number of shares outstanding to grow by 0.05% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 4.5%, as per the Simply Wall St company report.

Tele2 Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Economic headwinds in Sweden and the Baltics could impact consumer and business spending, potentially leading to slower revenue growth.

- The ongoing migration of Boxer TV customers from terrestrial to modern TV services may lead to increased churn, which could negatively affect revenue and net margins.

- Higher energy costs and reduced electricity support compared to last year create a cost headwind, potentially affecting net margins and earnings.

- The shift to a handset binding proposition and new pricing strategies have short-term impacts on revenue comparisons due to IFRS 15 treatment, potentially influencing earnings.

- Intense competition in the telecommunications market and the potential slow uptake of fixed mobile convergence (FMC) due to customer inertia may limit revenue growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of SEK 116.23 for Tele2 based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SEK 145.0, and the most bearish reporting a price target of just SEK 93.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be SEK 31.2 billion, earnings will come to SEK 4.9 billion, and it would be trading on a PE ratio of 18.8x, assuming you use a discount rate of 4.5%.

- Given the current share price of SEK 109.25, the analyst's price target of SEK 116.23 is 6.0% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives