Key Takeaways

- Strong demand for GAA technology and high-bandwidth memory could significantly increase market share and stabilize future revenue streams.

- Expansion in molybdenum applications and rising new orders may boost sales and earnings despite increased R&D expenses.

- Revenue growth is stabilizing in mature segments while sales in key markets are down, and increased R&D and regulatory uncertainties could pressure profitability.

Catalysts

About ASM International- Engages in the research, development, manufacture, marketing, and servicing of equipment and materials used to produce semiconductor devices in Europe, the United States, and Asia.

- Strong demand for gate-all-around (GAA) technology in 2-nanometer nodes, driven by data center growth and AI demands, is expected to increase market share and sales in ALD, positively impacting future revenues.

- Expansion of molybdenum applications in ALD for metalization, replacing tungsten and copper, enters high-volume production, which could significantly boost sales and earnings by increasing TAM (Total Addressable Market).

- Sustained high-bandwidth memory (HBM) demand linked with the 2-nanometer node ramp could result in robust DRAM sales, hence stabilizing and potentially increasing future revenue streams.

- Ongoing development projects transitioning to commercial release are raising R&D expenses, indicating future revenue-generating potential from these new technologies, potentially bolstering earnings.

- New orders increasing by 30% year-on-year indicate strong customer demand and future revenue growth, which may positively influence future earnings amid mixed market conditions.

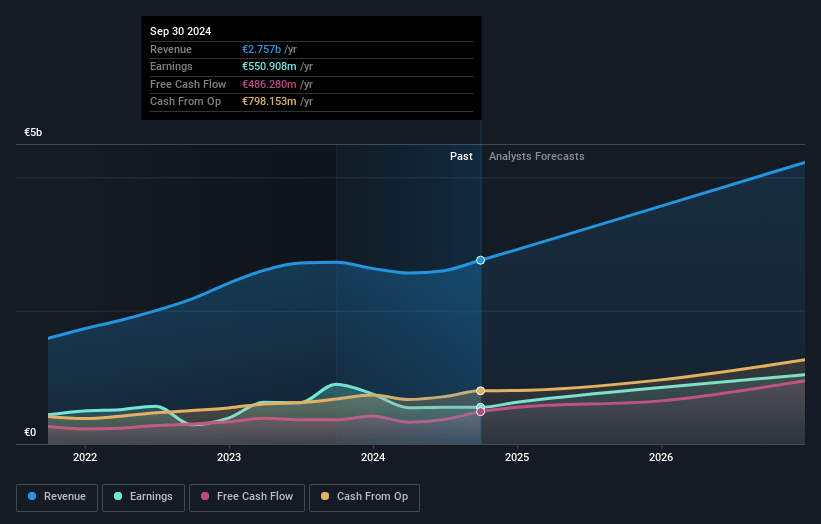

ASM International Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming ASM International's revenue will grow by 18.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 20.0% today to 25.0% in 3 years time.

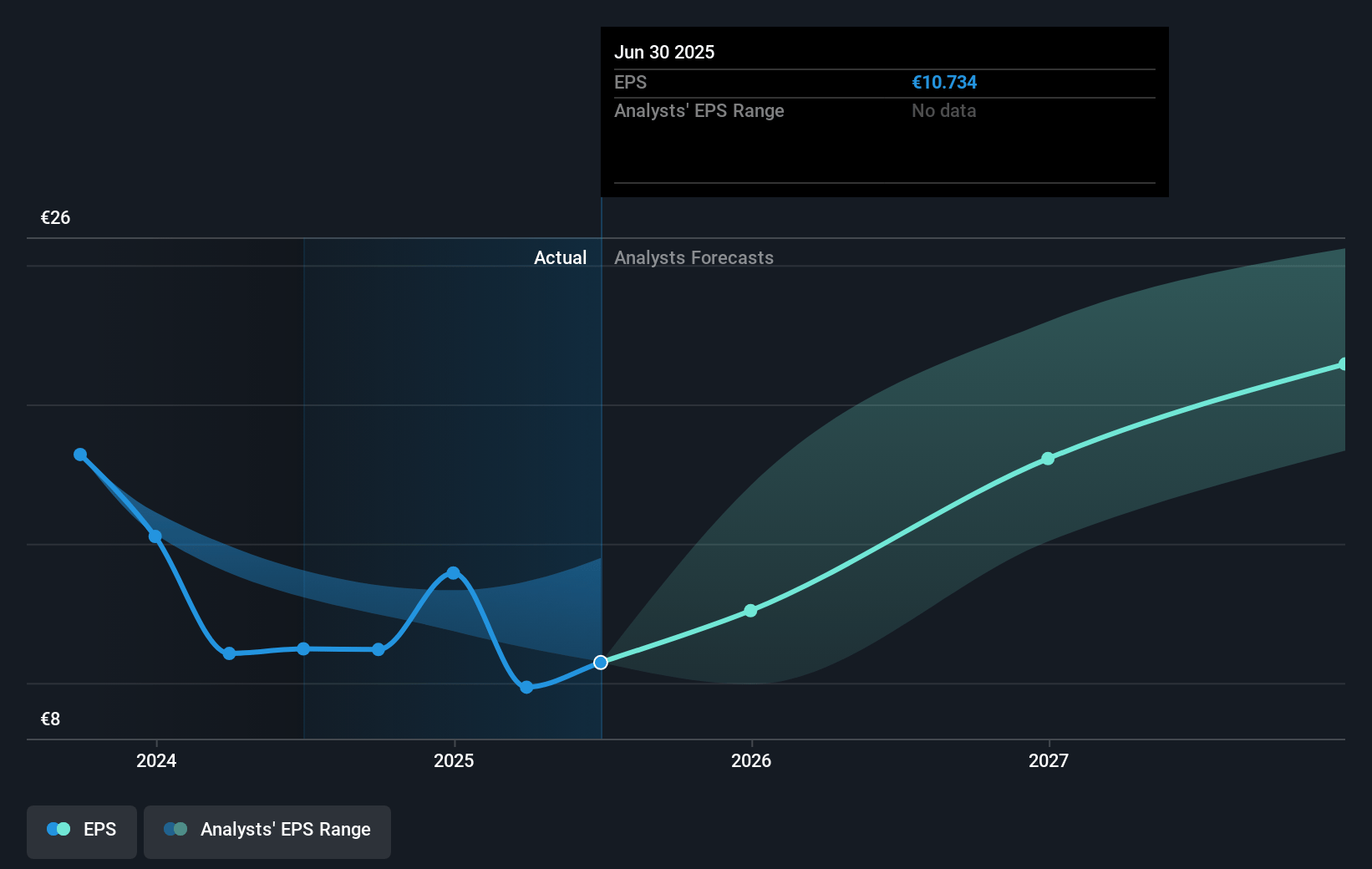

- Analysts expect earnings to reach €1.1 billion (and earnings per share of €22.62) by about January 2028, up from €550.9 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 36.0x on those 2028 earnings, down from 47.2x today. This future PE is lower than the current PE for the GB Semiconductor industry at 45.8x.

- Analysts expect the number of shares outstanding to grow by 1.13% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.45%, as per the Simply Wall St company report.

ASM International Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Revenue growth in ASM International's mature logic/foundry segment, especially in China, is showing signs of normalization after an exceptional period, which could impact future revenues as demand stabilizes globally.

- Sales in the power/analog/wafer market have been significantly down year-to-date, and this segment is not expected to recover until the second half of 2025 or later, which could impact ASM's overall revenue growth and profitability.

- The company's increased net R&D expenses, which rose 36% year-on-year, could pressure net margins if expected revenues from new technologies and projects do not fully materialize.

- Uncertainty around new export control regulations could affect ASM's sales forecast for China, leading to potential revenue declines if the outcome is more restrictive than anticipated.

- Economic growth remains relatively weak, and the industrial and automotive markets continue to face significant downturns, limiting visibility on revenue recovery in these markets, which could impact overall earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €684.45 for ASM International based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €960.0, and the most bearish reporting a price target of just €519.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €4.6 billion, earnings will come to €1.1 billion, and it would be trading on a PE ratio of 36.0x, assuming you use a discount rate of 6.5%.

- Given the current share price of €531.2, the analyst's price target of €684.45 is 22.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives