Key Takeaways

- Ambitious global expansion and acquisitions pose risks of financial strain and integration challenges, affecting revenue and financial stability if synergy expectations are unmet.

- Major expansion projects and international ventures involve high capital investments and execution risks, potentially impacting earnings, cash flows, and net margins.

- Strategic investments in exploration and operational efficiency are expected to enhance growth, profit margins, and long-term earnings.

Catalysts

About Saudi Arabian Mining Company (Ma'aden)- Operates as a mining and metals company in the Kingdom of Saudi Arabia, Indian Subcontinent, Japan, the United States, Europe, Australia, Brazil, Africa, GCC, and internationally.

- The ambition to become a global leader in aluminum through strategic acquisitions, including full control of Ma'aden Aluminum assets and stakes in ALBA, is based on significant future expenditure and integration challenges, potentially straining revenue growth and impacting financial stability if synergies are not realized as expected.

- The major expansion projects, such as Phosphate 3 Phase 1 and planned expansions in aluminum capacity, require substantial capital investment and face execution risks, which could lead to cost overruns or delays, directly impacting earnings and cash flows.

- Ma'aden's commitment to expanding internationally and acquiring significant shares in ventures like Vale Base Metals comes with geopolitical and operational risks that could disrupt revenue streams or increase costs, thereby affecting net margins and earnings sustainability.

- The extensive mineral exploration program and technological transformation initiatives represent significant upfront expenditures with uncertain returns, which might pressure operating cash flow and net profit margins if anticipated market conditions do not materialize.

- The ongoing maintenance and production challenges, such as the ones faced at the Sukhaybarat mine, highlight potential risks of operational disruptions that could affect output levels and commodity prices, leading to volatility in revenue and profitability forecasts.

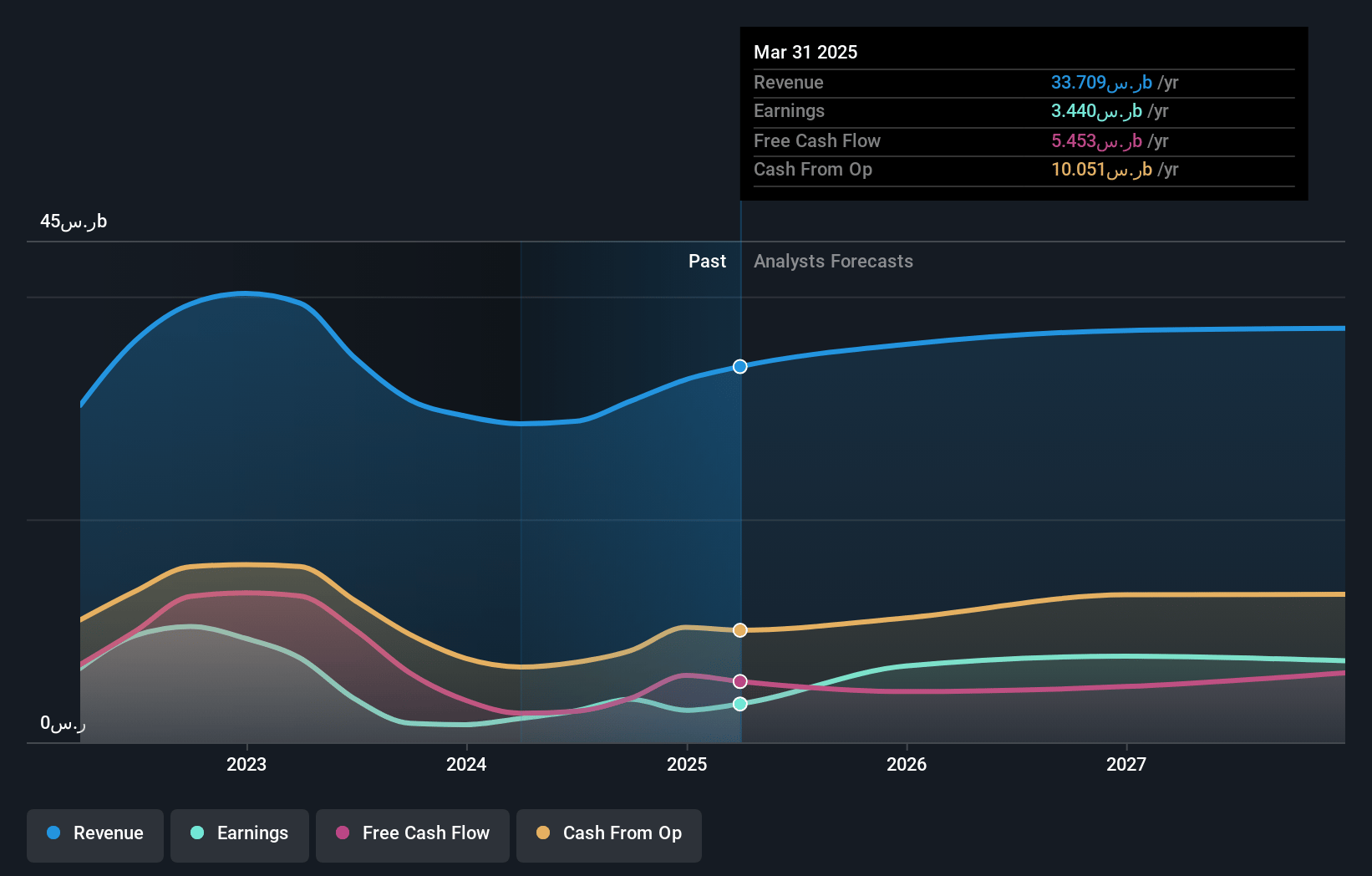

Saudi Arabian Mining Company (Ma'aden) Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Saudi Arabian Mining Company (Ma'aden)'s revenue will grow by 7.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 12.6% today to 20.5% in 3 years time.

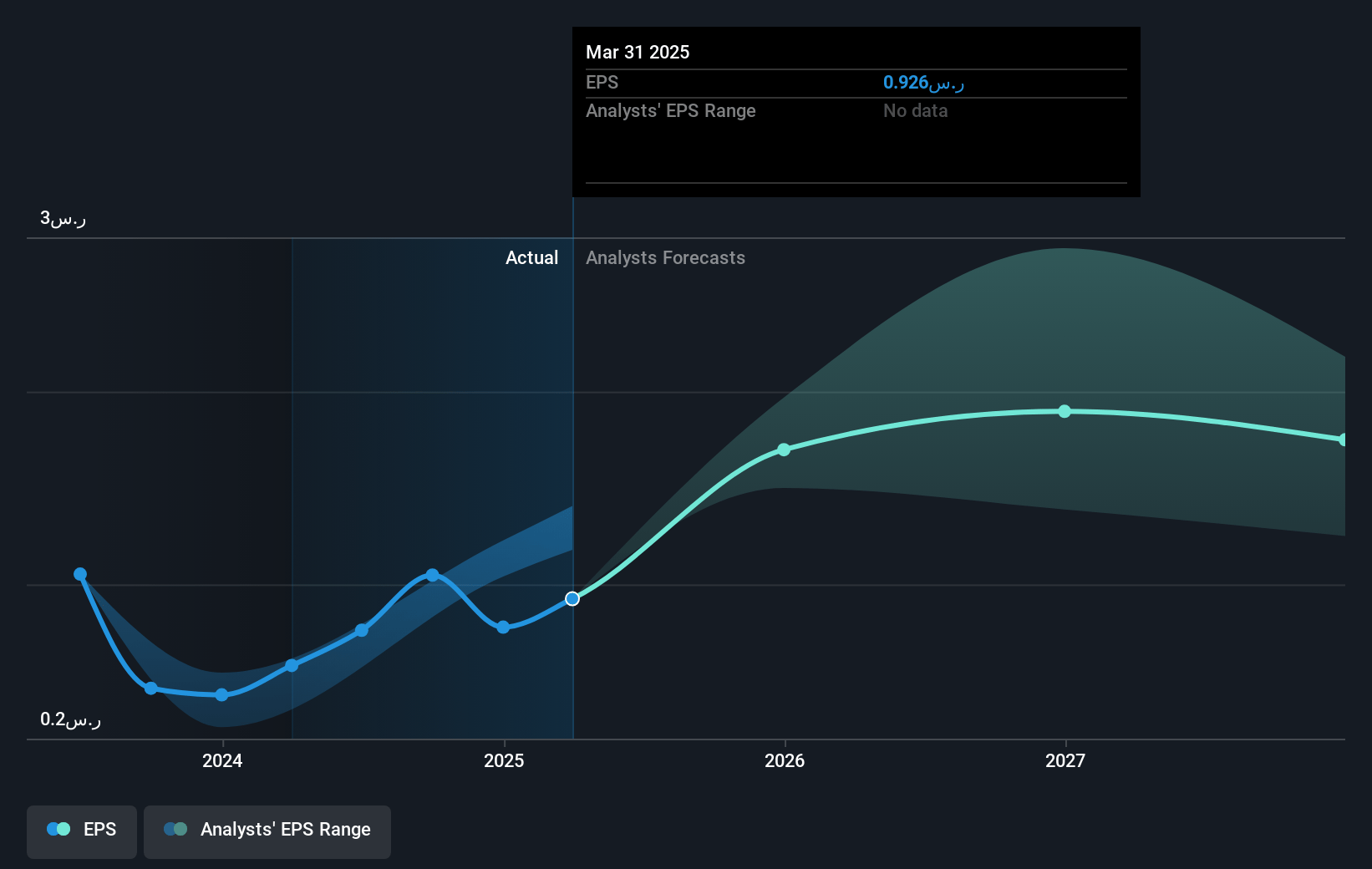

- Analysts expect earnings to reach SAR 7.8 billion (and earnings per share of SAR 2.0) by about December 2027, up from SAR 3.9 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as SAR 6.3 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 39.8x on those 2027 earnings, down from 51.5x today. This future PE is greater than the current PE for the SA Metals and Mining industry at 18.2x.

- Analysts expect the number of shares outstanding to grow by 1.93% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 20.63%, as per the Simply Wall St company report.

Saudi Arabian Mining Company (Ma'aden) Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Ma'aden achieved near-record production and sales volume for DAP and record gold production, indicating strong operational performance across its business segments, which could support higher revenue.

- The company delivered the second highest 9-month EBITDA on record, accompanied by a significant increase in net profit and operating cash flow, suggesting a strong and improving financial position that could enhance earnings.

- Ma'aden is executing strategic transactions in its aluminum business, such as gaining full operational control and acquiring key assets, which are expected to create a competitive aluminum platform and drive sustainable growth, potentially improving net margins.

- The significant exploration efforts and strategic investments in mineral exploration, with a focus on expanding production capacities for critical minerals, are likely to bolster future revenue streams and support long-term earnings growth.

- Ma'aden's strategic focus on technology-enabled mining and operational efficiency improvements is set to lower production costs and potentially improve profit margins in the future.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of SAR 45.37 for Saudi Arabian Mining Company (Ma'aden) based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SAR 60.0, and the most bearish reporting a price target of just SAR 30.5.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be SAR 38.0 billion, earnings will come to SAR 7.8 billion, and it would be trading on a PE ratio of 39.8x, assuming you use a discount rate of 20.6%.

- Given the current share price of SAR 54.0, the analyst's price target of SAR 45.37 is 19.0% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives