Key Takeaways

- NaturVet's growth through improved customer relations and visibility, alongside expansion in major sales channels, can drive significant revenue increase and operational scale.

- Strategic local manufacturing and new market acceptance enhance Swedencare's competitiveness, improve cost efficiencies, and boost investor interest, potentially positively impacting net margins and market capitalization.

- Swedencare's revenue faces risks from a major decline in organic growth, competition in branded sales, increased expenses, and heavy reliance on North American markets.

Catalysts

About Swedencare- Develops, manufactures, markets, and sells animal healthcare products for cats, dogs, and horses in Sweden, the United Kingdom, Rest of Europe, North America, Asia, and internationally.

- Swedencare's NaturVet division is expected to return to growth with improvements in customer relationships and increased visibility, which should contribute to reaching double-digit organic growth targets. This is likely to impact revenue positively.

- The acceptance of trade under the ticker SWDCF at OTCQX in New York could expand the company's investor base in North America, potentially driving stock liquidity and shareholder interest, which might help in enhancing the company's market capitalization.

- ProDen PlaqueOff's recent VOHC recognition for its effectiveness against both plaque and tartar is expected to boost its competitiveness, potentially increasing sales in the high-margin dental category. This could positively influence revenue and net margins.

- Expansion into big box retailers and the ongoing focus on strengthening relationships with major branded customers should increase distribution reach and sales channels, expected to boost revenue and operational scale.

- The strategic focus on local manufacturing to mitigate trade and tariff risks aids operational efficiency and cost management, potentially improving net margins due to reduced dependency on international supply chains.

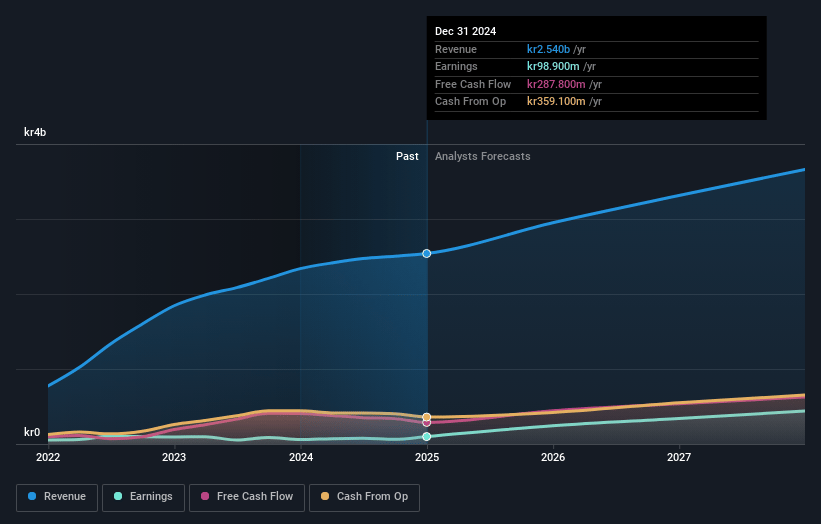

Swedencare Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Swedencare's revenue will grow by 11.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.9% today to 11.9% in 3 years time.

- Analysts expect earnings to reach SEK 418.8 million (and earnings per share of SEK 2.63) by about April 2028, up from SEK 98.9 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 25.0x on those 2028 earnings, down from 60.0x today. This future PE is lower than the current PE for the SE Pharmaceuticals industry at 67.5x.

- Analysts expect the number of shares outstanding to grow by 0.08% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 4.76%, as per the Simply Wall St company report.

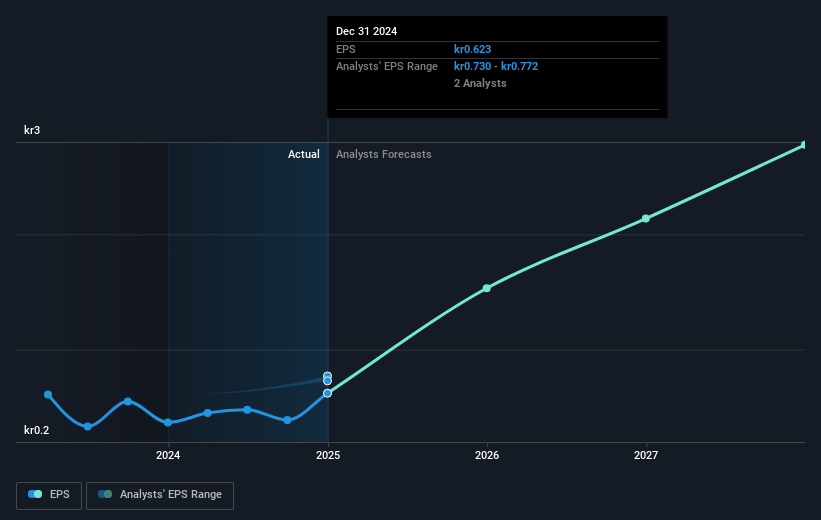

Swedencare Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- NaturVet, Swedencare's biggest group company, experienced a 21% organic growth decline, affecting overall growth and potentially impacting revenue and earnings if not rectified.

- The company faces challenges with its biggest pet specialty customer due to the launch of competing brands, affecting branded sales and potentially limiting revenue growth until 2025.

- Sales growth in North America was only 2% for the quarter, indicating a slowdown in the company's primary market, which could impact overall revenue if this trend continues.

- Additional operating expenses, including a nonoperational legal settlement and rebranding costs, have affected EBITDA margins; if such costs persist, they could restrict net margins.

- Heavy reliance on North American sales, with over 70% of revenue from the region, poses a risk if there are shifts in market dynamics or economic conditions, potentially affecting revenue and earnings stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of SEK57.0 for Swedencare based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be SEK3.5 billion, earnings will come to SEK418.8 million, and it would be trading on a PE ratio of 25.0x, assuming you use a discount rate of 4.8%.

- Given the current share price of SEK37.1, the analyst price target of SEK57.0 is 34.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.