Key Takeaways

- Execution of renewable projects and recycling focus positions Hydro for revenue growth by diversifying energy sources and capturing premium markets.

- Cost savings from fuel switches and operational improvements bolster net margins, enhancing earnings even during market downturns.

- Economic challenges and market pressures, especially in key sectors, could negatively impact Norsk Hydro's revenue, margins, and long-term strategic initiatives.

Catalysts

About Norsk Hydro- Engages in the power production, bauxite extraction, alumina refining, aluminium smelting, and recycling activities; and provision of extruded solutions worldwide.

- The execution of Hydro's renewable ambitions, such as the Illvatn pumped storage project and heightened investment in renewable energy generation, is expected to enhance revenue by diversifying energy sources and minimizing energy costs.

- Significant cost savings and profit increase are anticipated from the completion of the Alunorte fuel switch, which is projected to save $160 million to $190 million annually, positively impacting net margins by reducing fuel costs and CO2 emissions.

- Hydro's focus on recycling and developing sustainable products, like Hydro CIRCAL, positions the company to capture premium market opportunities and drive revenue growth from the increasing demand for greener aluminum solutions.

- Operational improvements in upstream aluminum metal procurement and extrusion processes, along with cost-cutting efforts during market downturns, are set to bolster net margins and enhance earnings even in challenging markets.

- Strategic partnerships, such as the collaboration with Mercedes-Benz on sustainable development, are likely to drive long-term growth and revenue by increasing demand for low-carbon aluminum and expanding market reach in sustainable applications.

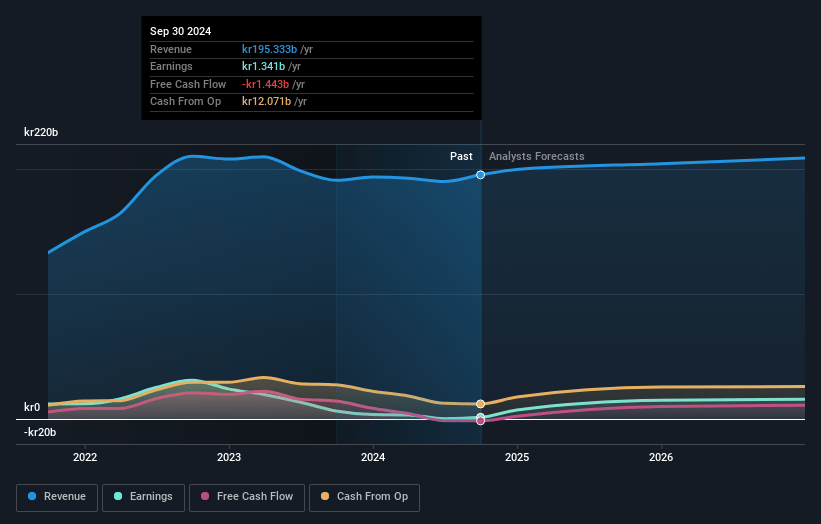

Norsk Hydro Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Norsk Hydro's revenue will grow by 4.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 0.7% today to 8.9% in 3 years time.

- Analysts expect earnings to reach NOK 19.8 billion (and earnings per share of NOK 10.04) by about January 2028, up from NOK 1.3 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 10.0x on those 2028 earnings, down from 97.8x today. This future PE is lower than the current PE for the GB Metals and Mining industry at 50.9x.

- Analysts expect the number of shares outstanding to decline by 0.1% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.44%, as per the Simply Wall St company report.

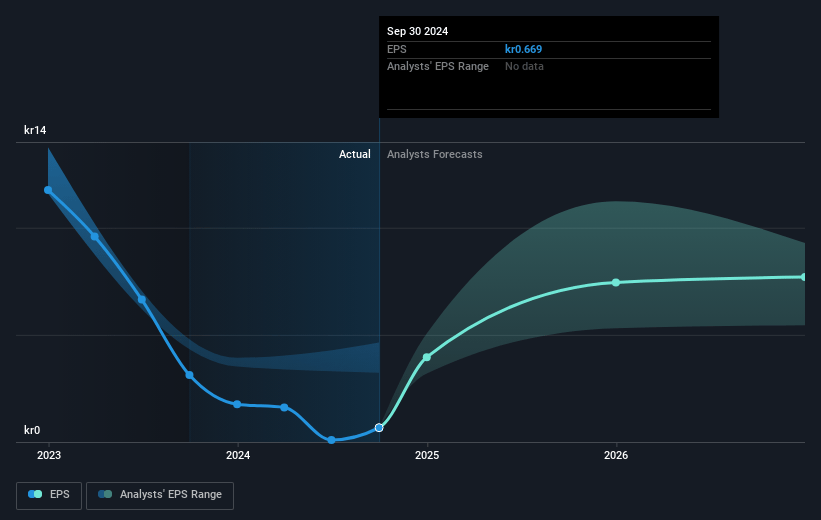

Norsk Hydro Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The pressure on downstream activities, particularly extrusions, due to weaker core markets in Europe and North America may continue to negatively impact revenue and net margins.

- The current market downturn and high scrap prices are putting a significant strain on recycling margins, which are at an all-time low, potentially affecting future profitability and earnings.

- The company's decision to reduce ownership in Vianode and the associated NOK 1 billion impairment indicates a more challenging market for battery materials, which could impact future earnings and strategic growth initiatives.

- Tightness in the global alumina market due to supply disruptions and increasing costs could adversely affect the company's raw material expenses, thereby decreasing net margins and impacting earnings.

- Economic slowdown, particularly impacting the building, construction, and automotive sectors, may lead to continued low extrusion demands and higher raw material costs, which could undermine revenue growth and profit margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of NOK80.67 for Norsk Hydro based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of NOK100.0, and the most bearish reporting a price target of just NOK55.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be NOK221.8 billion, earnings will come to NOK19.8 billion, and it would be trading on a PE ratio of 10.0x, assuming you use a discount rate of 7.4%.

- Given the current share price of NOK66.38, the analyst's price target of NOK80.67 is 17.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives