Narratives are currently in beta

Key Takeaways

- Strategic partnerships and new lithium production plants aim to increase revenue and earnings by expanding in India's steel and battery markets.

- Restructuring to streamline operations and focus on high-margin sectors should enhance profitability and improve net margins.

- The decline in steel and battery material prices, alongside market entry risks and high initial costs, threatens POSCO's revenue growth and profit margins.

Catalysts

About POSCO Holdings- Operates as an integrated steel producer in Korea and internationally.

- The strategic alliance with JSW Group in India to build an integrated steel mill and collaborate on rechargeable battery materials and renewable energy sectors is poised to enhance POSCO's revenue by tapping into India's rapidly growing steel market, where domestic steel consumption is increasing, supported by government policies.

- The commissioning and ramp-up of the new lithium production plants, along with strategic plans to leverage India's growing prominence in EV production, are expected to contribute positively to POSCO's earnings by expanding its foothold in the high-demand battery materials market.

- POSCO's restructuring efforts, including divestiture of nonessential businesses and noncore assets, aim to enhance capital efficiency and are likely to improve net margins by streamlining operations and reducing overhead costs.

- The focus on premium automotive steel products and expansion plans in high-margin sectors such as the steel plate and renewable energy segments are expected to improve overall profitability and contribute to higher net margins in the future.

- The anticipated stabilization of lithium production and progress in product certification and supply contracts are catalysts that could significantly impact POSCO's future revenue growth in the rechargeable battery sector as demand for EV-related materials increases globally.

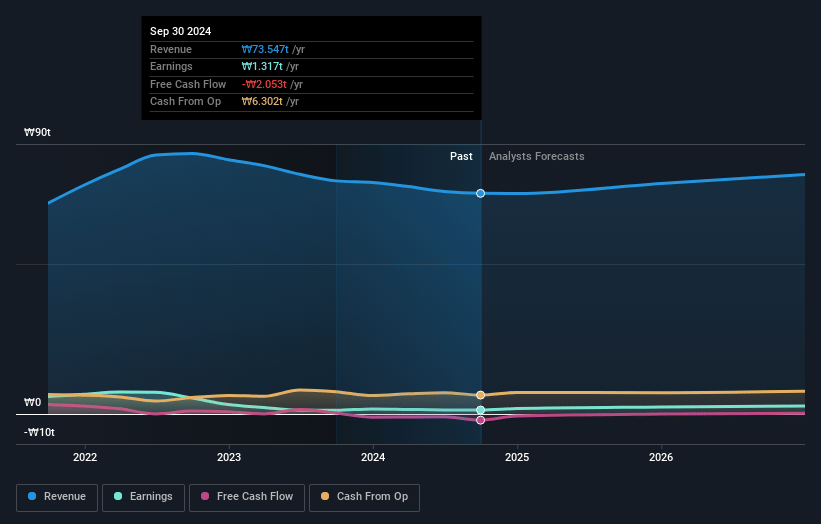

POSCO Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming POSCO Holdings's revenue will grow by 3.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 1.8% today to 4.1% in 3 years time.

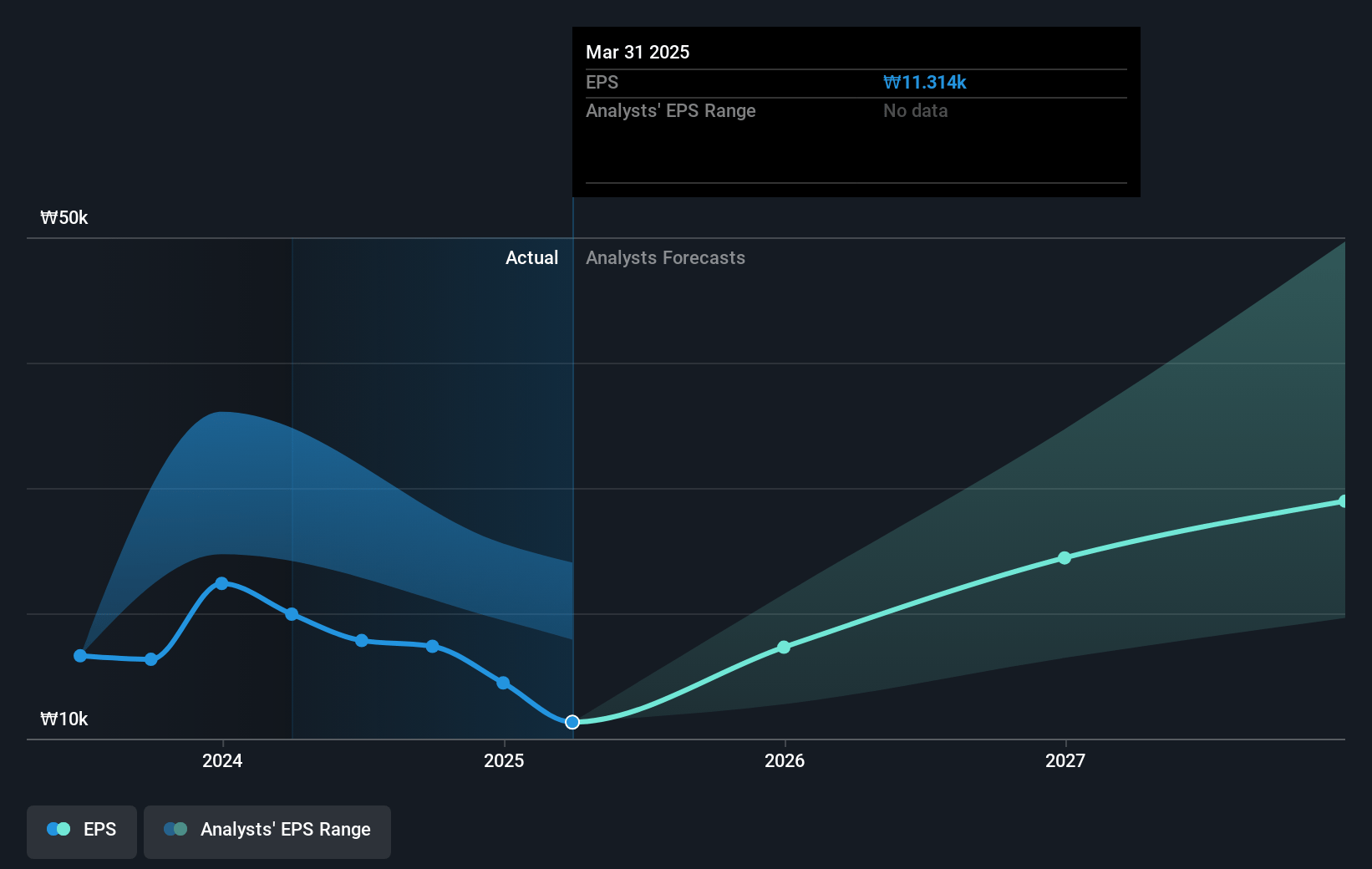

- Analysts expect earnings to reach ₩3342.7 billion (and earnings per share of ₩37113.03) by about January 2028, up from ₩1317.0 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ₩4344.0 billion in earnings, and the most bearish expecting ₩1726.9 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 16.3x on those 2028 earnings, up from 14.5x today. This future PE is greater than the current PE for the US Metals and Mining industry at 15.0x.

- Analysts expect the number of shares outstanding to grow by 6.18% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.15%, as per the Simply Wall St company report.

POSCO Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The decline in steel prices and the challenges in rechargeable battery materials due to falling lithium hydroxide prices could lead to reduced revenues and negatively impact net margins.

- Initial costs associated with the new lithium and brine production plants could weigh heavily on POSCO's earnings, delaying the ability to enhance utilization rates and reach normalized profit margins.

- The joint venture with JSW Group entails geopolitical and market entry risks, especially given the oligopolistic nature of the Indian steel market and the potential for oversupply, which could impede revenue growth.

- The current sluggishness in both the steel and battery materials markets has delayed cost recovery and could lead to reduced profit margins if demand does not improve as anticipated.

- Restructuring to sell non-core and underperforming assets, while beneficial long-term, may incur costs that could temporarily impact the company's earnings and cash flow.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₩440000.0 for POSCO Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₩650000.0, and the most bearish reporting a price target of just ₩250000.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₩82111.5 billion, earnings will come to ₩3342.7 billion, and it would be trading on a PE ratio of 16.3x, assuming you use a discount rate of 11.2%.

- Given the current share price of ₩253500.0, the analyst's price target of ₩440000.0 is 42.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives