Key Takeaways

- Dependence on ADDA 2025 and Swedish market competition may delay customer decisions and contract, impacting sales and revenue growth.

- Expansion efforts and R&D investments risk increased costs and immediate financial strain without guaranteed immediate revenue offset.

- Successful market expansion and strategic focus on high-potential regions have driven sales growth and improved profitability, with further revenue opportunities in new technologies and markets.

Catalysts

About Careium- Provides technology-enabled care services in Sweden, Norway, the United Kingdom, the Netherlands, Germany, France, and Spain.

- The dependence on a new tender framework (ADDA 2025) in Sweden, which is expected to delay customer decisions and contracts in the first half of 2025, could lead to a temporary decrease in sales and pressure on revenue growth.

- Significant uncertainty remains around the potential impact of upcoming contracts and competition in the Swedish market, creating a risk of further revenue decline in the Nordics if favorable outcomes do not materialize.

- Increased investment in R&D and technology, such as the new i-Care Center, may temporarily inflate costs, which could impact net margins if not offset by corresponding growth in sales and efficiencies.

- Expansion into assisted living and direct-to-consumer markets involves both market uncertainties and significant upfront capital outlays, which may lead to increased operational costs and may not immediately generate revenue.

- Potential acquisitions as part of growth strategy might require significant capital deployment or debt, impacting financial flexibility and perhaps pressure on free cash flow in the short term if integration challenges arise.

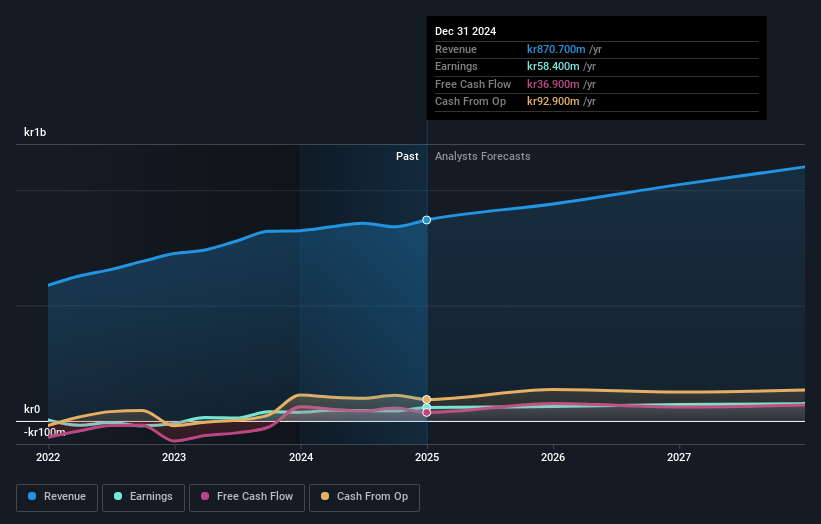

Careium Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Careium's revenue will grow by 8.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 6.7% today to 6.8% in 3 years time.

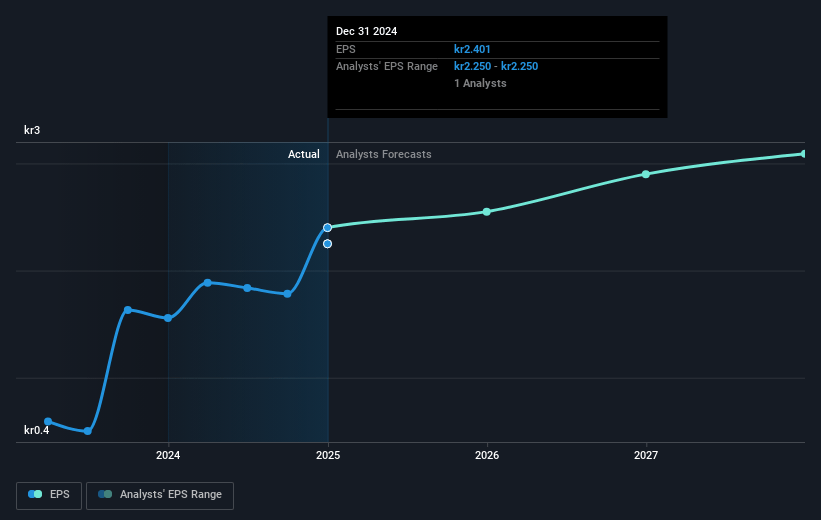

- Analysts expect earnings to reach SEK 75.0 million (and earnings per share of SEK 3.09) by about February 2028, up from SEK 58.4 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 11.6x on those 2028 earnings, down from 14.5x today. This future PE is lower than the current PE for the SE Medical Equipment industry at 31.5x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.86%, as per the Simply Wall St company report.

Careium Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Careium reported strong sales growth in various markets, including the U.K. and the Netherlands, along with improved profitability and gross margins, suggesting robust revenue and earnings potential in these regions.

- The company has successfully implemented strategic shifts to focus on high-potential markets, leading to substantial sales increases in DACH and France, demonstrating potential for continued revenue growth.

- Careium's efforts to expand into new markets such as assisted living may enhance revenue streams, especially through large tenders and B2B relationships.

- Careium's leverage reduction and strong free cash flow indicate financial stability, which could benefit net margins and provide resources for strategic investments.

- The company's focus on developing new technologies and solutions, such as the i-Care Center, may improve efficiency and profit margins through better contract pricing and product mix.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of SEK30.5 for Careium based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be SEK1.1 billion, earnings will come to SEK75.0 million, and it would be trading on a PE ratio of 11.6x, assuming you use a discount rate of 5.9%.

- Given the current share price of SEK34.9, the analyst price target of SEK30.5 is 14.4% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives