Key Takeaways

- Limited new tanker supply and rising demand support higher rates and margins, while Hafnia’s modern fleet enables strong growth and resilience.

- Investments in eco-efficient vessels, new ventures, and disciplined capital allocation enhance earnings stability, margins, and future profitability.

- Shifting energy policies, fleet challenges, sector consolidation, and regulatory risks threaten Hafnia’s long-term demand, market position, operating costs, and overall profitability.

Catalysts

About Hafnia- Owns and operates oil product tankers in Bermuda.

- Persistent constraints in new tanker construction, compounded by shipyard backlogs and stricter environmental requirements, are limiting global fleet additions at a time when global demand and trade volumes for refined products continue to rise. This supply-demand imbalance is likely to support higher charter rates and asset values for owners like Hafnia, benefiting both revenue growth and net margins.

- Shifting refinery locations, ongoing regional imbalances, and increased global trading distances for refined products are driving long-term growth in tonne-miles. Hafnia’s large, modern, and geographically diversified fleet is well positioned to capture this sustained high utilization, supporting robust top-line growth and earnings resilience.

- Fleet renewal and ongoing investment in dual-fuel and eco-efficient vessels are enabling Hafnia to offer lower-emission, future-proof shipping options as environmental regulations accelerate, attracting premium charter rates and lowering operating costs, which should directly impact operating margins and future profitability.

- Strategic expansion into adjacent businesses—such as the launch of Seascale Energy (a joint venture with Cargill) in bunker procurement—diversifies and grows Hafnia’s fee-based revenue streams, improving earnings stability and margin quality.

- Continued disciplined capital allocation via high dividend payouts, opportunistic share buybacks, and strong balance sheet management not only enhances shareholder returns but also increases the company’s ability to invest in growth and fleet modernization, ultimately supporting sustainable growth in earnings per share.

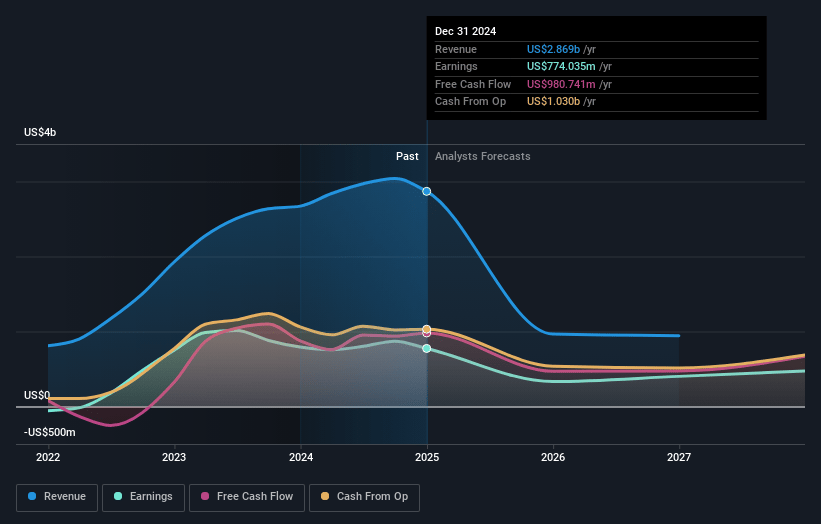

Hafnia Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Hafnia's revenue will decrease by 38.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 25.5% today to 58.3% in 3 years time.

- Analysts expect earnings to reach $326.6 million (and earnings per share of $0.87) by about May 2028, down from $617.7 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 10.5x on those 2028 earnings, up from 4.3x today. This future PE is greater than the current PE for the NO Oil and Gas industry at 4.8x.

- Analysts expect the number of shares outstanding to decline by 4.52% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.42%, as per the Simply Wall St company report.

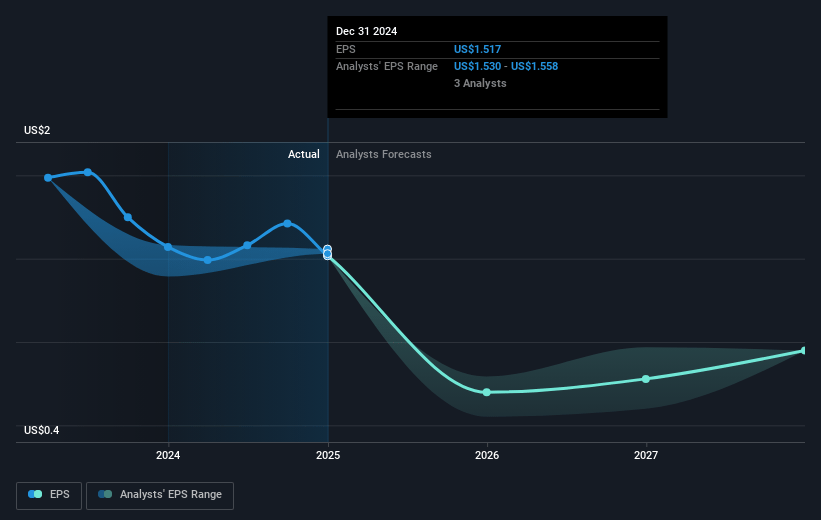

Hafnia Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Accelerating global decarbonization and energy transition policies may reduce long-term demand for oil and petroleum products, which could shrink the addressable market for product tanker operators like Hafnia and put sustained pressure on revenue growth.

- The increasing adoption of electric vehicles and expansion of renewable energy—combined with tightening international emissions regulations—could erode gasoline and diesel consumption, lower product tanker demand, and lead to declining vessel utilization rates and net margins for Hafnia over time.

- An aging fleet profile and a period of limited fleet renewal activity (with a focus on harvesting returns and divesting older vessels rather than acquiring new, more efficient ships) could result in higher maintenance costs, more frequent dry dockings, and increased off-hire days, ultimately putting pressure on operating costs, margins, and free cash flow.

- Heightened sector consolidation and the emergence of larger, diversified shipping groups may create increased competition and cost advantages at scale, putting pressure on Hafnia’s market share, procurement power, and ability to maintain competitive earnings and margins in a tightening market.

- Geopolitical volatility, regulatory uncertainty (such as the potential implementation of new port fees on Chinese-built vessels), and market sentiment-driven rate fluctuations create risks of prolonged rate downturns, higher compliance costs, and vessel value declines, which could materially impact Hafnia’s revenues, asset values, and overall profitability in the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of NOK68.167 for Hafnia based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of NOK77.0, and the most bearish reporting a price target of just NOK62.5.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $559.9 million, earnings will come to $326.6 million, and it would be trading on a PE ratio of 10.5x, assuming you use a discount rate of 6.4%.

- Given the current share price of NOK55.62, the analyst price target of NOK68.17 is 18.4% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.