Last Update 24 Apr 25

Fair value Increased 1.77%Key Takeaways

- Kingfish's shift to larger-sized fish and production efficiency improvements are likely to enhance net margins and profitability.

- Financial strengthening via equity raise supports expansion, potentially leading to higher future revenues and earnings.

- Operational challenges, cost issues, overproduction, U.S. tariff risks, and legal delays threaten Kingfish's efficiency, growth, and profitability in key markets.

Catalysts

About Kingfish- Produces and sells seafood products in Western Europe, Southern Europe, and internationally.

- Kingfish demonstrated a 60% increase in sales volume in Q4 and surpassed 2,000 tonnes of shipped volume for the year, indicating strong commercial traction that could significantly boost revenues in 2025 as they scale to full capacity.

- The company is focusing on selling larger-sized fish, which commands higher margins, and expects increased demand in this segment. This shift towards high-value segments is likely to improve net margins and profitability.

- Scaling operations to full capacity, which they expect to achieve quickly, will allow Kingfish to leverage its fixed cost base more effectively, improving operating leverage and increasing earnings.

- Continued improvements in production efficiency, including optimizing biomass levels and benefiting from lower feed costs, are expected to enhance operational efficiency and boost net margins.

- The completion of a €40 million equity raise strengthens the financial position, supporting Kingfish’s strategy to accelerate sales and expand production capacity, which could lead to higher revenues and potentially improved earnings.

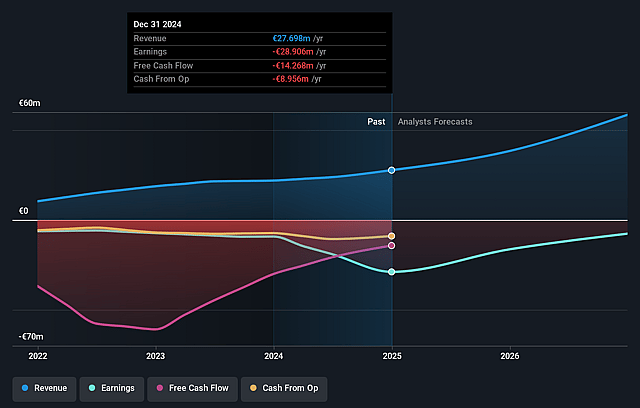

Kingfish Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Kingfish's revenue will grow by 36.9% annually over the next 3 years.

- Analysts are not forecasting that Kingfish will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Kingfish's profit margin will increase from -104.4% to the average NO Food industry of 11.6% in 3 years.

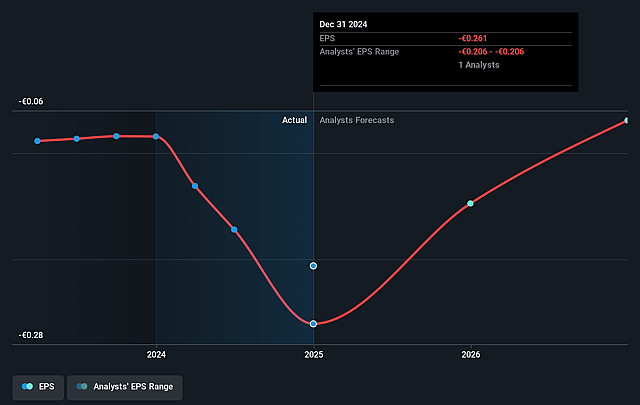

- If Kingfish's profit margin were to converge on the industry average, you could expect earnings to reach €8.2 million (and earnings per share of €0.06) by about April 2028, up from €-28.9 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 10.2x on those 2028 earnings, up from -2.5x today. This future PE is lower than the current PE for the NO Food industry at 21.1x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.56%, as per the Simply Wall St company report.

Kingfish Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company experienced IT problems during important meetings which could indicate systemic operational challenges that might affect overall efficiency and promptness, potentially impacting future revenues and investor confidence.

- Despite significant growth, the company faced higher than targeted production costs and a decline in EBITDA, both suggesting potential difficulties in achieving desired net margins and positive earnings.

- Overproduction issues led to a biomass reduction plan, which caused a €1.2 million reduction in biomass value, indicating potential inefficiencies that could affect revenue generation if not managed carefully.

- The U.S. market, representing 15% of sales volume, faces potential tariff risks that could hinder growth and revenue opportunities in an important market segment.

- There are ongoing legal proceedings regarding the U.S. expansion, which have already led to delays and could affect long-term expansion plans and associated revenue and profitability projections.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of NOK5.793 for Kingfish based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €71.0 million, earnings will come to €8.2 million, and it would be trading on a PE ratio of 10.2x, assuming you use a discount rate of 6.6%.

- Given the current share price of NOK6.0, the analyst price target of NOK5.79 is 3.6% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Kingfish?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.