Key Takeaways

- Strategic focus on data center expansion and fintech could drive revenue growth, enhance operational efficiency, and improve net profit margins.

- Strong financial flexibility from bond issuance and leveraging emerging markets may support strategic investments and boost future earnings.

- Competitive pressures in Qatar and Oman, debt concerns, and delayed strategic initiatives pose risks to revenue growth, profitability, and cash flow.

Catalysts

About Ooredoo Q.P.S.C- Provides telecommunications services in Qatar, Asia, rest of the Middle East, and North Africa region.

- Ooredoo's strategic focus on data center expansion, supported by a QAR 2 billion financing deal and collaboration with NVIDIA, positions the company as a leader in AI and digital infrastructure in the MENA region. This is expected to drive future growth in revenue and profitability as demand for AI and cloud services increases.

- The completion of the data center carve-out in markets like Qatar, Tunisia, and Kuwait, with others expected by 2025, indicates a streamlined and focused strategy that could enhance operational efficiency and positively impact EBITDA margins and net earnings.

- Expansion efforts in fintech, including obtaining new licenses in Oman and the Maldives, as well as pursuing licenses in Tunisia, Iraq, and Kuwait, could open additional revenue streams and improve net profit margins as digital financial services gain traction.

- Successful international bond issuance, coupled with a stable financial position featuring strong liquidity and conservative leverage, enhance Ooredoo's financial flexibility, which could support strategic investments and potentially increase earnings per share (EPS) through judicious capital allocation and debt management.

- Continued growth in emerging markets such as Iraq and Algeria, demonstrated by double-digit increases in revenue and EBITDA, provides a robust foundation for future revenue growth, potentially offsetting pressures in more mature markets and leading to overall improvement in the group's earnings trajectory.

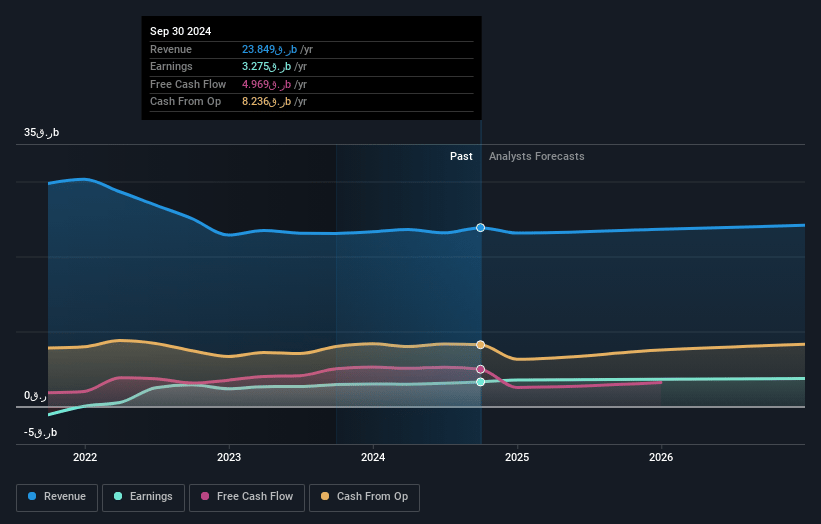

Ooredoo Q.P.S.C Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Ooredoo Q.P.S.C's revenue will decrease by 0.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 13.7% today to 16.3% in 3 years time.

- Analysts expect earnings to reach QAR 4.0 billion (and earnings per share of QAR 1.23) by about January 2028, up from QAR 3.3 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as QAR3.6 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 19.1x on those 2028 earnings, up from 12.6x today. This future PE is greater than the current PE for the QA Telecom industry at 12.6x.

- Analysts expect the number of shares outstanding to grow by 0.56% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 18.51%, as per the Simply Wall St company report.

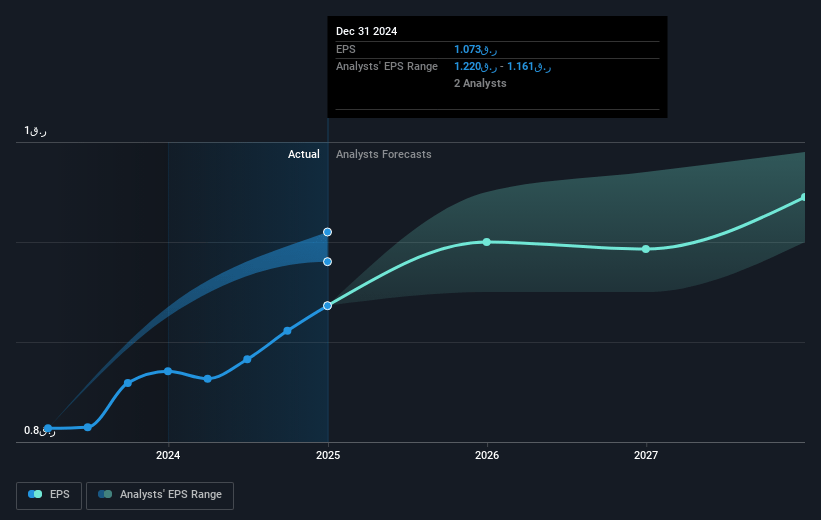

Ooredoo Q.P.S.C Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The highly competitive market environment in Qatar and Oman has impacted top-line performance, with decreases in revenue reported, suggesting challenges in sustaining revenue growth.

- The revenue decline in Oman due to high competition and Kuwait's EBITDA reduction from one-off bad debt provisions indicate potential risks to profitability and net margins in these regions.

- The anticipated capital expenditure increase, particularly for network rollouts and infrastructure improvements, could pressure free cash flow and may not immediately translate into higher earnings.

- The company's significant debt financing and bond issuance, although strategic, could elevate financial risk and potentially affect net margins if revenue and profitability targets are not met.

- Regulatory approvals and market conditions could delay strategic initiatives like tower and data center carve-outs, affecting anticipated revenue growth and operational efficiency.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of QAR14.1 for Ooredoo Q.P.S.C based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be QAR24.5 billion, earnings will come to QAR4.0 billion, and it would be trading on a PE ratio of 19.1x, assuming you use a discount rate of 18.5%.

- Given the current share price of QAR12.83, the analyst's price target of QAR14.1 is 9.0% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives