Last Update 23 Sep 25

Fair value Decreased 1.52%The consensus price target for AAK AB (publ.) was marginally reduced to SEK308.00 amid a decrease in revenue growth forecasts and a slight drop in future P/E, indicating tempered expectations for the company’s near-term performance.

Valuation Changes

Summary of Valuation Changes for AAK AB (publ.)

- The Consensus Analyst Price Target remained effectively unchanged, moving only marginally from SEK312.75 to SEK308.00.

- The Consensus Revenue Growth forecasts for AAK AB (publ.) has significantly fallen from 1.1% per annum to 1.0% per annum.

- The Future P/E for AAK AB (publ.) has fallen slightly from 20.48x to 19.57x.

Key Takeaways

- Growing demand for sustainable, health-focused foods and stricter supply chain regulations strengthen AAK's market position, enabling premiumization and customer loyalty.

- Operational efficiency programs and innovation investments drive higher margins and earnings resilience, supported by strategic diversification across stable and expanding markets.

- Structural volume declines, continued margin pressure, and sustainability risks threaten long-term growth, despite internal optimization and cost-saving investments.

Catalysts

About AAK AB (publ.)- Develops and sells plant-based oils and fats in Sweden and internationally.

- Ongoing shifts toward plant-based diets and heightened consumer demand for health-conscious, sustainable, and traceable food products position AAK's specialty oils portfolio to benefit from accelerating long-term reformulation efforts and premiumization, supporting resilient revenue growth and robust margin expansion over the coming years.

- Intensifying global sustainability and ESG focus, along with stricter regulations and customer requirements on supply chain traceability, provide a catalyst for AAK's responsibly sourced and ESG-compliant offerings-bolstered by transparency initiatives like their PAI report and new leadership in Sourcing, Trading, and Sustainability-helping secure sticky, long-term customer partnerships and protecting pricing power (net margin resilience).

- The company's operational optimization programs-including deep dives, production process enhancements, procurement excellence, and the "Fit-to-Win" cost performance initiative-are expected to structurally increase efficiency and deliver SEK 300m in annualized cost savings by mid-2026, with incremental earnings and EBITDA margin improvement as additional program benefits are realized.

- Investments in commercial and innovation excellence, including a unified global CRM and more tailored customer solutions, aim to accelerate the pace of value-added product launches and customer engagement, potentially restarting volume growth and shifting mix toward higher-margin, specialty applications that support gross margin and long-term earnings potential.

- AAK's diversification across resilient end-markets (dairy, plant-based, infant nutrition, technical products, etc.), combined with ongoing strategic M&A and capacity investments in high-growth regions such as Latin America, build in multi-channel growth optionality-helping to stabilize revenue and earnings even amid temporary softness in specific segments like Bakery or Confectionery.

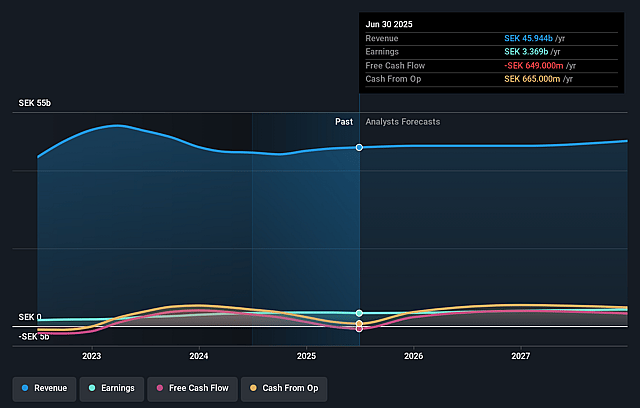

AAK AB (publ.) Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming AAK AB (publ.)'s revenue will grow by 1.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.3% today to 9.6% in 3 years time.

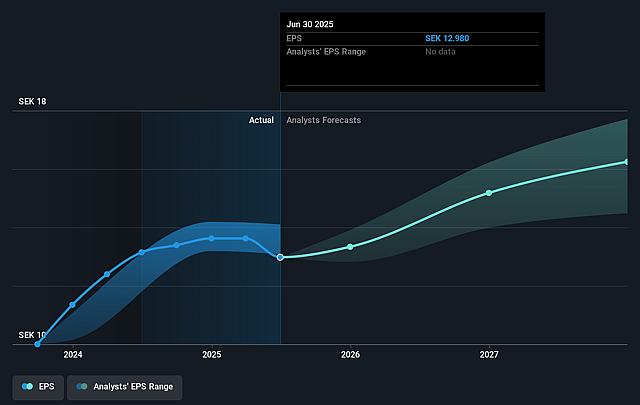

- Analysts expect earnings to reach SEK 4.6 billion (and earnings per share of SEK 16.25) by about September 2028, up from SEK 3.4 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as SEK3.8 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 20.5x on those 2028 earnings, up from 20.3x today. This future PE is lower than the current PE for the GB Food industry at 21.8x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 4.92%, as per the Simply Wall St company report.

AAK AB (publ.) Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Sustained volume declines across key segments-especially in Bakery and Chocolate & Confectionery Fats-suggest headwinds from both soft end-market demand and AAK's shift away from lower-margin contracts; if underlying global consumption of processed food ingredients continues to weaken due to long-term health trends or changing consumer preferences, revenue growth may be structurally impaired.

- Although the company is achieving operating profit growth through internal optimization and margin improvements, these gains may not be sustainable if the volume base continues to erode, or if competition intensifies, thereby putting pressure on future revenue and margin progression.

- AAK's continued reliance on commodity oils such as palm entails exposure to price volatility, regulatory interventions, and reputational risks related to sustainability-any tightening of ESG or deforestation regulations could increase compliance costs, disrupt supply chains, and compress gross margins.

- Ongoing investments in process optimization, restructuring (such as the Fit-to-Win program), digitization, and sustainability are generating cost savings, but also require significant upfront restructuring charges and capital expenditures; if the expected productivity gains do not materialize or market conditions worsen, net margins and earnings could be negatively affected.

- Management's own comments about active portfolio selection-walking away from some contracts due to pricing-indicate ongoing pricing pressure and a highly competitive market; this strategy, while protecting margins short-term, may lead to reduced market share and top-line stagnation or decline if competitors become more aggressive or if AAK's innovation pipeline does not produce sufficient high-value differentiated solutions to offset these losses, ultimately impacting revenue and long-term earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of SEK312.75 for AAK AB (publ.) based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SEK380.0, and the most bearish reporting a price target of just SEK245.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be SEK47.5 billion, earnings will come to SEK4.6 billion, and it would be trading on a PE ratio of 20.5x, assuming you use a discount rate of 4.9%.

- Given the current share price of SEK263.2, the analyst price target of SEK312.75 is 15.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.