Key Takeaways

- Strategic investments in AI-driven innovations and ARM's performance bolster revenue growth and long-term profitability.

- Vision Fund 2's success in AI IPOs and T-Mobile stake solidify earnings and asset value.

- SoftBank's financial stability is vulnerable to its Vision Fund's volatility, foreign exchange movements, geopolitical risks, and the unpredictable performance of Arm and AI ventures.

Catalysts

About SoftBank Group- Provides telecommunication services in Japan and internationally.

- SoftBank Group's Vision Fund 2 is expected to continue generating gains from its portfolio of AI-driven companies, highlighted by promising IPOs and exits. These successes could significantly boost revenue and earnings.

- The robust performance of T-Mobile post-merger indicates sustained free cash flow growth. The increased equity value of SoftBank's stake in T-Mobile should positively impact earnings and net asset value.

- Investment in AI-centric companies such as OpenAI aligns with the strategic focus on transformative tech, which is expected to drive future revenue growth through scalable innovations and market expansion.

- The stable and significant cash reserves position SoftBank to capitalize on investment opportunities without compromising financials, suggesting potential for future revenue growth through strategic acquisitions.

- Continued strong performance of ARM, coupled with its strategic importance in AI chip development, is expected to contribute positively to SoftBank's net margins and long-term earnings growth.

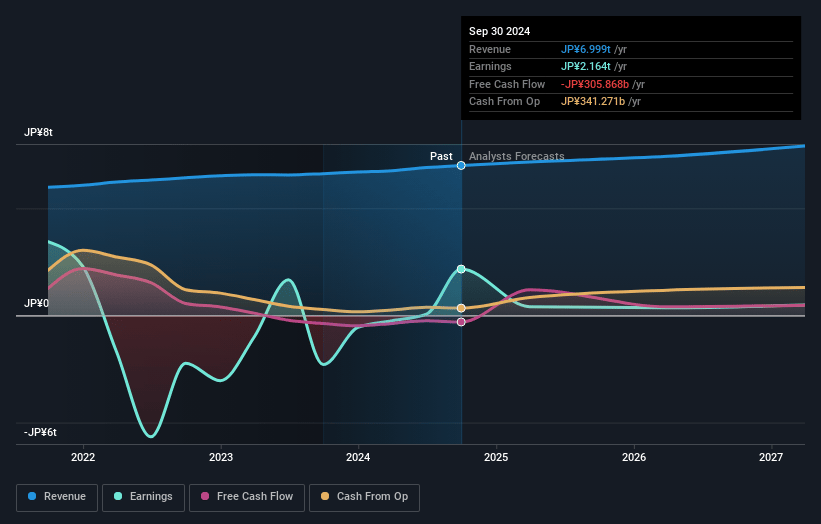

SoftBank Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming SoftBank Group's revenue will grow by 4.7% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 30.9% today to 5.2% in 3 years time.

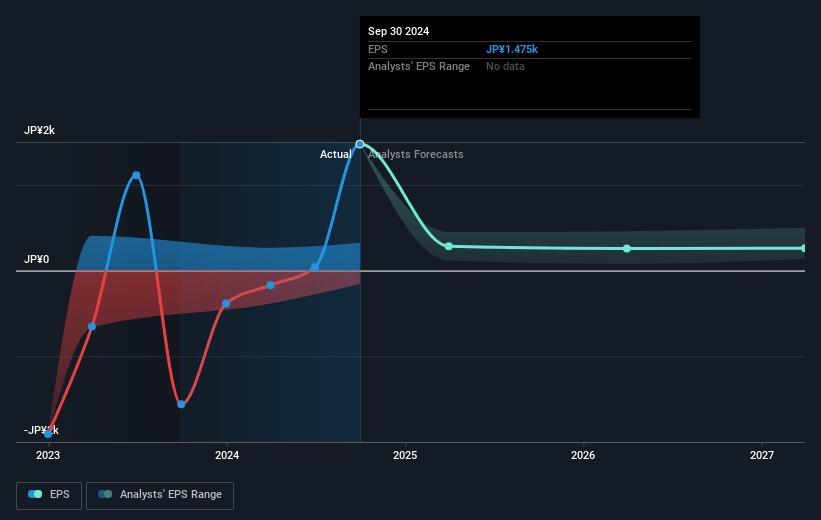

- Analysts expect earnings to reach ¥418.1 billion (and earnings per share of ¥260.44) by about January 2028, down from ¥2163.5 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ¥919.6 billion in earnings, and the most bearish expecting ¥199.9 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 51.8x on those 2028 earnings, up from 6.3x today. This future PE is greater than the current PE for the JP Wireless Telecom industry at 18.1x.

- Analysts expect the number of shares outstanding to grow by 3.67% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 4.69%, as per the Simply Wall St company report.

SoftBank Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- SoftBank's reliance on its Vision Fund for investment gains adds an element of uncertainty, as any underperformance or volatility in market conditions could adversely affect future revenue and net margins.

- The impact of foreign exchange movements, which led to negative effects on SoftBank's net asset value and equity, presents a risk to financial stability and earnings if these fluctuations continue unfavorably.

- SoftBank's exposure to geopolitical risks, such as potential changes in U.S.-China relations under different political administrations, could negatively impact portfolio companies and indirectly affect revenue streams.

- While Arm has shown strong performance, the high volatility in its stock price could lead to significant fluctuations in SoftBank's earnings if market conditions shift unexpectedly.

- The potential failure to successfully capitalize on AI and investment opportunities due to execution risks or mistimed investments could impede SoftBank's ability to increase future net asset value and maintain robust earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ¥11757.19 for SoftBank Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ¥16000.0, and the most bearish reporting a price target of just ¥8800.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ¥8030.2 billion, earnings will come to ¥418.1 billion, and it would be trading on a PE ratio of 51.8x, assuming you use a discount rate of 4.7%.

- Given the current share price of ¥9399.0, the analyst's price target of ¥11757.19 is 20.1% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives