Key Takeaways

- Marginal risk reduction from the banking package could maintain high capital levels, potentially suppressing return on equity growth.

- High dividend payouts might limit growth reinvestment, suppressing long-term earnings and impacting shareholder returns.

- Strong profitability, capital management, and customer satisfaction highlight potential resilience and growth, with effective credit risk and asset management suggesting stable earnings and revenue growth.

Catalysts

About Svenska Handelsbanken- Provides various banking products and services for private and corporate customers primarily in Sweden, the United Kingdom, Norway, the Netherlands, the United States, Luxembourg, Finland, and Poland.

- The anticipated introduction of the banking package is expected to have a marginal reduction in risk exposure, potentially maintaining high capital levels that could suppress return on equity (ROE) growth.

- Mutual fund market share is growing, but at a slower pace than net inflows, indicating a potential plateau in revenue growth if the trend continues without sufficient performance improvement to capture a larger share of the market.

- Operational efficiency measures in business support and group functions have shown short-term expense reductions, but if not sustained, could result in future margin pressures with increased costs impacting earnings.

- Heavy focus on asset quality with limited risk appetite may limit exposure to higher-yielding opportunities, potentially constraining revenue and earnings growth despite the low credit loss experience.

- High anticipated dividend payout ratio (over 100% of Q3 earnings) could reduce reinvestment in growth opportunities and suppress long-term earnings potential, impacting shareholder returns.

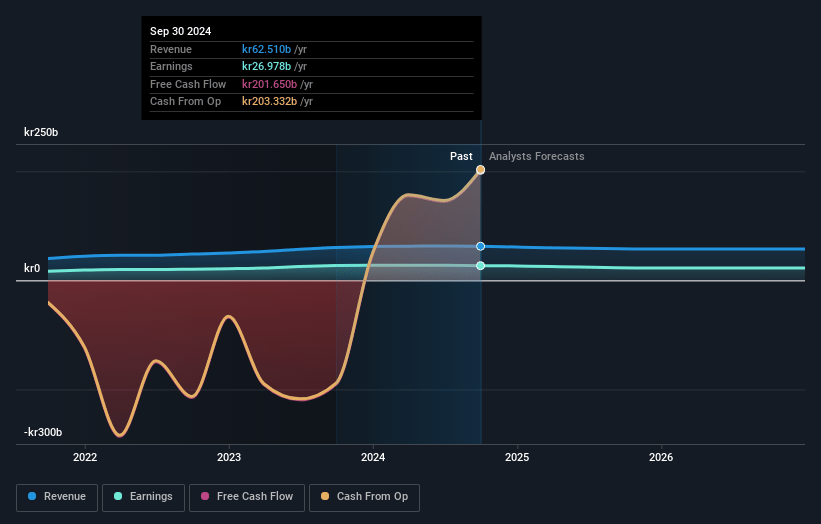

Svenska Handelsbanken Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Svenska Handelsbanken's revenue will decrease by -0.9% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 43.2% today to 39.8% in 3 years time.

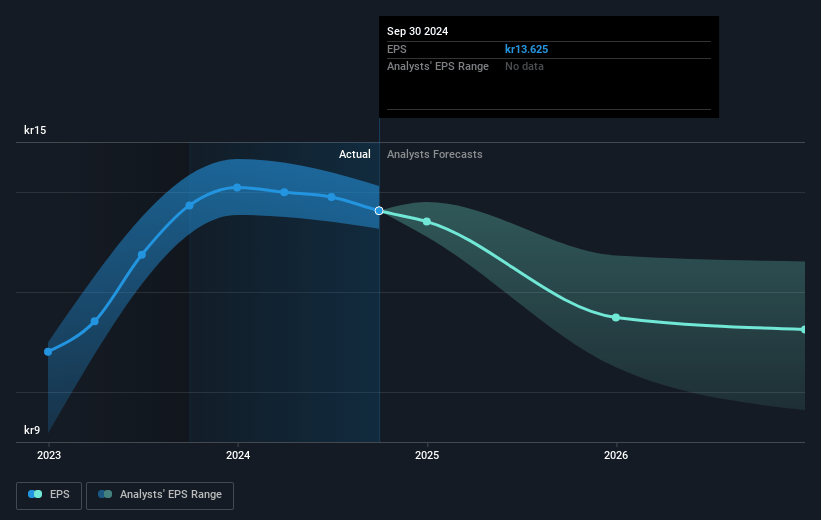

- Analysts expect earnings to reach SEK 24.2 billion (and earnings per share of SEK 12.74) by about January 2028, down from SEK 27.0 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as SEK19.1 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 11.9x on those 2028 earnings, up from 9.1x today. This future PE is greater than the current PE for the GB Banks industry at 9.1x.

- Analysts expect the number of shares outstanding to decline by 1.3% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.44%, as per the Simply Wall St company report.

Svenska Handelsbanken Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Handelsbanken has reported significant profitability improvements, with an increase in ROE and a reduction in cost-to-income ratios. This financial strength suggests potential resilience and growth prospects in revenue and earnings.

- The bank's strong capital position, with a CET1 ratio well above regulatory requirements, and the potential to deliver high dividend payouts indicate good capital management and potential for sustained earnings distribution.

- Customer satisfaction remains high, evidenced by awards and recognition, which could translate into customer retention and growth, potentially improving revenue and net margins.

- The bank's successful growth in assets under management, driven by strong customer relationships and increased advisory activities, indicates potential for sustained revenue growth from fee and commission income.

- The neutral impact of regulatory changes and the bank's effective credit risk management, with minimal credit losses historically, suggest stability in asset quality and positive implications for net margins and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of SEK116.0 for Svenska Handelsbanken based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SEK147.0, and the most bearish reporting a price target of just SEK95.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be SEK60.9 billion, earnings will come to SEK24.2 billion, and it would be trading on a PE ratio of 11.9x, assuming you use a discount rate of 9.4%.

- Given the current share price of SEK124.35, the analyst's price target of SEK116.0 is 7.2% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives