Key Takeaways

- Expansion into iGaming and casual genres, along with successful games, is poised to boost DoubleUGames' revenue and overall financial performance.

- Strategic cross-border acquisitions and emphasis on in-house platform payments are set to enhance profitability and stabilize cash flow significantly.

- Dependence on forex gains and smaller-than-expected acquisitions could challenge growth, while high marketing costs and platform fees pressure operating margins.

Catalysts

About DoubleUGames- Develops and services mobile games worldwide.

- DoubleUGames plans to expand new business in the iGaming and casual genres in 2025, which is expected to accelerate revenue growth, especially with the success of flagship games like Merge Studio and additional games in development. This should positively impact overall revenue.

- The company is focusing on increasing the proportion of payments through its own DTC platform, aiming to double it from 8% in 2024, which could enhance profitability by reducing platform fees and improving EBITDA margins.

- DoubleUGames is actively seeking cross-border M&A opportunities, aiming to acquire more social casino businesses to ensure stable cash flow and profitability. Successful acquisitions could lead to significant top-line growth and improved net margins.

- Despite reducing its marketing expenses from 15% of revenue in 2023 to 8% in 2024, DoubleUGames achieved revenue growth and plans to maintain current marketing expense levels. This cost efficiency translates into better operating and net margins, optimizing earnings growth.

- The company recorded significant foreign exchange gains in 2024 due to the appreciation of cash assets held in U.S. dollars, which contributed to a record net income. Continued favorable currency rate trends in 2025 could further enhance net earnings.

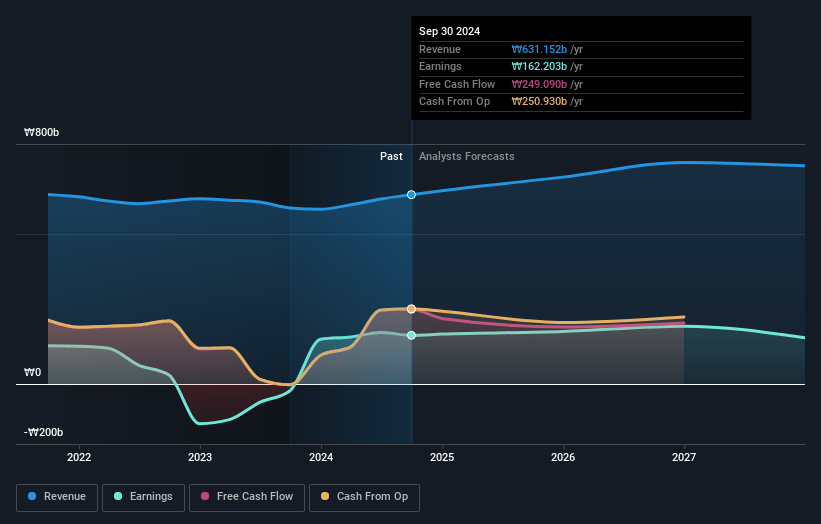

DoubleUGames Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming DoubleUGames's revenue will grow by 7.6% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 29.5% today to 25.9% in 3 years time.

- Analysts expect earnings to reach ₩204.2 billion (and earnings per share of ₩9704.1) by about May 2028, up from ₩187.2 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ₩231.0 billion in earnings, and the most bearish expecting ₩154.1 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 7.8x on those 2028 earnings, up from 6.0x today. This future PE is lower than the current PE for the KR Hospitality industry at 12.8x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.33%, as per the Simply Wall St company report.

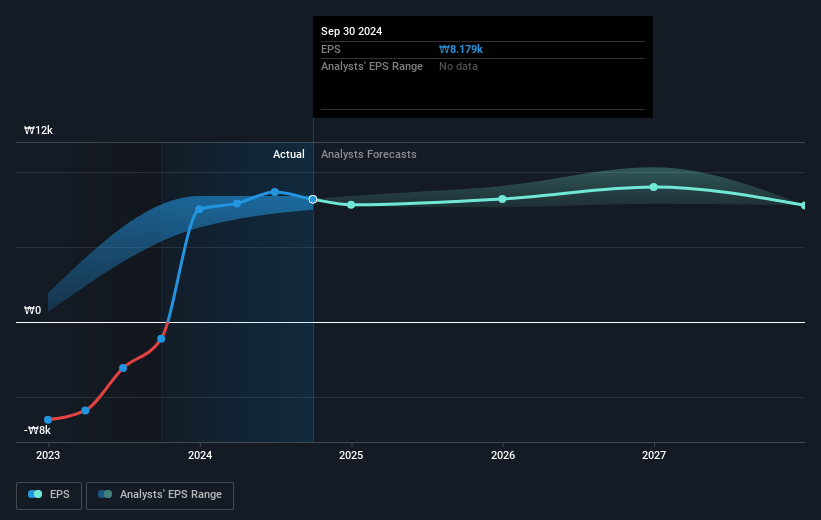

DoubleUGames Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company is heavily reliant on foreign exchange gains to boost net income due to its assets being largely in U.S. dollars, which poses a risk if currency rates fluctuate unfavorably, impacting net income.

- DoubleUGames' business is dependent on successful M&A activities to secure stable cash flow and profitability, but the size of the recent Paxie Games acquisition was smaller than expected, potentially affecting future growth and revenue if larger deals do not materialize.

- Revenue growth from the iGaming sector heavily relies on high marketing spend, which if not managed or yielding returns effectively, could adversely affect operating profit margins.

- The company's operating expenses include marketing and personnel costs that are tightly managed by reducing marketing spend and using automation, which can also lead to risks of under-investment affecting revenue growth or employee morale impacting operational efficiency.

- Continued reliance on platforms like Google and Apple, albeit reduced, still incurs significant platform costs, and any changes in their fee structures could impact DoubleUGames’ profit margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₩65818.182 for DoubleUGames based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₩74000.0, and the most bearish reporting a price target of just ₩56000.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₩789.6 billion, earnings will come to ₩204.2 billion, and it would be trading on a PE ratio of 7.8x, assuming you use a discount rate of 8.3%.

- Given the current share price of ₩56400.0, the analyst price target of ₩65818.18 is 14.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.